Post-Workout Supplements Market Size

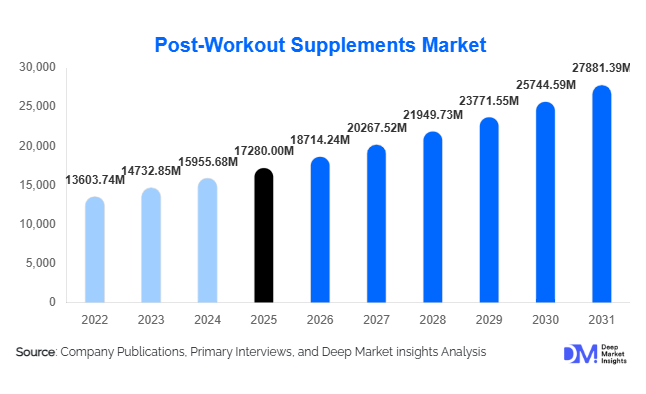

According to Deep Market Insights,the global post-workout supplements market size was valued at USD 17,280 million in 2025 and is projected to grow from USD 18,714.24 million in 2026 to reach USD 27,881.39 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing global fitness participation, rising awareness of muscle recovery science, and expanding adoption of protein-based nutrition across both athletic and lifestyle consumer segments. Growing penetration of e-commerce platforms, personalized nutrition models, and plant-based formulations are further strengthening demand across developed and emerging economies.

Key Market Insights

- Protein powders dominate the market, accounting for more than half of global revenue share due to affordability, convenience, and strong scientific validation for muscle recovery.

- Plant-based formulations are the fastest-growing category, driven by rising vegan adoption, lactose intolerance awareness, and clean-label preferences.

- North America leads the global market, supported by high disposable incomes, strong sports culture, and advanced retail infrastructure.

- Asia-Pacific is the fastest-growing region, fueled by expanding gym memberships and rising protein awareness in India and China.

- Online retail channels are rapidly gaining traction, enabling subscription-based and direct-to-consumer sales models.

- Personalized and functional recovery solutions, supported by wearable integration and AI-based nutrition planning, are reshaping product innovation.

What are the latest trends in the post-workout supplements market?

Shift Toward Plant-Based and Clean-Label Recovery

Consumers are increasingly demanding transparency in ingredient sourcing, non-GMO certifications, and minimal additive formulations. Plant-based proteins derived from pea, rice, and soy are experiencing accelerated adoption, particularly among younger and urban consumers. Clean-label recovery blends with reduced artificial sweeteners and natural flavoring systems are gaining shelf space across specialty nutrition stores and e-commerce platforms. Manufacturers are also incorporating digestive enzymes and probiotic strains to enhance absorption and gut compatibility, addressing concerns regarding bloating associated with traditional whey protein.

Personalized and Technology-Integrated Nutrition

The integration of wearable fitness devices and mobile health applications is driving demand for customized post-workout formulations. Consumers are increasingly tracking recovery metrics, sleep quality, and workout intensity, creating opportunities for AI-driven supplement recommendations. Subscription-based personalized nutrition services are expanding, particularly in North America and Europe. Companies are also investing in data analytics platforms to offer dynamic product recommendations, improving customer retention and lifetime value.

What are the key drivers in the post-workout supplements market?

Rising Global Fitness Participation

The steady growth of gym memberships, marathon participation, bodybuilding competitions, and home-based fitness programs has significantly increased demand for muscle recovery solutions. Recreational fitness enthusiasts now represent a larger consumer base than professional athletes, expanding overall market volume.

Growing Awareness of Muscle Recovery Science

Scientific validation of protein timing, branched-chain amino acids (BCAAs), essential amino acids (EAAs), and creatine supplementation has enhanced consumer confidence. Increased educational marketing and influencer-led content have accelerated adoption among mainstream consumers seeking lean muscle gain and faster recovery cycles.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in dairy production impact whey protein concentrate and isolate pricing, while agricultural yield variability affects plant protein costs. These fluctuations influence profit margins and pricing strategies across premium and mass-market brands.

Regulatory and Labeling Compliance

Stringent regulations governing supplement claims, ingredient approvals, and labeling standards vary across regions. Compliance costs and approval delays can restrict product launches, especially in emerging markets with evolving nutraceutical regulations.

What are the key opportunities in the post-workout supplements industry?

Expansion into Clinical and Aging Populations

Post-workout formulations are increasingly being adopted in rehabilitation centers and for sarcopenia prevention among aging populations. Medical-grade protein blends and clinically validated amino acid supplements present strong institutional demand opportunities.

