Plantain Chips Market Size

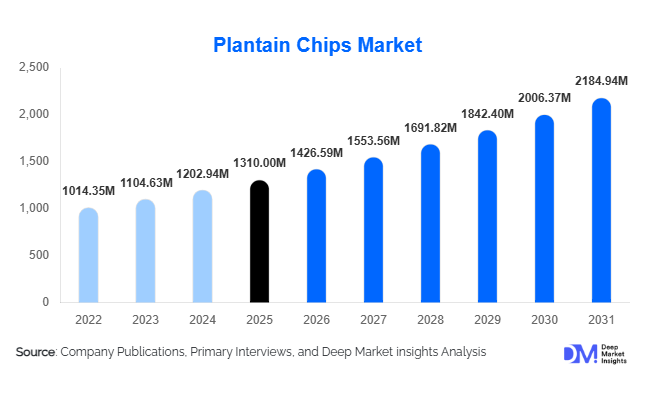

According to Deep Market Insights, the global plantain chips market size was valued at USD 1,310 million in 2025 and is projected to grow from USD 1,426.59 million in 2026 to reach USD 2,184.94 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The plantain chips market growth is primarily driven by rising demand for healthier snack alternatives, increasing consumer preference for gluten-free and ethnic snack products, and the growing popularity of tropical fruit-based snacks across developed and emerging economies.

Key Market Insights

- Plantain chips are increasingly positioned as healthier alternatives to traditional potato chips, supported by rising demand for gluten-free, vegan, and minimally processed snacks.

- Premium and organic plantain chip variants are witnessing strong growth, particularly across North America and Europe where clean-label snacking trends continue expanding.

- North America dominates the global market, driven by strong multicultural food demand and rising adoption of tropical snacks among health-conscious consumers.

- Asia-Pacific is the fastest-growing regional market, supported by urbanization, growing disposable incomes, and expanding organized retail infrastructure.

- Flavor innovation is reshaping competition, with manufacturers launching chili-lime, barbecue, garlic herb, and regional spice variants to differentiate product portfolios.

- Technological advancements such as vacuum frying and air frying are enabling healthier product development with reduced oil absorption and longer shelf life.

Plantain Chips Market Trends

Health-Oriented Snack Innovation Accelerating Market Expansion

The plantain chips industry is increasingly evolving toward health-oriented product innovation as consumers seek alternatives to conventional fried snacks. Manufacturers are introducing baked, air-fried, low-sodium, organic, and non-GMO plantain chips to cater to wellness-focused consumers. Demand for clean-label products has encouraged companies to eliminate artificial preservatives and synthetic flavoring agents while adopting healthier edible oils such as avocado oil and sunflower oil. Premium snacking trends are further encouraging brands to introduce kettle-cooked and artisanal product lines that combine healthier positioning with superior texture and flavor profiles. The growing influence of vegan and gluten-free diets across urban populations is also contributing significantly to category expansion.

Ethnic and Tropical Snack Consumption Becoming Mainstream

Plantain chips are transitioning from regionally consumed ethnic snacks into globally commercialized packaged food products. Rising multicultural food consumption and growing exposure to Caribbean, African, and Latin American cuisines are increasing mainstream demand across supermarkets and convenience stores. Retailers are allocating larger shelf spaces to tropical and alternative snack categories, particularly in North America and Europe. Foodservice operators, cafés, and airlines are also incorporating plantain chips into menus as premium snack alternatives. Social media exposure and digital food content are further strengthening awareness of tropical snacks among younger consumers, contributing to broader product acceptance globally.

Plantain Chips Market Drivers

Rising Demand for Healthier Snack Alternatives

Consumers worldwide are increasingly shifting away from highly processed snacks containing artificial additives, excessive sodium, and trans fats. Plantain chips are benefiting from this trend due to their perception as a healthier, more natural snack alternative. The market is particularly supported by increasing demand for gluten-free, vegan-friendly, and minimally processed foods among millennials and Generation Z consumers. Snack manufacturers are capitalizing on these preferences by expanding healthier product portfolios featuring organic ingredients, reduced oil content, and clean-label positioning. The rapid growth of the global healthy snacks industry continues to positively influence plantain chip demand across both developed and emerging markets.

