Prebiotic Polyol Sweeteners Market Size

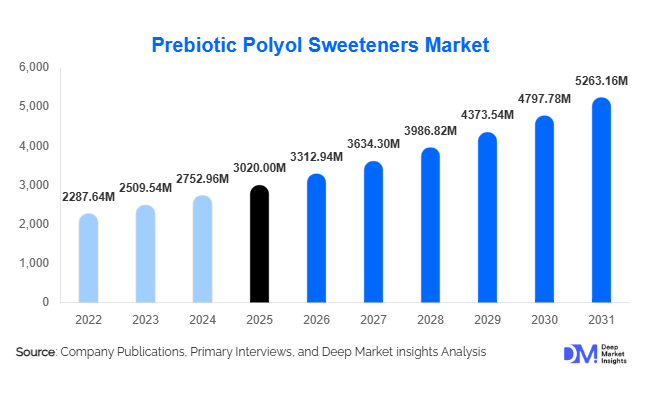

According to Deep Market Insights,the global prebiotic polyol sweeteners market size was valued at USD 3,020 million in 2025 and is projected to grow from USD 3,312.94 million in 2026 to reach USD 5,263.16 million by 2031, expanding at a CAGR of 9.7% during the forecast period (2026–2031). The market growth is primarily driven by rising global sugar reduction mandates, increasing diabetic and obese populations, and expanding demand for gut-health-oriented functional ingredients. Prebiotic polyols such as maltitol, lactitol, polydextrose, and isomalt are gaining strong adoption across bakery, confectionery, nutraceutical, and pharmaceutical applications due to their dual functionality—providing sweetness while supporting digestive health.

Key Market Insights

- Sugar reformulation initiatives are accelerating globally, with food manufacturers increasingly replacing sucrose with low-glycemic prebiotic polyols.

- Bakery & confectionery remain the largest application segment, driven by rapid growth in sugar-free chocolates and baked goods.

- North America dominates the global market, supported by strong diabetic-friendly product demand and regulatory pressure on sugar labeling.

- Asia-Pacific is the fastest-growing region, led by China and India due to rising diabetes prevalence and expanding functional food manufacturing.

- Powder form accounts for the majority of consumption, owing to ease of blending and industrial-scale production compatibility.

- Top five players account for approximately 52% of the market, reflecting moderate consolidation with strong global competition.

What are the latest trends in the prebiotic polyol sweeteners market?

Gut-Health Fortified Functional Foods

Food manufacturers are increasingly positioning products with digestive wellness claims. Prebiotic polyols such as polydextrose and lactitol are being incorporated into fiber-enriched snacks, dairy alternatives, and breakfast cereals. This shift is supported by rising consumer awareness of microbiome health and increasing willingness to pay premium prices for products delivering functional benefits beyond sweetness. Synbiotic formulations combining probiotics and prebiotic polyols are emerging in dietary supplements and functional beverages, particularly in North America, Japan, and Germany. Brands are emphasizing clean-label positioning and clinically supported digestive claims to enhance consumer trust.

Low-Glycemic & Diabetic-Friendly Reformulations

With more than half a billion adults globally managing diabetes or pre-diabetic conditions, food manufacturers are reformulating products to meet low-glycemic standards. Maltitol and isomalt are widely used in sugar-free confectionery due to their sugar-like taste profile and reduced caloric value. Regulatory sugar taxes across multiple countries are further incentivizing reformulation. Companies are investing in improved hydrogenation and starch conversion technologies to enhance sweetness intensity and reduce gastrointestinal side effects, thereby broadening application potential.

What are the key drivers in the prebiotic polyol sweeteners market?

Rising Global Diabetes and Obesity Rates

The growing prevalence of lifestyle-related diseases is a primary growth driver. Consumers are actively seeking reduced-sugar products that support blood sugar control. Prebiotic polyols provide a viable alternative due to their low glycemic index and reduced caloric content, supporting demand across bakery, beverages, and nutraceuticals. This health-driven demand has resulted in sustained double-digit growth in sugar-free product launches globally.