Emerging Market Manufacturing and Localization

Government initiatives such as Make in India and domestic nutraceutical production incentives in Asia are encouraging local manufacturing investments. Establishing regional production facilities reduces import dependency and enhances pricing competitiveness, particularly in price-sensitive markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17280 Million |

| Market Size in 2026 | USD 18714.24 Million |

| Market Size in 2031 | USD 27881.39 Million |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Protein powders continue to dominate the global post-workout supplements market, accounting for approximately 52% of the 2025 market share. The segment’s leadership is primarily driven by their superior cost efficiency per serving, high protein concentration, and strong clinical validation supporting muscle protein synthesis and recovery benefits. Whey-based formulations, in particular, benefit from rapid absorption kinetics and a complete amino acid profile, making them the preferred choice among strength trainers and bodybuilders. In addition, established brand equity and wide retail penetration further reinforce their market position. Recovery blends that combine protein with carbohydrates, branched-chain amino acids (BCAAs), creatine, and electrolytes are gaining traction among endurance athletes and hybrid training participants, as these formulations address glycogen replenishment and muscle repair simultaneously. Ready-to-drink (RTD) beverages are expanding steadily, supported by convenience-driven consumption patterns, improved flavor technologies, and the growing preference for portable nutrition solutions among urban consumers and working professionals.

Ingredient Source Insights

Animal-based formulations account for nearly 61% of global market share in 2025, largely driven by the widespread adoption of whey protein due to its complete amino acid composition, high leucine content, and rapid digestibility. The leading segment driver remains the strong body of scientific research validating whey’s effectiveness in enhancing muscle recovery, lean mass development, and post-exercise protein synthesis. Additionally, long-standing consumer trust and established supply chains contribute to the segment’s sustained dominance. However, plant-based proteins represent the fastest-growing category, supported by rising environmental awareness, lactose intolerance prevalence, and increasing adoption of vegan and flexitarian diets. Innovations in pea, rice, soy, and blended plant proteins are improving texture and amino acid balance, narrowing the performance gap with animal-based sources and expanding their appeal among mainstream fitness consumers.

Form Insights

Powder formats account for approximately 58% of total revenue share, maintaining their leadership due to affordability, extended shelf life, customizable dosing, and compatibility with personalized nutrition regimens. The primary growth driver for this segment is its flexibility, allowing consumers to adjust serving sizes, stack ingredients, and integrate products into smoothies or functional recipes. Bulk packaging options and subscription-based e-commerce models further enhance cost competitiveness. Meanwhile, ready-to-drink liquid formats are witnessing accelerated growth, particularly in metropolitan markets, as convenience, time efficiency, and single-serve packaging align with fast-paced lifestyles. Advancements in aseptic processing and clean-label formulations are also improving product stability and consumer acceptance.

Distribution Channel Insights

Online retail commands approximately 34% of the global 2025 market share, emerging as the leading distribution channel due to the expansion of direct-to-consumer strategies, subscription programs, and influencer-driven digital marketing campaigns. The key driver of this segment is the growing consumer preference for price transparency, product comparison, and access to niche or premium brands not widely available in brick-and-mortar stores. Data-driven personalization and targeted advertising further strengthen conversion rates. Specialty nutrition stores remain essential for premium positioning and personalized guidance, particularly for performance-oriented and first-time consumers seeking expert recommendations. Supermarkets and hypermarkets also maintain relevance by offering mass-market accessibility and promotional bundling.

Consumer Type Insights

Recreational fitness enthusiasts account for nearly 39% of global demand in 2025, surpassing professional athletes due to the expanding global participation in lifestyle fitness activities. The leading driver for this segment is the mainstreaming of fitness culture, fueled by social media influence, body transformation trends, and increasing awareness of preventive healthcare. Growth in boutique fitness studios, community-based training programs, and digital workout platforms has broadened the consumer base beyond competitive athletes. Professional athletes and serious bodybuilders continue to represent a high-value niche, characterized by premium product adoption and demand for scientifically validated formulations.

End-Use Setting Insights

Home consumption dominates the market with approximately 63% share, supported by the sustained shift toward home-based workouts, digital fitness subscriptions, and hybrid training models that combine gym and at-home routines. The leading driver of this segment is convenience, as consumers increasingly integrate supplementation into daily wellness routines without reliance on gym infrastructure. The proliferation of smart fitness equipment and virtual coaching platforms has further accelerated at-home consumption patterns. Gym-based consumption remains significant, particularly in developed markets where established fitness chains and performance training facilities drive product visibility and impulse purchases. Clinical and rehabilitation settings are expanding at a CAGR exceeding 9%, supported by the growing use of protein supplementation in injury recovery, sarcopenia management, and post-surgical rehabilitation protocols.

