Poultry Products Market Size

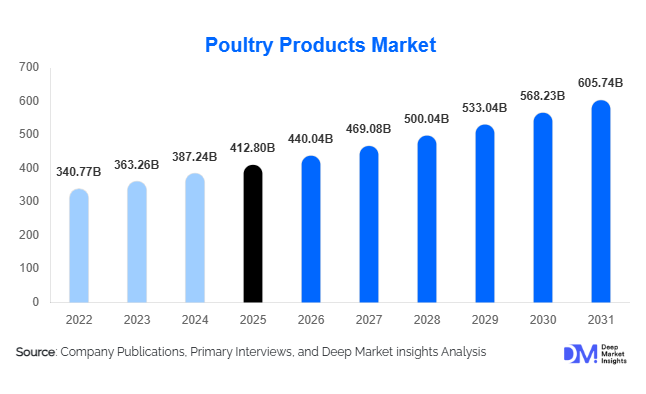

According to Deep Market Insights, the global poultry products market size was valued at USD 412.8 billion in 2025 and is projected to grow from USD 440.04 billion in 2026 to reach USD 605.74 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The poultry products market growth is primarily driven by rising global protein consumption, affordability compared to red meat, expansion of quick-service restaurant (QSR) chains, and increasing consumer preference for lean and high-protein diets. Rapid urbanization, cold-chain expansion, and technological advancements in poultry farming and processing are further accelerating industry growth. Poultry remains one of the most accessible animal proteins globally, supported by efficient production cycles, relatively lower feed conversion ratios, and strong adaptability across developed and emerging markets.

Key Market Insights

- Chicken dominates global poultry consumption, accounting for the majority of production due to affordability and cultural acceptance across regions.

- Processed and value-added poultry products are expanding rapidly, supported by convenience food demand and urban lifestyles.

- Asia-Pacific leads global consumption, driven by population growth and rising middle-class income levels.

- Foodservice demand is accelerating poultry utilization, especially through fast-food and ready-to-eat meal expansion.

- Automation and precision poultry farming technologies are improving yield efficiency and biosecurity standards.

- Export-oriented production hubs such as Brazil, the U.S., and Thailand are strengthening global trade flows.

What are the latest trends in the poultry products market?

Shift Toward Value-Added and Ready-to-Cook Poultry

Consumers increasingly prefer processed poultry formats such as marinated cuts, nuggets, sausages, and ready-to-cook meals. Urbanization and dual-income households are driving demand for convenient protein options requiring minimal preparation. Manufacturers are expanding portfolios with flavored, pre-seasoned, and frozen poultry products tailored to regional tastes. Retailers are also allocating greater shelf space to chilled and frozen poultry categories, reflecting changing purchasing behavior. Premiumization through antibiotic-free, organic, and free-range poultry offerings is emerging strongly in developed markets.

Technology Integration in Poultry Farming

Automation, artificial intelligence, and IoT-enabled monitoring systems are transforming poultry farming operations. Smart feeding systems, environmental monitoring sensors, and predictive disease analytics are helping producers improve bird health and reduce mortality rates. Processing plants are adopting robotics for cutting, packaging, and quality inspection, improving productivity while maintaining food safety standards. Blockchain traceability solutions are also gaining traction, enabling transparency from farm to consumer and strengthening trust among health-conscious buyers.

What are the key drivers in the poultry products market?

Rising Global Protein Consumption

Growing populations and rising incomes are increasing demand for affordable animal protein. Poultry offers a cost-effective alternative to beef and pork, particularly in emerging economies where dietary diversification is accelerating. Health-conscious consumers increasingly view poultry as a lean protein source with lower fat content, supporting sustained consumption growth.

Expansion of Quick-Service Restaurants and Foodservice Chains

The rapid expansion of global QSR brands and regional foodservice operators has significantly increased poultry demand. Fried chicken chains, sandwich outlets, and delivery-based kitchens rely heavily on standardized poultry cuts. Foodservice operators prefer poultry due to consistent cooking performance and lower procurement costs compared to red meats.

Advancements in Supply Chain and Cold Storage Infrastructure

Investments in refrigerated logistics and cold storage networks are enabling broader distribution of frozen and chilled poultry products. Emerging markets are witnessing rapid cold-chain expansion, allowing producers to reach previously underserved regions and reduce spoilage losses.

What are the restraints for the global market?

Volatility in Feed Prices

Poultry production heavily depends on feed inputs such as corn and soybean meal. Fluctuating commodity prices directly impact production costs and profit margins. Feed cost inflation often leads to pricing pressures across the supply chain.