Expansion of Organized Retail and E-Commerce Channels

The rapid expansion of supermarkets, hypermarkets, and digital grocery platforms has significantly improved product accessibility and brand visibility for plantain chip manufacturers. Online retail channels enable niche snack brands to reach international consumers without requiring extensive traditional retail infrastructure. E-commerce has also accelerated premium product sales by enabling consumers to explore specialty snacks and international food categories more conveniently. Subscription-based snack services, digital marketing campaigns, and influencer-led promotions are increasingly shaping purchasing decisions, particularly among younger urban consumers seeking innovative snacking experiences.

Plantain Chips Market Restraints

Volatility in Raw Material Prices

Plantain cultivation remains highly dependent on climatic conditions, creating significant fluctuations in raw material availability and pricing. Tropical storms, droughts, floods, and crop diseases can negatively affect plantain yields across major producing countries including Colombia, Ecuador, Nigeria, and Peru. Such disruptions increase production costs for manufacturers and create challenges in maintaining stable supply chains. Rising edible oil prices further contribute to cost pressures, impacting profitability across conventional plantain chip product categories.

Regulatory Pressure on Fried Snack Products

Governments across several developed economies are implementing stricter nutritional labeling regulations concerning sodium levels, trans fats, calorie disclosure, and ingredient transparency. Fried snack categories are increasingly scrutinized by health authorities and consumer advocacy groups, encouraging manufacturers to invest heavily in healthier processing technologies such as vacuum frying and air frying. While these technologies improve nutritional profiles, they require significant capital investment and operational upgrades, creating financial barriers particularly for small and medium-sized processors.

Plantain Chips Market opportunities

Premium Organic and Functional Snack Categories

The growing demand for premium healthy snacks presents substantial opportunities for plantain chip manufacturers. Organic, non-GMO, air-fried, and low-sodium variants are increasingly attracting consumers willing to pay premium prices for healthier alternatives. Functional snack positioning incorporating natural ingredients, high fiber content, and clean-label formulations is expected to support strong revenue growth. Companies investing in sustainable packaging, premium seasoning blends, and healthier oils are likely to strengthen market differentiation and improve profitability within premium consumer segments.

Export-Led Expansion from Emerging Economies

Major plantain-producing nations across Latin America and Africa are increasingly expanding food processing capabilities to improve export revenues and agricultural value addition. Governments are supporting agro-processing investments through export incentives, industrial food parks, and SME financing programs. Countries such as Colombia, Ecuador, Peru, and the Dominican Republic are strengthening their export presence across North America and Europe due to favorable raw material availability and competitive manufacturing costs. Growing global demand for tropical and ethnic snacks is expected to create long-term export opportunities for regional processors and international food manufacturers.

Product Type Insights

The global plantain chips market is witnessing substantial product diversification as manufacturers continue expanding offerings to address changing consumer snacking preferences, health awareness, and flavor experimentation trends. Among all product categories, savory and salted plantain chips continue to dominate the market, accounting for nearly 34% of total global revenue share. Their dominance is primarily attributed to broad consumer familiarity, affordable pricing, strong shelf availability, and compatibility with mainstream snacking habits across both developed and emerging economies. Consumers continue to prefer savory variants because they closely resemble traditional potato chips while offering a distinctive tropical flavor profile and perceived nutritional advantages. These products maintain strong penetration across supermarkets, hypermarkets, convenience stores, foodservice outlets, and online retail channels, allowing manufacturers to achieve higher sales volumes and broader market visibility.Organic plantain chips are emerging as one of the fastest-growing premium categories within the global market. Demand for organic variants is especially strong across the United States, Canada, Germany, the United Kingdom, and Nordic countries, where consumers actively prioritize non-GMO ingredients, pesticide-free sourcing, and environmentally sustainable food production. Organic certification not only improves consumer trust but also enables premium pricing opportunities for manufacturers targeting affluent urban consumers. Additionally, the growing popularity of vegan, gluten-free, paleo-friendly, and allergen-free diets continues strengthening demand for plantain chips as an alternative snack product that aligns with specialized nutritional preferences.Packaging innovation is also contributing significantly to product category expansion. Manufacturers are increasingly introducing resealable pouches, portable single-serve packs, family-size packaging, and sustainable packaging solutions to improve convenience and align with evolving urban lifestyles. Portable packaging formats are particularly important among working professionals, students, travelers, and younger consumers who prioritize convenience and on-the-go snacking. Sustainable packaging materials are additionally gaining traction as environmentally conscious consumers increasingly evaluate brands based on sustainability commitments and packaging waste reduction initiatives.

