Plant-Based Infant Formula Market Size

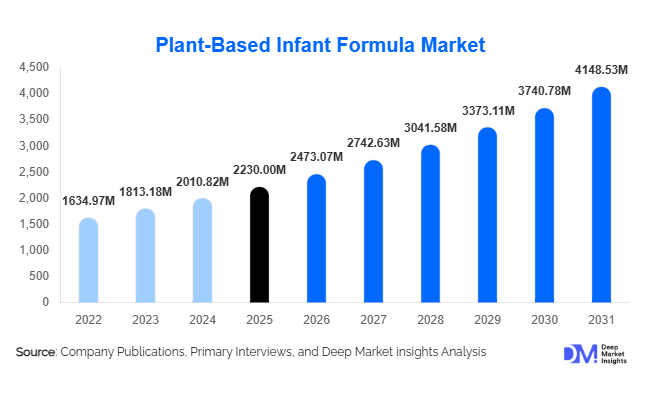

According to Deep Market Insights,the global plant-based infant formula market size was valued at USD 2,230 million in 2025 and is projected to grow from USD 2,473.07 million in 2026 to reach USD 4,148.53 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). The plant-based infant formula market growth is primarily driven by increasing cases of lactose intolerance and cow’s milk protein allergy (CMPA) among infants, rising parental preference for vegan and clean-label nutrition, and advancements in plant protein fortification technologies that enhance nutritional equivalence to dairy-based formulas.

Key Market Insights

- Soy-based formulations dominate the global market, accounting for over 40% of total revenue due to established clinical acceptance and supply chain maturity.

- Stage 1 (0–6 months) formulas represent the largest demand segment, driven by early-life nutritional dependency and pediatric recommendations.

- Premium and organic-certified products account for nearly half of global revenue, reflecting strong brand trust and clean-label demand.

- North America leads the global market, contributing approximately 32% of 2025 revenue, supported by high awareness of plant-based diets.

- Asia-Pacific is the fastest-growing region, expanding at over 13% CAGR due to rising middle-class income and strong imported formula demand in China.

- Online retail is the fastest-growing distribution channel, driven by subscription-based infant nutrition models and cross-border e-commerce.

What are the latest trends in the plant-based infant formula market?

Premiumization and Clean-Label Positioning

Premium and organic-certified plant-based infant formulas are witnessing accelerated growth as parents increasingly scrutinize ingredient transparency, pesticide residues, and GMO content. Clean-label claims such as non-GMO, allergen-free, soy-free alternatives, and sustainable sourcing certifications are becoming key differentiators. Manufacturers are investing in traceable supply chains and ESG-compliant production facilities to strengthen brand equity. Organic pea and rice protein variants are gaining momentum in developed markets, particularly in North America and Europe, where regulatory standards are stringent and consumer trust is closely linked to certification credentials.

Technological Advancements in Plant Protein Fortification

Innovation in hydrolyzed plant protein processing and microencapsulation of nutrients is significantly improving digestibility and bioavailability. Companies are incorporating algae-derived DHA, plant-based ARA, iron, probiotics, and nucleotides to replicate the nutritional profile of traditional dairy formulas. Precision fermentation and enzymatic modification technologies are narrowing performance gaps while enhancing taste and solubility. Clinical validation studies and pediatric endorsements are reinforcing consumer confidence, supporting mainstream adoption beyond niche vegan households.

What are the key drivers in the plant-based infant formula market?

Rising Incidence of Lactose Intolerance and CMPA

Increasing diagnosis of lactose intolerance and cow’s milk protein allergy among infants is a primary growth driver. Pediatricians are increasingly recommending plant-based alternatives as part of allergy management strategies. Growing awareness among parents regarding digestive sensitivities and immune health is translating into sustained demand for soy- and rice-based formulations globally.

Shift Toward Vegan and Flexitarian Lifestyles

The global shift toward plant-based lifestyles among millennials is influencing infant nutrition decisions. Parents adopting vegan or flexitarian diets prefer plant-based continuity in early childhood nutrition. Environmental sustainability concerns and ethical food sourcing further strengthen this transition, particularly in developed economies.

What are the restraints for the global market?

Stringent Regulatory Frameworks

Infant formula products face strict regulatory scrutiny across major markets including the United States, European Union, and China. Extensive clinical validation, safety approvals, and nutritional compliance requirements increase development costs and prolong product launch timelines, acting as a restraint for new entrants.

Premium Pricing and Cost Pressures

Higher production costs associated with plant protein isolation, fortification technologies, and organic certification contribute to premium pricing. In emerging and price-sensitive markets, affordability constraints may limit widespread adoption despite rising awareness.

