Poultry (Broiler) Market Size

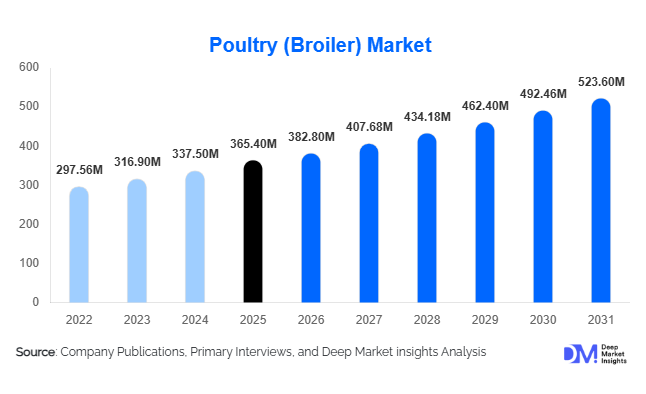

According to Deep Market Insights, the global poultry (broiler) market size was valued at USD 365.4 billion in 2025 and is projected to grow from USD 382.8 billion in 2026 to reach USD 523.6 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). Market expansion is primarily supported by rising global protein consumption, affordability of chicken compared with red meat, rapid urbanization, and strong growth in quick-service restaurants (QSRs) and processed food industries. Poultry remains the most consumed animal protein globally due to shorter production cycles, efficient feed conversion ratios, and fewer cultural or religious consumption restrictions compared to other meats.

Key Market Insights

- Broiler chicken accounts for the largest share of global meat consumption growth, supported by cost efficiency and scalable production systems.

- Processed and value-added poultry products are expanding rapidly, driven by convenience food demand and urban lifestyles.

- Asia-Pacific dominates production and consumption, led by China, India, Indonesia, and Thailand.

- Export-oriented producers such as Brazil and the United States continue to shape global pricing and trade flows.

- Automation, precision feeding, and genetics optimization are improving yield efficiency and reducing mortality rates.

- Sustainability and antibiotic-free production are emerging as key purchasing criteria among retailers and consumers.

What are the latest trends in the poultry (broiler) market?

Shift Toward Processed and Ready-to-Cook Poultry

The poultry industry is witnessing a structural transition from fresh whole birds toward processed, marinated, frozen, and ready-to-cook formats. Urban consumers increasingly prefer convenience-driven protein options that reduce cooking time while maintaining affordability. Food processors are investing heavily in automated deboning, portioning, and packaging facilities to support this shift. Retail chains and QSR operators are demanding standardized cuts such as breast fillets, nuggets, and strips, which deliver higher margins compared to whole birds. This transition is particularly visible across Asia-Pacific and Latin America, where rising middle-class populations are reshaping consumption patterns.

Technology-Led Efficiency Improvements

Producers are integrating precision farming technologies including IoT-based environmental monitoring, AI-driven feed optimization, and automated poultry housing systems. These technologies improve feed conversion ratios, reduce disease outbreaks, and enhance productivity per bird. Genetic advancements in broiler breeds are enabling faster growth cycles while maintaining meat quality. Digital traceability platforms are also gaining adoption, allowing processors and retailers to monitor farm-to-fork transparency, which strengthens consumer trust and regulatory compliance.

What are the key drivers in the poultry (broiler) market?

Rising Global Demand for Affordable Animal Protein

Poultry remains the most economical source of animal protein, making it the preferred choice in both developed and developing economies. Rising disposable incomes in emerging markets are enabling consumers to shift from plant-based staples toward protein-rich diets. Compared to beef and pork, poultry production requires lower feed input and shorter production cycles, allowing producers to respond quickly to demand fluctuations. Population growth and dietary diversification continue to drive consistent global consumption expansion.

Expansion of Foodservice and QSR Industries

The rapid global expansion of quick-service restaurant chains and food delivery platforms is significantly boosting demand for standardized broiler meat cuts. Chicken-based menus dominate fast-food offerings due to versatility and consumer acceptance. Large QSR chains rely heavily on contract poultry suppliers, ensuring stable long-term demand. Increasing penetration of fried chicken chains across Asia, the Middle East, and Africa is further accelerating production investments.

