Plant-Based Chocolate Flavor Market Size

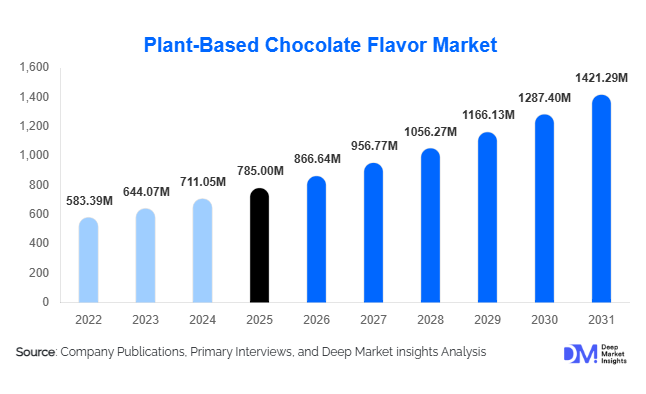

According to Deep Market Insights, the global plant-based chocolate flavor market size was valued at USD 785 million in 2025 and is projected to grow from USD 866.64 million in 2026 to reach USD 1,421.29 million by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of plant-based dairy alternatives, increasing clean-label reformulations in confectionery and beverages, and rising adoption of sustainable cocoa alternatives. Growing consumer preference for vegan, allergen-free, and ethically sourced ingredients is encouraging global food manufacturers to incorporate plant-based chocolate flavors across beverages, bakery, snacks, and nutritional applications. Technological advancements in fermentation-derived cocoa notes and botanical chocolate blends are further strengthening product performance, stability, and scalability across industrial applications.

Key Market Insights

- Powder-based plant chocolate flavors dominate the market, accounting for over 40% share due to ease of storage, transportation, and suitability for protein powders and bakery mixes.

- Dairy alternative applications lead global demand, contributing nearly one-third of total revenue as chocolate remains a preferred flavor in plant-based milk and ice cream.

- North America holds the largest market share, supported by strong vegan product penetration and established plant-based beverage brands.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class consumption and rising dairy substitute adoption in China and India.

- Fermentation-derived chocolate flavors are gaining momentum, offering sustainable alternatives to traditional cocoa supply chains.

- Top five players account for nearly 46% of global revenue, reflecting moderate consolidation and high innovation intensity.

What are the latest trends in the plant-based chocolate flavor market?

Fermentation-Based Cocoa Alternatives Accelerating Adoption

Biotechnology-enabled fermentation is emerging as a transformative trend in the plant-based chocolate flavor market. Manufacturers are investing in precision fermentation to replicate cocoa aroma compounds without relying solely on conventional cocoa farming. This approach reduces exposure to climate-driven cocoa price volatility while enhancing flavor consistency and sustainability credentials. Fermentation-derived flavors also support carbon-neutral and deforestation-free claims, aligning with ESG mandates from multinational food companies. As scalability improves, fermentation platforms are expected to shift from niche innovation to mainstream ingredient sourcing.

Clean-Label and Allergen-Free Reformulation

Food and beverage brands are reformulating product lines to eliminate artificial additives and dairy-derived components. Plant-based chocolate flavors certified as non-GMO, organic, and allergen-free are witnessing accelerated adoption in beverages, protein supplements, and baked goods. Consumers increasingly scrutinize ingredient lists, prompting brands to adopt botanical extracts and natural cocoa-derived plant flavors with transparent sourcing. Clean-label positioning is enabling premium pricing while strengthening consumer trust across developed markets.

What are the key drivers in the plant-based chocolate flavor market?

Rapid Growth of Plant-Based Dairy Alternatives

The expansion of plant-based milk, yogurt, and ice cream categories is a primary driver. Chocolate consistently ranks among the top flavor choices in dairy alternatives, ensuring stable ingredient demand. With plant-based dairy recording double-digit growth globally, chocolate flavor suppliers are securing long-term supply agreements with beverage manufacturers. Innovation in oat, almond, soy, and pea-based formulations is further diversifying application scope.