What are the key opportunities in the plant-based infant formula industry?

Expansion in Asia-Pacific Markets

Asia-Pacific presents significant growth opportunities, particularly in China and India, where rising disposable income and growing awareness of dairy allergies are driving demand. Cross-border e-commerce channels allow international brands to penetrate urban markets efficiently. Premium imported formulas enjoy strong trust among Chinese parents, supporting export-led growth.

R&D Investments in Advanced Nutrition

Investments in fermentation-derived proteins, algae-based omega-3 fortification, and hypoallergenic formulations offer competitive differentiation. Companies that prioritize clinical research and pediatric collaboration are positioned to secure regulatory approvals faster and command premium margins in developed markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2230 Million |

| Market Size in 2026 | USD 2473.07 Million |

| Market Size in 2031 | USD 4148.53 Million |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Type Insights

Soy-based infant formula dominates the global plant-based infant formula market, accounting for approximately 41% of global revenue in 2025. The segment’s leadership is primarily driven by its long-standing clinical validation, broad pediatric acceptance, and relatively complete amino acid composition compared to other plant proteins. Additionally, well-established global soybean supply chains, cost efficiency in large-scale production, and regulatory familiarity across major markets have reinforced its commercial dominance. Healthcare professionals often recommend soy-based formulas for infants with lactose intolerance, further supporting consistent demand. Meanwhile, rice-based and pea-protein formulations are steadily gaining traction as hypoallergenic and easier-to-digest alternatives, particularly for infants with soy sensitivities or multiple food intolerances. Innovation in protein extraction technologies has improved the texture, digestibility, and nutritional density of these alternatives. Multi-plant blends are emerging as premium offerings that combine complementary amino acid profiles, improved gut tolerance, and enhanced micronutrient absorption, appealing to parents seeking diversified plant nutrition solutions.

Infant Stage Insights

Stage 1 (0–6 months) formulas account for nearly 46% of total market revenue in 2025, making it the leading segment due to the critical nutritional dependency of infants during early development. During the first six months, infants rely exclusively on formula or breast milk, which significantly increases consumption frequency and volume compared to later stages. This high consumption intensity, combined with strict pediatric guidance and regulatory oversight for early-life nutrition, drives substantial revenue concentration in Stage 1 products. Stage 2 (6–12 months) and Stage 3 toddler formulas are expanding steadily as parents increasingly extend plant-based dietary practices beyond infancy. Growth in these stages is supported by rising awareness of digestive health, immune support formulations, and fortified nutrient blends tailored to developmental milestones. Pediatric supervision and improved nutritional fortification are enhancing confidence in continued plant-based feeding practices.

Formulation Insights

Fortified plant-based formulas hold approximately 38% market share, representing the leading formulation segment driven by parental demand for complete nutritional equivalence to conventional dairy-based formulas. The inclusion of DHA, ARA, iron, vitamin D, calcium, and probiotic strains is a major growth catalyst, as these nutrients are critical for cognitive development, immune support, and bone health. Scientific advancements in plant-based micronutrient stabilization and bioavailability have strengthened consumer confidence. Organic-certified variants are rapidly expanding within the premium tier, particularly in regions with stringent food safety regulations. Regulatory alignment and certification frameworks in Europe and North America have enhanced transparency and trust, encouraging parents to choose clean-label, non-GMO, and pesticide-free formulations. The convergence of fortification and organic certification is increasingly shaping premium purchasing decisions.

Distribution Channel Insights

Supermarkets and hypermarkets account for about 34% of global sales, making them the dominant distribution channel due to established consumer trust, strong shelf visibility, and immediate product availability. Large retail chains offer extensive product comparisons, promotional pricing strategies, and pharmacist or in-store expert consultations that influence purchasing decisions. However, online retail is the fastest-growing channel, expanding at over 14% CAGR, fueled by subscription-based delivery models, convenience-driven purchasing behavior, and increasing digital trust among millennial parents. Cross-border e-commerce platforms have significantly boosted premium imported formula sales, especially in Asia-Pacific markets. Digital platforms also enable detailed product education, customer reviews, and personalized recommendations, strengthening brand engagement and repeat purchasing behavior.

Price Tier Insights

Premium products represent approximately 49% of global revenue, positioning this as the leading price segment driven by strong brand equity, safety perceptions, and willingness among parents to invest in high-quality infant nutrition. Infant formula purchasing behavior is highly risk-averse, and parents often associate higher prices with superior ingredient sourcing, rigorous testing, and enhanced nutritional profiles. Super-premium organic formulas command even higher margins, particularly in export-driven markets such as China, where imported products are perceived as safer and more reliable. Transparent labeling, advanced clinical validation, and sustainability positioning further reinforce premium pricing power across developed and emerging economies.