Explore more data points, trends and opportunities Download Free Sample Report

Post-Workout Supplements Market Segmentations

By Product Type

- Protein Powders

- Recovery Blends

- BCAA & EAA Formulations

- Creatine-Based Supplements

- Glutamine Supplements

- Carbohydrate Recovery Drinks

- Ready-to-Drink (RTD) Post-Workout Beverages

- Post-Workout Nutrition Bars

By Ingredient Source

- Animal-Based

- Plant-Based

- Synthetic Amino Acid-Based

- Mixed Source Formulations

By Form

- Powder

- Liquid (RTD)

- Capsule/Tablets

- Bars/Solid Format

By Distribution Channel

- Online Retail

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Pharmacies & Drugstores

- Direct Sales / Fitness Center Sales

By Consumer Type

- Professional Athletes

- Bodybuilders & Strength Trainers

- Recreational Fitness Enthusiasts

- Lifestyle & Wellness Consumers

- Clinical & Rehabilitation Users

By End-Use Setting

- Home Consumption

- Gyms & Fitness Centers

- Sports Academies & Institutions

- Clinical & Rehabilitation Centers

Regional Insights

North America

North America accounts for nearly 36% of the global market share in 2025, with the United States contributing close to 30% of global revenue. Regional growth is driven by a deeply entrenched sports and fitness culture, high consumer spending power, and strong awareness of protein supplementation benefits. The presence of leading global brands, extensive retail networks, and advanced e-commerce infrastructure further supports market expansion. Additionally, innovation in clean-label, functional, and performance-enhancing formulations continues to stimulate repeat purchases. The region also benefits from widespread gym penetration, collegiate sports participation, and influencer-led marketing strategies that sustain high product visibility.

Europe

Europe represents approximately 24% of the global market, led by Germany, the United Kingdom, and France. Regional growth is driven by increasing demand for clean-label, organic, and plant-based recovery products, reflecting heightened consumer scrutiny regarding ingredient transparency and sustainability. Expanding health consciousness, government-backed fitness initiatives, and a rising aging population seeking muscle maintenance solutions contribute to steady market growth. The region’s well-established regulatory framework also enhances consumer trust and supports premium product positioning. E-commerce adoption and cross-border trade within the European Union further facilitate brand expansion.

Asia-Pacific

Asia-Pacific holds about 28% market share in 2025 and represents the fastest-growing region, expanding at nearly 10% CAGR. Growth is fueled by rapid urbanization, rising disposable incomes, and increasing penetration of organized fitness centers across China and India. Expanding middle-class populations and growing exposure to Western fitness trends through digital platforms are accelerating supplement adoption. Additionally, local manufacturing expansion, celebrity endorsements, and government initiatives promoting sports participation contribute to market development. The region’s young demographic profile and growing e-commerce ecosystems further strengthen long-term growth prospects.

Latin America

Latin America accounts for around 5% of global demand, led by Brazil and Mexico. Regional growth is supported by a strong bodybuilding culture, increasing participation in competitive sports, and expanding social media-driven fitness communities. Rising urbanization and improving retail infrastructure are enhancing product accessibility. Additionally, economic recovery in key markets and growing awareness of nutritional supplementation are supporting gradual market expansion. International brands are increasing regional investments, while domestic players focus on competitively priced offerings to capture price-sensitive consumers.

Middle East & Africa

The Middle East & Africa region contributes nearly 7% of global revenue, driven by rising health awareness in the United Arab Emirates and Saudi Arabia and increasing investments in sports infrastructure. Government-led initiatives promoting active lifestyles, coupled with expanding premium gym chains and international sporting events, are strengthening demand. Growth in expatriate populations and higher disposable incomes in Gulf Cooperation Council countries further support market expansion. In Africa, gradual urbanization and improving retail penetration are creating emerging opportunities, particularly in South Africa and select North African markets.

Key Players in the Post-Workout Supplements Market

- Glanbia plc

- Abbott Laboratories

- Herbalife Ltd.

- Nestlé Health Science

- The Hut Group

- PepsiCo Inc.

- GNC Holdings LLC

- Amway Corp.

- MusclePharm Corporation

- Iovate Health Sciences International

- NOW Foods

- Transparent Labs

- Dymatize Enterprises

- Myprotein

- Optimum Nutrition