Application Insights

Retail snacking remains the dominant application segment within the global plantain chips market, supported by the rapid expansion of ready-to-eat packaged food consumption worldwide. Increasing urbanization, busier lifestyles, rising dual-income households, and growing preference for convenient snack solutions continue strengthening demand for packaged snack products across both developed and developing economies. Plantain chips are increasingly positioned as healthier alternatives to conventional potato chips due to their natural ingredient profile, gluten-free characteristics, and association with tropical and ethnic food cultures. This positioning has helped manufacturers attract consumers seeking diversified snack experiences while maintaining convenience and affordability.Travel and hospitality applications are emerging as high-growth areas within the plantain chips market. Airlines, premium hotels, resorts, cruise operators, and tourism-focused hospitality providers are increasingly incorporating premium snack assortments into customer service offerings. Plantain chips are benefiting from this trend due to their portability, long shelf life, premium image, and compatibility with diverse consumer dietary preferences. The continued recovery and expansion of international tourism and business travel activity are expected to create additional long-term opportunities for packaged tropical snack products.Institutional demand is also gradually increasing as schools, universities, corporate cafeterias, healthcare facilities, and catering providers diversify snack portfolios to accommodate changing dietary preferences. Plantain chips are increasingly included within healthier vending machine selections and cafeteria snack programs due to growing pressure on institutions to provide better-for-you food alternatives. Additionally, social consumption occasions including parties, sporting events, movie nights, and entertainment gatherings continue contributing significantly to global market demand as flavored and gourmet plantain chip products gain broader acceptance among mainstream consumers.

Distribution Channel Insights

Supermarkets and hypermarkets continue accounting for the largest share of global plantain chip sales, representing approximately 41% of the market in 2025. These retail formats maintain dominance because they provide broad product visibility, extensive shelf space, competitive pricing structures, and convenient access to large consumer populations. Major retail chains across North America, Europe, Asia-Pacific, and Latin America are continuously expanding healthy snack and ethnic food categories to accommodate evolving consumer preferences. Increased shelf allocation for gluten-free, vegan, organic, and premium snack products has significantly improved the visibility and accessibility of plantain chip brands across mainstream retail environments.Online retail channels are currently experiencing the fastest growth across the global plantain chips market. E-commerce platforms, digital grocery services, subscription snack boxes, and direct-to-consumer brand websites are transforming purchasing behavior by improving product accessibility and enabling consumers to discover niche snack categories more efficiently. Online retail growth is especially important for premium, organic, specialty, and imported plantain chip brands that may face shelf space limitations within traditional retail channels. Digital platforms additionally enable manufacturers to improve customer engagement through personalized marketing campaigns, influencer collaborations, social media advertising, and subscription-based purchasing models.Health and wellness stores are also becoming increasingly relevant distribution channels as demand rises for organic, non-GMO, air-fried, and clean-label snack products. Specialty retailers focusing on natural foods continue attracting health-conscious consumers willing to pay premium prices for higher-quality snack alternatives. This trend is particularly prominent across developed economies where wellness-focused consumption patterns continue reshaping the broader packaged food industry.

Consumer Demographic Insights

Millennials and Generation Z consumers represent the largest and fastest-growing demographic segments within the global plantain chips market. These consumer groups exhibit strong preferences for innovative, globally inspired, healthier, and socially conscious food products, making them highly receptive to alternative snack categories. Younger consumers are significantly more willing to experiment with ethnic flavors, tropical ingredients, and unconventional snack formats compared to older generations. Their purchasing decisions are also strongly influenced by social media trends, brand authenticity, sustainability commitments, and clean-label claims.Working professionals also contribute significantly to market demand due to increasing preference for portable snack products suitable for office consumption, commuting, and travel. Busy work schedules and growing urbanization continue encouraging demand for convenient ready-to-eat snacks that require minimal preparation while offering satisfying flavor experiences. Single-serve packaging and resealable pouch formats are particularly popular among this demographic because they support portion control and convenience.Health-conscious consumers continue driving substantial growth across baked, low-sodium, low-fat, organic, and air-fried plantain chip categories. Rising awareness regarding obesity, cardiovascular health, digestive wellness, and artificial ingredient consumption is encouraging consumers to evaluate snack purchases more carefully. Plantain chips benefit from positive consumer perceptions associated with natural ingredients, gluten-free positioning, and lower levels of artificial additives compared to conventional snack alternatives.Household consumption remains the dominant end-use category globally, although younger demographics continue demonstrating faster growth rates due to increasing experimentation with premium snacks and international food products. Families are also increasingly incorporating plantain chips into shared entertainment occasions, lunchbox snacks, and home-based social gatherings, further strengthening long-term market penetration.