Sugar Reduction Regulations and Taxation

Governments across North America, Europe, and Latin America are implementing sugar taxes and front-of-pack labeling mandates. These regulatory measures compel food producers to adopt alternative sweeteners. Prebiotic polyols are favored due to their multifunctional properties and compatibility with industrial processing. Reformulation contracts with multinational FMCG players are significantly boosting bulk demand through B2B channels.

What are the restraints for the global market?

Digestive Tolerance Limitations

Excessive consumption of polyols can cause gastrointestinal discomfort, necessitating mandatory labeling in several countries. This limits usage concentration in certain applications and requires formulation balancing.

Raw Material Price Volatility

Polyols are derived primarily from corn and wheat starch. Fluctuations in agricultural commodity prices and energy costs impact production margins and pricing stability, posing challenges for manufacturers.

What are the key opportunities in the prebiotic polyol sweeteners industry?

Expansion in Emerging Markets

Countries such as India, Indonesia, Brazil, and Vietnam present high-growth opportunities due to rising middle-class incomes and increasing health awareness. Government initiatives such as domestic food processing incentives are encouraging local manufacturing investments, reducing reliance on imports.

Synbiotic and Personalized Nutrition Products

The integration of prebiotic polyols into personalized nutrition and microbiome-targeted supplements represents a high-value opportunity. Partnerships between ingredient manufacturers and probiotic companies are driving innovation in digestive health solutions.

Product Type Insights

Maltitol dominates the global prebiotic polyols market, accounting for approximately 28% of the total market share in 2025. The segment’s leadership is primarily driven by its close resemblance to sucrose in taste and texture, superior thermal stability, and excellent compatibility with chocolate, bakery, and confectionery formulations. Its low glycemic index and reduced caloric value make it highly preferred in sugar-free and diabetic-friendly product formulations, particularly in developed markets. The expanding global demand for reduced-sugar processed foods continues to strengthen maltitol’s market position.

Polydextrose is emerging as the fastest-growing product type due to its dual functionality as both a low-calorie bulking agent and a soluble dietary fiber. Increasing consumer awareness regarding gut health, digestive wellness, and fiber enrichment in daily diets is accelerating adoption across functional foods and nutraceuticals. Isomalt and lactitol are gaining significant traction in pharmaceutical and nutraceutical applications due to their tooth-friendly properties and suitability in chewable tablets and lozenges. Hydrogenated starch hydrolysates (HSH) and specialty blends are increasingly utilized in large-scale industrial bakery and dairy processing, driven by their cost efficiency and moisture retention capabilities.

Form Insights

Powdered prebiotic polyols hold nearly 64% of the global market share in 2025, primarily driven by their logistical advantages, extended shelf life, ease of storage, and compatibility with dry-mix manufacturing processes. The powdered form enables precise dosing, better blending characteristics, and enhanced stability in bakery premixes, confectionery fillings, and nutritional supplement formulations. The rapid expansion of industrial-scale food processing facilities globally further supports the dominance of powdered formats.

Liquid forms account for a comparatively smaller share but maintain steady demand in beverages, pharmaceutical syrups, and liquid dietary supplements. Their functional solubility and ease of incorporation into ready-to-drink products support niche growth, although storage constraints and shorter shelf life limit large-scale adoption.

Application Insights

Bakery & confectionery applications lead the market with a 34% share of total revenue in 2025. The segment’s dominance is driven by rising global demand for sugar-free chocolates, cookies, chewing gums, and reduced-calorie baked goods. Increasing regulatory pressure on sugar reduction, combined with consumer preference for indulgent yet healthier alternatives, continues to fuel innovation in this segment.

Nutraceutical applications represent the fastest-growing segment, supported by rising consumption of fiber supplements, gut-health capsules, and functional powders. Growing awareness regarding digestive health and immunity enhancement, particularly post-pandemic, is accelerating product launches in this category. Functional beverages are also emerging as a strong application area, particularly in Asia-Pacific, where demand for fortified drinks and low-calorie hydration products is expanding rapidly.