Sustainability and Ethical Sourcing Imperatives

Volatility in traditional cocoa supply chains, particularly due to climate impacts in West Africa, is encouraging manufacturers to diversify sourcing. Plant-based and fermentation-derived chocolate flavors provide cost predictability and sustainability advantages. Food companies are integrating fair-trade certifications, carbon labeling, and deforestation-free commitments into procurement strategies, strengthening long-term demand visibility for sustainable flavor solutions.

What are the restraints for the global market?

Higher Production and Certification Costs

Organic-certified and fermentation-derived plant-based chocolate flavors involve higher production and R&D costs compared to synthetic alternatives. Premium pricing may limit adoption among price-sensitive manufacturers, particularly in emerging markets.

Flavor Authenticity and Technical Challenges

Replicating the depth and complexity of traditional cocoa remains technically demanding. Inconsistent sensory performance across applications may slow substitution in premium confectionery, requiring continued investment in flavor chemistry and encapsulation technologies.

What are the key opportunities in the plant-based chocolate flavor industry?

Expansion into Functional and Sports Nutrition

Protein powders, meal replacements, and fortified beverages represent high-growth applications. Chocolate remains a dominant flavor in sports nutrition, and plant-based formulations align well with vegan athlete trends. Suppliers offering heat-stable, high-intensity chocolate flavors tailored to protein matrices can capture significant value.

Emerging Asia-Pacific Demand

China, India, and Southeast Asia are witnessing rapid adoption of plant-based beverages. Localization of flavor profiles and regional manufacturing investments can unlock cost efficiencies and accelerate market penetration. Strategic partnerships with regional beverage brands present strong growth potential.

Form Insights

Powder-based plant chocolate flavors dominate the global market, accounting for approximately 42% of total revenue share in 2025. The segment’s leadership is primarily driven by its extended shelf life, superior storage stability, and lower transportation and handling costs compared to liquid formats. Powder variants are highly compatible with dry beverage mixes, protein powders, instant cocoa blends, bakery premixes, and meal replacement formulations, making them particularly attractive to large-scale food manufacturers seeking cost-efficient and scalable flavor solutions. In addition, powder-based systems provide improved dosing accuracy and reduced microbial risk, which further enhances their adoption in industrial processing environments.

Liquid concentrates represent the second-largest segment, widely preferred in ready-to-drink beverages, plant-based milk formulations, and flavored syrups due to ease of blending and uniform flavor dispersion. Their ability to integrate seamlessly into high-moisture applications supports demand from beverage manufacturers focusing on rapid production cycles. Meanwhile, encapsulated plant chocolate flavors are gaining traction as a technologically advanced sub-segment, offering improved flavor stability under high-temperature processing conditions such as extrusion, baking, and UHT treatment. Encapsulation also enables controlled flavor release, enhancing sensory consistency and extending product shelf life, which is increasingly valued in functional and fortified food products.

Source Insights

Cocoa-derived plant-certified chocolate flavors hold the largest market share, contributing nearly 48% of total revenue in 2025. The leading position of this segment is driven by authentic taste replication, established global supply chains, and strong consumer trust associated with cocoa-based ingredients. Manufacturers favor cocoa-derived variants due to their proven sensory acceptance and compatibility with clean-label positioning strategies. Furthermore, sustainability certifications and traceable sourcing initiatives have strengthened the commercial viability of cocoa-based plant flavors in developed markets.

Fermentation-derived chocolate flavors represent the fastest-growing sub-segment, supported by their sustainability advantages, reduced dependence on traditional cocoa cultivation, and improved scalability through biotechnology-driven production methods. These solutions address concerns related to cocoa price volatility and climate risks, making them increasingly attractive for long-term procurement strategies. Carob-based alternatives are witnessing moderate growth, particularly in cost-sensitive markets where manufacturers seek economical substitutes without significantly compromising flavor profile. Carob’s naturally sweet characteristics and caffeine-free positioning also contribute to its niche adoption across health-oriented product categories.