Export Market Growth and Trade Liberalization

International poultry trade is expanding as exporting countries leverage cost advantages and biosecurity improvements. Brazil, the U.S., and Thailand have strengthened export capacities through modern processing infrastructure and disease management systems. Growing import dependence among Middle Eastern and Asian countries is creating sustained demand for frozen broiler meat, supporting global market expansion.

What are the restraints for the global market?

Feed Cost Volatility

Poultry production profitability is highly dependent on feed prices, particularly corn and soybean meal. Fluctuations caused by climate conditions, geopolitical disruptions, and biofuel demand significantly impact production costs. Rising feed costs compress margins, especially for small and medium-scale producers operating without integrated supply chains.

Disease Outbreak Risks and Regulatory Constraints

Avian influenza outbreaks remain a persistent challenge, causing supply disruptions, trade restrictions, and culling losses. Increasing animal welfare regulations and antibiotic usage restrictions also require producers to invest in upgraded housing and biosecurity measures, raising operational costs.

What are the key opportunities in the poultry (broiler) industry?

Expansion in Emerging Markets

Rapid urbanization across Africa, Southeast Asia, and South Asia presents strong growth opportunities. Governments are encouraging domestic poultry production to enhance food security, creating investment opportunities in hatcheries, feed mills, and processing facilities. New entrants can leverage contract farming models to scale production efficiently while reducing capital intensity.

Value-Added and Premium Poultry Segments

Demand for antibiotic-free, organic, and free-range chicken is increasing among health-conscious consumers. Retailers and foodservice operators are introducing premium poultry categories with traceability certifications. Producers entering branded poultry segments benefit from higher margins and improved customer loyalty compared with commodity poultry sales.

Automation and Smart Farming Integration

Automation technologies offer opportunities to improve labor productivity and reduce mortality rates. Investments in robotic processing lines, climate-controlled housing, and AI-driven analytics enable producers to optimize output while maintaining consistent quality standards. Technology adoption is expected to differentiate large integrated players from smaller traditional farms.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 365.4 Million |

| Market Size in 2026 | USD 382.8 Million |

| Market Size in 2031 | USD 523.6 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global poultry market demonstrates strong segmentation dynamics across fresh, frozen, and processed poultry categories, each reflecting distinct consumer behaviors, supply chain maturity levels, and regional dietary preferences. Among these, fresh or chilled broiler chicken continues to dominate the global landscape, accounting for approximately 46% of the global poultry market in 2025. This leadership position is primarily supported by deeply rooted cultural consumption patterns across Asia-Pacific, the Middle East, and several developing economies where consumers strongly associate freshness with quality, nutrition, and food safety. In many emerging markets, traditional wet markets and neighborhood butcher systems remain integral components of food distribution, enabling daily purchase habits that reinforce the dominance of fresh poultry products.The leading driver behind fresh poultry’s market dominance is affordability combined with high protein value. Compared with red meat alternatives such as beef or lamb, poultry offers a cost-efficient protein source that aligns well with expanding middle-class populations and price-sensitive consumers. Additionally, shorter production cycles in broiler farming allow producers to respond quickly to demand fluctuations, ensuring consistent supply availability. Improvements in local farming infrastructure, better feed efficiency, and genetic advancements in poultry breeds further enhance productivity, strengthening the competitiveness of fresh poultry globally. Urban expansion across developing nations also contributes significantly, as improved transportation networks allow fresh products to reach metropolitan markets without requiring extensive freezing infrastructure.Technological innovation in food processing also plays a significant role. Manufacturers are introducing flavor diversification, healthier formulations, and premium product positioning, including low-fat, organic, and antibiotic-free processed poultry options. Expansion of frozen ready meals, snack foods, and protein-based convenience offerings continues to elevate processed poultry demand, particularly among younger consumers and urban populations. As modern retail penetration deepens worldwide, processed poultry is expected to steadily gain share from traditional fresh segments over the long term.