Disease Outbreaks and Biosecurity Risks

Avian influenza and other poultry diseases pose periodic risks to production and international trade. Outbreaks lead to culling measures, export restrictions, and supply disruptions, creating uncertainty for producers and processors.

What are the key opportunities in the poultry products industry?

Emerging Market Consumption Growth

Rapid urbanization and income growth in Asia, Africa, and Latin America present strong opportunities for poultry producers. Governments are supporting domestic poultry industries to enhance food security, encouraging investments in modern farming infrastructure and processing facilities.

Alternative Feed and Sustainable Production Systems

Innovations in alternative feed ingredients, including insect protein and plant-based additives, are improving sustainability while reducing feed dependency risks. Producers adopting environmentally efficient practices are gaining competitive advantages through ESG-focused consumer demand.

Export Expansion and Trade Diversification

Export-oriented producers are expanding into new markets across the Middle East and Southeast Asia. Trade agreements and halal-certified processing facilities are enabling companies to tap into high-growth import markets with rising poultry consumption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 412.80 Billion |

| Market Size in 2026 | USD 440.04 Billion |

| Market Size in 2031 | USD 605.74 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fresh poultry products continue to dominate the global poultry products market, accounting for approximately 46% of the global market share in 2025. The leadership of this segment is primarily driven by strong consumer preference for freshly sourced protein, perceived nutritional superiority, and increasing demand for minimally processed food products across both developed and emerging economies. Rising urban populations and improved cold-chain logistics have enabled retailers to maintain product freshness while expanding distribution reach. Additionally, growing awareness regarding clean-label food consumption and reduced processing has further strengthened demand for fresh poultry across supermarkets, wet markets, and specialty meat retailers. Frozen poultry products remain a significant segment due to their longer shelf life, price stability, and suitability for international trade and bulk procurement, particularly in import-dependent regions. Meanwhile, processed poultry products represent the fastest-growing category, supported by changing lifestyles, increasing workforce participation, and demand for ready-to-cook and ready-to-eat meal solutions. Expansion of quick-service restaurants, convenience retail formats, and value-added product innovation such as marinated, breaded, and seasoned poultry offerings continues to accelerate growth within this segment.

Application Insights

Foodservice applications emerged as the leading segment, contributing nearly 39% of total poultry product consumption in 2025, primarily driven by the rapid expansion of quick-service restaurant chains, casual dining formats, and online food delivery ecosystems worldwide. Poultry’s cost efficiency, versatility across cuisines, and shorter preparation time compared to red meat make it the preferred protein for commercial kitchens. Increasing consumer preference for chicken-based menu items, particularly fried chicken, grilled products, and sandwiches, has further strengthened foodservice demand. Retail household consumption remains stable and resilient, supported by rising home cooking trends, health-conscious dietary shifts toward lean protein, and growing penetration of packaged poultry products in organized retail channels. Institutional applications, including schools, hospitals, corporate cafeterias, and large-scale catering services, are witnessing gradual expansion due to population growth, urban infrastructure development, and increasing reliance on standardized protein supply for mass meal programs.

Distribution Channel Insights

Modern retail channels, including supermarkets and hypermarkets, hold approximately 41% market share, supported by expanding organized retail infrastructure, improved refrigeration facilities, and consumer trust in packaged and quality-certified poultry products. The dominance of this segment is driven by convenience, product variety, standardized hygiene practices, and promotional pricing strategies that attract urban consumers. Traditional retail channels continue to maintain relevance in developing economies where wet markets remain culturally significant; however, their share is gradually transitioning toward organized formats. Online grocery platforms are emerging rapidly as a transformative distribution channel, particularly in metropolitan regions, supported by digital adoption, app-based purchasing behavior, and advancements in last-mile cold delivery logistics. Subscription-based meat delivery services and direct-to-consumer poultry brands are further reshaping purchasing patterns by offering freshness guarantees, traceability, and customized product options.

End-Use Industry Insights

The foodservice industry represents the fastest-growing end-use sector, expanding at over 7% annually as global dining-out culture strengthens and convenience-driven consumption increases. The proliferation of quick-service restaurants, cloud kitchens, and delivery-only brands has significantly elevated poultry demand due to its affordability and adaptability across global cuisines. Retail household consumption continues to grow steadily, supported by rising health awareness, increasing protein intake among younger demographics, and growing popularity of home-prepared meals. Export-oriented demand is also expanding as major poultry-producing nations scale processing capacities to address supply shortages and fluctuating red meat availability in importing countries. Institutional catering, including airlines, hospitality chains, educational institutions, and healthcare facilities, contributes incremental growth through long-term supply contracts and standardized meal provisioning requirements, reinforcing consistent demand across economic cycles.