| By Product Type | By Processing Method | By Distribution Channel | By Application | By Consumer Demographics |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global plantain chips market in 2025, making it the leading regional market worldwide. The United States dominates regional demand due to increasing multicultural food consumption patterns, strong Hispanic population influence, and rising consumer preference for healthier snack alternatives. Plantain chips have transitioned from niche ethnic products into mainstream snack categories as retailers continue expanding healthier and globally inspired snack assortments.Expanding e-commerce penetration, rising investment in snack innovation, and strong product visibility across major supermarket chains continue supporting regional expansion. Additionally, the growing popularity of Latin American and Caribbean cuisine across North America is further increasing consumer familiarity with plantain-based products. Canada is also witnessing rising adoption of tropical snacks through specialty retailers, multicultural grocery stores, and online distribution platforms.

Europe

Europe represents nearly 24% of global plantain chip market demand, supported by increasing consumer interest in vegan, organic, sustainable, and clean-label snack products. Countries including the United Kingdom, Germany, France, Spain, Italy, and the Netherlands serve as major regional consumption hubs due to expanding multicultural food preferences and growing health awareness.European supermarkets are aggressively expanding private-label healthy snack portfolios to capture growing consumer demand for alternative snack products at competitive price points. Sustainability-focused regulations and retailer initiatives are additionally encouraging manufacturers to adopt recyclable packaging, environmentally responsible sourcing practices, and cleaner production processes. Increasing popularity of ethnic cuisines and international travel exposure are also strengthening consumer familiarity with tropical snack products across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 10% through 2031. China, India, Japan, South Korea, Indonesia, Thailand, Malaysia, and Vietnam are witnessing rapidly increasing demand for premium snack products, international food experiences, and healthier packaged foods.India is emerging as a particularly significant growth market due to extensive banana cultivation, expanding food processing industries, and rising urban snack consumption. Domestic manufacturers are increasingly launching branded plantain chip products across organized retail channels while benefiting from abundant raw material availability. China is experiencing growing imports of premium tropical snacks among younger consumers seeking differentiated snack experiences, while Southeast Asian markets benefit from strong regional familiarity with banana-based snack products. Expanding retail infrastructure, modern trade penetration, and digital commerce adoption continue accelerating long-term market growth across the region.

Latin America

Latin America remains one of the most important production and consumption hubs for plantain chips globally due to extensive plantain cultivation across Colombia, Ecuador, Peru, Guatemala, Venezuela, and the Dominican Republic. Plantain-based snacks are deeply integrated into regional culinary traditions, supporting consistently high domestic consumption levels.Colombia and Ecuador remain among the leading exporters supplying North American and European markets with raw plantains and processed snack products. Governments across the region are increasingly supporting agro-processing industries through agricultural modernization programs, export incentives, rural employment initiatives, and food manufacturing investments. Rising regional urbanization and expanding organized retail infrastructure are additionally improving product distribution and branded snack penetration.

Middle East & Africa

The Middle East & Africa region is witnessing steadily increasing demand for packaged tropical snacks as urbanization, retail modernization, and disposable income growth continue transforming regional food consumption patterns. African countries including Nigeria, Ghana, Kenya, and South Africa benefit from substantial plantain cultivation and expanding domestic snack manufacturing industries.Gulf economies such as the United Arab Emirates and Saudi Arabia are witnessing growing imports of premium snack products driven by rising disposable incomes, expanding expatriate populations, tourism sector growth, and strong demand for international food products. African manufacturers are also increasingly investing in local processing facilities to reduce import dependence and capitalize on rising domestic snack consumption. Continued retail development, improving cold chain logistics, and increasing foreign investment within regional food industries are expected to support long-term plantain chips market expansion across the Middle East & Africa.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Plantain Chips Market

- Chifles Chips

- Inka Crops

- Goya Foods

- Tropical Foods

- Frito-Lay

- Trader Joe’s

- Barnana

- Artisan Tropic

- Iberia Foods

- Turbana Corporation

- Simply7 Snacks

- Sunshine Snacks

- Prime Planet Energy & Foods

- Alimentos Yupi

- GraceKennedy Foods