Application Insights

Poultry consumption patterns vary widely depending on application sectors, reflecting broader shifts in global food consumption habits. Foodservice applications currently lead poultry utilization, accounting for nearly 38% of global demand. The primary driver behind this leadership is the rapid expansion of quick-service restaurant (QSR) chains, fast-casual dining concepts, and delivery-based food platforms. Chicken-based menu items offer operational advantages for restaurants due to lower ingredient costs, menu versatility, and widespread consumer acceptance across cultural and religious groups. Fried chicken, grilled products, sandwiches, and wraps have become staple offerings in both developed and emerging markets, reinforcing sustained poultry demand through commercial food channels.Household retail consumption represents approximately 35% of global poultry demand, supported by evolving home cooking trends and improved accessibility through modern grocery retail. The leading driver for household consumption is increasing health awareness among consumers seeking lean protein alternatives. Poultry is widely perceived as healthier than red meat due to lower fat content and versatility in diverse cuisines. The pandemic-era shift toward home meal preparation has also created lasting behavioral changes, encouraging consumers to experiment with poultry-based recipes and meal planning.Food processing industries account for roughly 27% of total poultry utilization, benefiting from rising demand for packaged meals, frozen foods, and ready-to-eat snacks. Poultry’s adaptability as an ingredient allows manufacturers to incorporate it into a wide range of products, including soups, instant meals, protein snacks, and meal kits. Growth in this segment is primarily driven by convenience food consumption and expansion of global packaged food industries. Increasing adoption of automated processing facilities and standardized supply chains further enhances efficiency, allowing industrial users to scale poultry utilization at competitive costs.

Distribution Channel Insights

Distribution structures within the poultry market reflect varying levels of retail modernization and infrastructure development worldwide. Traditional retail channels and wet markets continue to dominate, contributing approximately 41% of global poultry sales volume. These channels remain highly influential in Asia, Africa, and parts of Latin America where consumers prioritize freshness and daily purchasing habits. The leading driver behind traditional retail dominance is accessibility and trust built through localized supply systems. Smaller retailers provide flexible pricing, immediate availability, and culturally familiar purchasing experiences that modern retail formats often cannot fully replicate.Modern retail formats, including supermarkets and hypermarkets, account for nearly 33% market share, supported by expanding cold-chain logistics and urban retail infrastructure. The key growth driver in this segment is rising consumer preference for hygiene, standardized quality, and product variety. Organized retail environments allow retailers to offer branded poultry products, packaged cuts, and value-added offerings that appeal to convenience-focused shoppers. Investments in refrigeration technology, supply chain traceability, and private-label poultry brands continue strengthening this distribution channel globally.Online grocery and direct-to-consumer sales, though currently representing around 6% of global sales, are expanding rapidly as digital commerce ecosystems mature. The leading driver for online poultry distribution is the convergence of e-commerce adoption and improvements in last-mile cold delivery infrastructure. Consumers increasingly value doorstep delivery, subscription meat services, and digitally enabled traceability that ensures product origin transparency. As logistics technology evolves, online distribution is expected to become a major growth catalyst, particularly in urban markets.

End-Use Industry Insights

The poultry market serves multiple end-use industries, each contributing uniquely to demand expansion. The foodservice industry represents the fastest-growing end-use segment globally, fueled by the accelerating expansion of fried chicken chains, casual dining outlets, and delivery-focused restaurant formats. With the global QSR industry expanding at an annual rate of nearly 7–8%, poultry consumption continues to rise proportionally due to chicken’s operational efficiency, flavor adaptability, and universal consumer acceptance. Restaurants benefit from predictable cooking times, portion control, and cost advantages compared with other animal proteins.Processed food manufacturing is another rapidly expanding end-use industry. Frozen ready meals, protein snacks, and convenience-based food solutions increasingly rely on poultry ingredients due to scalability and consumer familiarity. Innovation in food technology allows manufacturers to develop high-protein packaged foods targeting health-conscious consumers, athletes, and busy professionals. Growth in retail freezer sections worldwide further amplifies industrial poultry demand.Export-oriented consumption also plays a critical role in global poultry dynamics. Several countries rely heavily on imported poultry products to ensure food security, particularly regions with limited domestic agricultural capacity. Stable international trade networks enable producers to balance supply-demand mismatches across regions, supporting market stability.Institutional consumption across hotels, healthcare facilities, military establishments, and educational institutions continues expanding steadily. Increasing urban population density and rising organized catering services drive consistent procurement volumes, contributing to long-term demand predictability for poultry suppliers.