Explore more data points, trends and opportunities Download Free Sample Report

Poultry Products Market Segmentations

By Product Type

- Fresh Poultry

- Frozen Poultry

- Processed Poultry

- Organic/Antibiotic-Free Poultry

By Application

- Foodservice

- Retail Household Consumption

- Institutional & Hospitality

- Exports & International Trade

By Distribution Channel

- Modern Retail

- Traditional Retail

- Online Grocery Platforms

- Direct Foodservice Contracts

- Wholesale Distributors

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 36% of the global poultry products market in 2025, making it the largest regional market. Growth across the region is driven by rapid population expansion, rising disposable incomes, and increasing dietary transition from traditional carbohydrate-heavy meals toward affordable animal protein sources. China remains the largest consumer due to strong domestic demand, evolving dietary preferences, and large-scale commercial poultry farming operations. India is among the fastest-growing markets, supported by expanding middle-class consumption, government initiatives encouraging organized livestock farming, and increasing penetration of branded poultry products. Southeast Asian countries, including Indonesia, Vietnam, and the Philippines, are witnessing rising imports and domestic production investments to meet accelerating urban demand. Improvements in cold-chain infrastructure, expansion of modern retail networks, and increasing adoption of processed poultry products further strengthen regional growth momentum.

North America

North America held nearly 24% market share, supported by high per-capita poultry consumption and technologically advanced production systems. The United States dominates regional output, benefiting from vertically integrated poultry operations, strong export competitiveness, and continuous innovation in processing efficiency. Regional growth is driven by consumer preference for lean protein alternatives, rising demand for value-added poultry products, and strong foodservice sector performance. Expansion of ready-to-eat meal categories and premium organic poultry offerings also contributes to market value growth. Canada demonstrates stable expansion supported by premiumization trends, sustainability-focused farming practices, and increasing demand for antibiotic-free and welfare-certified poultry products.

Europe

Europe demonstrates steady market growth led by Germany, France, the United Kingdom, and Poland, supported by strong regulatory frameworks and evolving consumer preferences toward sustainable and ethically sourced food products. Demand for organic, free-range, and animal-welfare-certified poultry continues to rise across Western Europe, encouraging producers to adopt higher production standards. Eastern Europe is increasingly emerging as a competitive production hub due to lower operational costs and expanding export capabilities within the European Union. Regional growth is further supported by innovation in processed poultry offerings, growing convenience food demand, and increasing retail penetration of private-label poultry products.

Middle East & Africa

The Middle East & Africa region presents strong long-term growth potential, driven by population expansion, urbanization, and rising protein consumption levels. The Middle East remains heavily dependent on poultry imports, particularly in Saudi Arabia and the United Arab Emirates, where domestic production capacity is limited by climatic constraints. Halal-certified poultry demand plays a central role in shaping trade flows, encouraging imports primarily from Brazil and European exporters. Governments across Gulf countries are investing in food security initiatives and domestic poultry farming projects to reduce import reliance. In Africa, increasing urban migration, improving retail infrastructure, and growing affordability of poultry compared to red meat are accelerating consumption growth, positioning poultry as a primary protein source for emerging middle-income populations.

Latin America

Latin America remains a strategically important poultry-producing region, with Brazil leading global exports due to competitive feed availability, advanced farming efficiency, and strong international trade relationships. Mexico and Argentina represent major consumption markets supported by population growth and expanding foodservice sectors. Regional growth is driven by export-oriented investments, favorable agricultural resources, and increasing modernization of processing facilities. Government support for agribusiness expansion, combined with rising global demand for affordable protein, continues to strengthen Latin America’s role as a key supplier within the international poultry trade ecosystem.

Key Players in the Poultry Products Market

- Tyson Foods Inc.

- JBS S.A.

- BRF S.A.

- Sanderson Farms

- Perdue Farms

- CP Foods (Charoen Pokphand Foods)

- Pilgrim’s Pride Corporation

- Hormel Foods Corporation

- OSI Group

- Wayne-Sanderson Farms

- Moy Park

- Venky’s (India) Limited

- Nippon Ham Foods Ltd.

- NH Foods Ltd.

- Plukon Food Group