Explore more data points, trends and opportunities Download Free Sample Report

Plant-Based Infant Formula Market Segmentations

By Source Type

- Soy-Based Infant Formula

- Rice-Based Infant Formula

- Pea Protein-Based Infant Formula

- Almond-Based Infant Formula

- Oat-Based Infant Formula

- Coconut-Based Infant Formula

- Multi-Plant Blend-Based Infant Formula

By Infant Stage

- Stage 1 (0–6 Months)

- Stage 2 (6–12 Months)

- Stage 3 (12–24 Months / Toddler Formula)

By Formulation Type

- Standard Plant-Based Formula

- Hypoallergenic Formula

- Organic Certified Formula

- Fortified (DHA/ARA, Iron, Probiotics) Formula

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Baby Stores

- Online Retail (E-commerce & D2C)

- Hospital & Institutional Sales

By Packaging Type

- Metal Cans

- Flexible Pouches

- Ready-to-Feed Liquid Bottles

By Price Tier

- Mass-Market

- Premium

- Super-Premium / Organic

Regional Insights

North America

North America accounts for approximately 32% of the 2025 market share, led by the United States, which contributes nearly 78% of regional revenue. Regional growth is driven by high allergy awareness, increasing lactose intolerance diagnoses, and rising adoption of vegan and plant-forward lifestyles among younger parents. Strong regulatory oversight, advanced pediatric healthcare infrastructure, and widespread availability of fortified specialty formulas further support market expansion. Additionally, robust retail networks and mature e-commerce ecosystems enable rapid product accessibility and subscription-based purchasing models. Innovation in clean-label and organic-certified offerings continues to stimulate premium segment growth across the region.

Europe

Europe holds around 29% of global share, with Germany, France, and the UK leading adoption. The region’s growth is supported by stringent organic certification standards, strict infant nutrition regulations, and strong consumer preference for clean-label, sustainably sourced products. European parents exhibit high awareness regarding ingredient transparency, non-GMO sourcing, and environmental sustainability, which drives demand for organic and fortified plant-based formulas. Government-backed food safety frameworks and advanced research in infant nutrition further strengthen consumer trust. The premiumization trend remains particularly strong in Western Europe, where purchasing power and sustainability consciousness are elevated.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 13% CAGR. China dominates regional demand due to strong preference for imported premium infant formulas, heightened food safety concerns, and rising disposable incomes among urban households. Cross-border e-commerce channels significantly contribute to premium product penetration. India and Australia are emerging as important markets, supported by expanding middle-class populations, increasing pediatric awareness of plant-based alternatives, and rising urbanization. In Southeast Asia, improving retail infrastructure and growing exposure to global nutrition trends are accelerating adoption. The region’s large birth cohort and evolving parental preferences toward premium and specialty nutrition collectively drive sustained high growth rates.

Latin America

Latin America represents approximately 6–7% of global revenue, with Brazil and Mexico leading regional demand. Growth is primarily driven by expanding urban middle-class populations, rising female workforce participation, and improving modern retail penetration. Increasing awareness of lactose intolerance and digestive sensitivities among infants is gradually supporting plant-based formula adoption. While price sensitivity remains a constraint, the premium segment is gaining traction in metropolitan areas where consumers demonstrate stronger brand consciousness and health awareness. Continued expansion of pharmacy chains and digital retail platforms is expected to further support regional growth.

Middle East & Africa

The Middle East & Africa region contributes nearly 5% of global revenue, with the UAE and South Africa representing key markets. Regional growth is supported by high reliance on imported premium infant formulas, rising expatriate populations, and increasing disposable incomes in Gulf Cooperation Council countries. Urbanization, expanding modern retail formats, and growing healthcare awareness are gradually strengthening plant-based formula penetration. In Africa, improving distribution networks and rising demand for specialized infant nutrition products are expected to support steady long-term expansion, although affordability remains a critical factor influencing purchasing behavior.

Key Players in the Plant-Based Infant Formula Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Reckitt Benckiser Group plc

- Perrigo Company plc

- Else Nutrition Holdings Inc.

- The Hain Celestial Group, Inc.

- Bellamy’s Organic

- Ausnutria Dairy Corporation Ltd.

- Arla Foods amba

- HiPP GmbH & Co. Vertrieb KG

- Beingmate Co., Ltd.

- Mead Johnson Nutrition

- Sprout Organic Foods

- Bunge Limited