Distribution Channel Insights

B2B industrial sales account for approximately 72% of total market revenue, reflecting bulk procurement by multinational food, beverage, and pharmaceutical manufacturers. Long-term direct supply agreements dominate high-volume transactions, ensuring price stability and consistent quality standards. Strategic supplier partnerships and global sourcing contracts further strengthen the B2B ecosystem.

Specialty ingredient distributors serve small and mid-scale producers, particularly in emerging markets, providing customized blends and technical formulation support. Although smaller in share, this channel plays a crucial role in expanding market penetration across regional manufacturers and niche health-focused brands.

End-Use Industry Insights

The food processing industry represents 56% of total global demand, valued at approximately USD 1,800 million in 2026. Growth in this segment is primarily driven by large-scale production of sugar-reduced packaged foods, export-oriented confectionery manufacturing, and private-label product expansion across retail chains. Reformulation initiatives by leading food brands to comply with sugar reduction targets further strengthen demand.

The nutraceutical industry is the fastest-growing end-use sector, projected to expand at over 11% CAGR during the forecast period. Rapid growth in digestive health supplements, prebiotic capsules, and functional nutrition powders significantly contributes to this trend. Pharmaceutical demand remains stable, particularly for sugar-free medicinal syrups, chewable tablets, and pediatric formulations.Export-driven demand remains strong in the United States, Germany, and China, where processed food exports continue to expand and global supply chain integration enhances cross-border ingredient trade.

| By Product Type | By Form | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 32% of the global market share in 2025, with the United States contributing nearly 78% of regional demand. Growth in the region is driven by high diabetes prevalence, increasing consumer demand for low-calorie and keto-friendly products, and strong regulatory pressure to reduce added sugar in packaged foods. Advanced food processing infrastructure, high R&D investments, and widespread adoption of functional ingredients further support regional expansion. The presence of multinational food manufacturers and strong retail distribution networks enhances market maturity.

Europe

Europe accounts for roughly 29% of global demand, led by Germany, France, and the UK. The region benefits from well-established functional food markets, stringent sugar taxation policies, and supportive regulatory frameworks for prebiotic and fiber labeling. Clean-label product innovation and strong consumer preference for digestive health solutions continue to accelerate market growth. Additionally, rising demand for sugar-free confectionery across Western Europe sustains steady adoption.

Asia-Pacific

Asia-Pacific represents about 30% of the global market and is the fastest-growing region, expanding at nearly 11% CAGR. China serves as a major production and export hub due to large-scale manufacturing capacity and cost competitiveness. India is the fastest-growing country in the region, expanding at approximately 13% CAGR, supported by rising diabetes prevalence, rapid urbanization, expanding middle-class consumption, and increasing demand for processed and functional foods. Growing investments in domestic nutraceutical manufacturing further accelerate regional growth.

Latin America

Latin America demonstrates steady growth, primarily driven by Brazil and Mexico. Sugar taxation policies, rising health awareness, and expanding middle-class populations are encouraging reformulation of traditional high-sugar food products. Increasing investments in local food processing industries and growing exports of confectionery products further contribute to regional demand.

Middle East & Africa

The Middle East & Africa region is witnessing gradual expansion, with the UAE and Saudi Arabia serving as key demand centers. Growth is supported by rising health consciousness, government initiatives to reduce sugar consumption, expanding food manufacturing sectors, and increasing imports of specialty food ingredients. Urbanization and growing premium retail formats further enhance market opportunities across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Prebiotic Polyol Sweeteners Market

- Cargill Inc.

- Roquette Frères

- Ingredion Incorporated

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Tereos Group

- Mitsubishi Corporation Life Sciences

- Shandong Futaste Co., Ltd.

- Gulshan Polyols Ltd.

- BENEO GmbH

- Baolingbao Biology Co., Ltd.

- Wilmar International Ltd.

- SPI Pharma

- Dancheng Caixin Sugar Industry Co., Ltd.

- Zibo ZhongShi Green Biotech Co., Ltd.