Explore more data points, trends and opportunities Download Free Sample Report

Poultry (Broiler) Market Segmentations

By Product Type

- Whole Broiler Chicken

- Chicken Cuts

- Processed & Value-Added Poultry Products

- Frozen Broiler Products

- Fresh/Chilled Broiler Meat

By Production System

- Conventional Intensive Farming

- Antibiotic-Free Poultry

- Organic & Free-Range Broilers

- Contract Farming/Integrated Poultry Systems

By Distribution Channel

- Modern Retail

- Traditional Wet Markets

- Foodservice & HoReCa Supply

- Online Meat Delivery Platforms

- Direct Processor-to-Industrial Buyers

By End-Use Industry

- Household Consumption

- Quick Service Restaurants

- Food Processing Industry

- Institutional Catering

- Export Markets

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global poultry market, accounting for approximately 38% of total market share in 2025. The region’s leadership is driven primarily by population scale, rapid urbanization, and increasing dietary protein consumption. China remains the largest consumer within the region, supported by expanding processed poultry demand and modernization of retail infrastructure. Rising disposable incomes encourage dietary diversification, with poultry emerging as a preferred protein due to affordability and cultural compatibility.India represents one of the fastest-growing poultry markets globally, fueled by expanding middle-class populations, improving cold-chain logistics, and growth in organized poultry farming systems. Government support for agricultural modernization and rising investments in feed production enhance domestic supply capabilities. Southeast Asian countries such as Indonesia and Thailand function as key production and export hubs due to competitive labor costs and advanced processing facilities. The leading regional growth driver remains poultry’s price advantage over red meat combined with strong urban consumption growth and evolving foodservice sectors.

North America

North America holds nearly 22% of global market share, led by the United States as one of the world’s largest poultry producers and exporters. Market maturity is supported by highly automated production systems, advanced genetics, and vertically integrated supply chains that optimize efficiency from feed production to retail distribution. Strong domestic consumption patterns sustain stable demand levels.The primary regional growth driver is increasing demand for processed and value-added poultry products aligned with convenience-focused lifestyles. Expansion of ready-to-eat meals, frozen foods, and restaurant delivery platforms continues strengthening consumption volumes. Additionally, technological advancements in processing efficiency and sustainability practices contribute to productivity improvements across the industry.

Europe

Europe accounts for approximately 18% of global poultry market share, characterized by stringent regulatory standards and evolving consumer preferences. Demand across major markets such as the United Kingdom, Germany, France, and Poland remains stable, supported by poultry’s positioning as a healthier protein alternative.The leading driver of regional growth is increasing consumer demand for antibiotic-free, organic, and animal welfare-certified poultry products. Sustainability concerns and environmental awareness strongly influence purchasing decisions, prompting producers to invest in traceability systems and ethical farming practices. Eastern Europe continues emerging as a production expansion zone due to lower operating costs and favorable investment environments, strengthening regional supply capacity.

Middle East & Africa

The Middle East and Africa region represents a rapidly expanding poultry market driven by demographic growth and food security priorities. Countries such as Saudi Arabia and the United Arab Emirates rely significantly on poultry imports to meet domestic demand, creating strong trade opportunities for global exporters. Government-led food security initiatives are encouraging investment in domestic poultry farming infrastructure, including feed production and processing facilities.Africa is among the fastest-growing regional markets, particularly Nigeria and South Africa, where poultry serves as an affordable protein source for expanding populations. Rising urbanization, improving retail networks, and increasing investment in local poultry production are key growth drivers. Poultry’s affordability relative to beef and lamb remains the dominant factor supporting consumption expansion across the region.

Latin America

Latin America accounts for nearly 12% of global poultry market share, led by Brazil and Mexico. Brazil remains a dominant global exporter due to cost-efficient large-scale farming operations, favorable feed availability, and strong international trade relationships. Export competitiveness allows regional producers to maintain stable production volumes even during domestic demand fluctuations.Regional growth is primarily driven by urbanization, improving economic stability, and expanding modern retail infrastructure. Increasing adoption of processed poultry products and rising foodservice sector development further support consumption growth. Government support for agricultural exports and continuous investment in production efficiency position Latin America as a critical contributor to global poultry supply expansion over the forecast period.

Key Players in the Global Poultry (Broiler) Market

- JBS S.A.

- Tyson Foods Inc.

- BRF S.A.

- CP Foods (Charoen Pokphand Foods)

- Sanderson Farms

- Perdue Farms

- Pilgrim’s Pride Corporation

- Hormel Foods Corporation

- Wayne-Sanderson Farms

- Koch Foods

- Amadori Group

- PHW Group

- MHP SE

- Japfa Ltd.

- Venky’s (India) Limited