Application Insights

Dairy alternatives lead the application landscape, accounting for approximately 31% of total market share in 2025. The segment’s dominance is driven by the rapid expansion of plant-based milk, yogurt, ice cream, and creamers, where chocolate remains one of the most preferred flavors among consumers. The growing shift toward lactose-free and vegan diets, coupled with product innovation in almond, oat, soy, and coconut-based beverages, continues to reinforce demand for plant-certified chocolate flavor solutions.

Bakery and confectionery applications follow closely, benefiting from the rising popularity of vegan cakes, cookies, brownies, and chocolate-coated snacks. Nutritional and functional foods represent a high-growth segment, driven by increasing consumption of protein-enriched beverages, meal replacement shakes, and fortified snack bars where chocolate serves as a masking and enhancing flavor. Snacks and cereals are emerging as secondary yet promising growth channels, particularly in North America and Europe, where manufacturers are launching indulgent yet plant-based breakfast and snacking options to meet evolving consumer preferences.

Distribution Channel Insights

Direct sales to food and beverage manufacturers account for nearly 55% of total revenue, reflecting the preference of global brands for long-term supply agreements with established flavor houses. This channel ensures formulation customization, quality assurance, and supply chain reliability, which are critical for large-scale production. Strategic partnerships between ingredient suppliers and multinational food processors further reinforce this segment’s leadership.

Ingredient distributors remain important in emerging markets, providing regional reach, smaller batch supply, and technical support for local manufacturers. Additionally, online B2B platforms are gradually expanding access for small and mid-sized enterprises by offering transparent pricing, simplified procurement processes, and broader ingredient portfolios. Digitalization of ingredient sourcing is expected to accelerate over the forecast period, particularly in Asia-Pacific and Latin America.

| By Form | By Source | By Application | By Nature | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, led by the United States, which dominates regional demand due to strong penetration of plant-based beverages, high consumer awareness regarding clean-label ingredients, and widespread availability of dairy alternatives across retail channels. Continuous product innovation in ready-to-drink plant-based beverages and functional foods further drives flavor demand. Canada contributes significantly through growing demand for organic-certified flavors and expansion of premium dairy alternative brands. Robust distribution infrastructure, strong presence of global flavor manufacturers, and advanced food processing capabilities continue to support regional growth.

Europe

Europe accounts for nearly 29% of global revenue, with Germany, the United Kingdom, and France leading consumption. Regional growth is driven by stringent sustainability regulations, high demand for ethically sourced ingredients, and strong adoption of vegan and flexitarian diets. Government policies promoting environmental responsibility and transparent labeling practices further accelerate plant-certified ingredient usage. Europe also leads in organic-certified plant-based flavor imports, supported by mature retail networks and consumer willingness to pay premium prices for sustainable and clean-label products.

Asia-Pacific

Asia-Pacific represents around 24% of global revenue and is the fastest-growing region, expanding at a CAGR exceeding 12%. China and India serve as key growth engines, supported by expanding plant-based milk markets, rapid urbanization, rising disposable incomes, and increasing Western-style bakery consumption. Growing health awareness and lactose intolerance prevalence also stimulate dairy alternative demand. Japan and Australia remain innovation-driven markets with strong emphasis on premium formulations and functional beverages. The region’s expanding manufacturing base and improving cold-chain infrastructure further strengthen market penetration.

Latin America

Latin America contributes approximately 8% of global market share, with Brazil and Mexico leading regional demand. Growth is supported by expanding bakery and beverage industries, increasing middle-class population, and gradual adoption of plant-based dairy alternatives. Local cocoa production in certain countries provides strategic sourcing advantages, while improving retail penetration enhances availability of flavored plant-based products. Economic stabilization and rising health-conscious consumption trends are expected to further support regional expansion.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of the global market, with the UAE and South Africa emerging as niche premium markets. Demand remains largely import-driven, supported by expanding modern retail infrastructure, growth in the beverage sector, and increasing exposure to international plant-based brands. Rising tourism, urbanization, and premium product positioning contribute to steady growth in the Gulf countries, while improving food manufacturing capabilities in select African economies create gradual long-term opportunities.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|