Pickles and Pickle Product Market Size

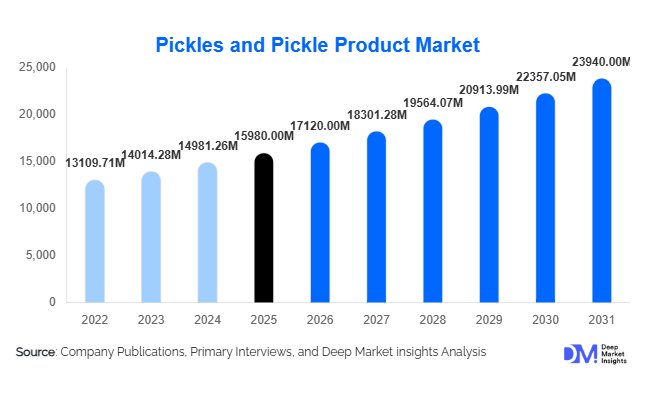

According to Deep Market Insights, the global pickles and pickle product market size was valued at USD 15,980 million in 2025 and is projected to grow from USD 17,120.60 million in 2026 to reach USD 23,940.32 million by 2031, expanding at a CAGR of 6.9% during the forecast period (2026–2031). Market expansion is primarily driven by rising global demand for fermented foods, increasing consumption of convenience meals, and the growing popularity of ethnic and regional cuisines across developed and emerging economies. The increasing consumer inclination toward probiotic-rich and naturally preserved foods is further strengthening market demand.

Key Market Insights

- Fermented and probiotic pickles are gaining popularity as consumers increasingly associate them with digestive health and immunity benefits.

- Asia-Pacific dominates global consumption, supported by strong cultural integration of pickled foods in daily diets across India, China, Korea, and Japan.

- Premium and artisanal pickle brands are expanding rapidly, driven by clean-label and organic food preferences.

- Retail modernization and e-commerce penetration are improving global accessibility of regional pickle varieties.

- Foodservice demand is rising, especially from quick-service restaurants integrating pickled ingredients into burgers, sandwiches, and fusion cuisine.

- Packaging innovation, including resealable pouches and glass alternatives, is improving shelf life and logistics efficiency.

What are the latest trends in the pickles and pickle product market?

Rise of Functional and Fermented Foods

Global dietary trends increasingly favor fermented foods due to perceived gut-health benefits. Traditional fermentation processes used in kimchi, sauerkraut, and regional vegetable pickles are being repositioned as functional foods. Manufacturers are highlighting probiotic content, natural fermentation, and reduced preservatives to appeal to health-conscious consumers. This trend is particularly strong in North America and Europe, where fermented food adoption has accelerated alongside wellness-focused diets.

Premiumization and Regional Flavor Expansion

Consumers are increasingly seeking authentic global flavors, leading to strong growth in premium pickle offerings such as gourmet olives, artisanal cucumber pickles, Korean kimchi varieties, and Indian regional achar products. Small-batch production, organic ingredients, and traditional recipes are becoming key differentiation factors. Retailers are expanding international food aisles, while private-label brands are introducing localized flavors to capture evolving taste preferences.

What are the key drivers in the pickles and pickle product market?

Growing Demand for Convenience Foods

Urban lifestyles and rising dual-income households are increasing consumption of ready-to-eat meals and quick meal accompaniments. Pickles serve as low-cost flavor enhancers that extend meal variety without preparation time. Their long shelf life and compatibility with processed foods make them an essential category within packaged foods globally.

Expansion of Quick-Service Restaurants (QSRs)

The global expansion of burger chains, sandwich outlets, and fast-casual restaurants has significantly increased industrial demand for pickled cucumbers, onions, and jalapeños. Pickled ingredients enhance flavor profiles while maintaining cost efficiency and consistency across large foodservice networks.

Health Awareness Supporting Fermented Products

Consumers increasingly recognize fermented vegetables as natural sources of beneficial bacteria. Low-calorie positioning and clean-label claims are encouraging adoption among health-conscious consumers, particularly millennials and urban populations.

What are the restraints for the global market?

High Sodium Content Concerns

Traditional pickling methods rely heavily on salt and vinegar, creating challenges amid rising health concerns related to sodium intake. Regulatory pressure and consumer awareness are pushing manufacturers to reformulate products, sometimes impacting taste stability.

Raw Material Price Volatility

Fluctuations in vegetable prices—particularly cucumbers, cabbage, mangoes, and peppers—affect production costs. Climate variability and agricultural supply disruptions increase pricing uncertainty, impacting manufacturer margins.

What are the key opportunities in the pickles and pickle product industry?

Expansion into Emerging Markets

Urbanization across Southeast Asia, Africa, and Latin America is creating new demand for packaged condiments. Organized retail growth and rising disposable income allow branded pickle manufacturers to replace traditional unorganized markets with standardized packaged products.

Clean-Label and Organic Product Development

Organic pickles made without artificial preservatives present strong growth opportunities. Consumers increasingly prefer natural fermentation methods and traceable ingredient sourcing, enabling premium pricing strategies and brand differentiation.

Technology Integration in Production and Packaging

Automation, controlled fermentation systems, and advanced packaging technologies are improving consistency, scalability, and export viability. Modified atmosphere packaging and recyclable containers also align with sustainability initiatives, creating long-term competitive advantages.

Product Type Insights

The global pickle market demonstrates strong diversification across product categories; however, vegetable-based pickles continue to dominate overall consumption patterns, accounting for nearly 48% of global market share in 2025. This leadership is primarily supported by the widespread acceptance of cucumber pickles across both developed and emerging economies. Their versatility in sandwiches, burgers, salads, and quick-service restaurant (QSR) menus ensures consistent demand from both retail and foodservice sectors. Additionally, large-scale industrial processing capabilities, longer shelf stability, and standardized flavor profiles make vegetable pickles highly scalable for multinational manufacturers. The leading segment driver for vegetable-based pickles is their integration into global fast-food ecosystems and daily meal consumption habits, particularly in North America and Europe where pickles serve as staple condiments.Fruit-based pickles, especially mango varieties, maintain strong cultural relevance across Asia-Pacific and Middle Eastern markets. These products benefit from deep-rooted culinary traditions and household preservation practices, which sustain steady baseline demand. Increasing commercialization of traditional recipes by organized food brands is further expanding availability through modern retail channels. Meanwhile, premium fruit pickle variants featuring reduced oil content, organic ingredients, and artisanal preparation methods are attracting urban consumers seeking authentic regional flavors.Fermented pickles represent the fastest-growing product category, driven by increasing consumer awareness of gut health, microbiome balance, and functional foods. Rising demand for probiotic-rich diets has positioned fermented products such as kimchi, sauerkraut, and naturally fermented cucumbers as health-oriented alternatives to conventional preserved foods. The leading growth driver within this segment is the convergence of traditional fermentation techniques with modern wellness trends, enabling manufacturers to market pickles as functional nutritional products rather than simple condiments.Vinegar-based pickles continue to dominate Western markets due to their consistency, predictable taste profiles, and compatibility with industrial-scale production systems. Food safety reliability, extended shelf life, and cost efficiency remain key factors sustaining demand, particularly among private-label supermarket brands and foodservice operators requiring standardized supply chains.

Application Insights

Household consumption remains the largest application segment, contributing approximately 55% of total market demand in 2025. The dominance of this segment is supported by daily dietary incorporation of pickles across Asia, Eastern Europe, and the Middle East, where they function as flavor enhancers accompanying staple foods such as rice, bread, and meat-based dishes. The leading segment driver is habitual consumption rooted in cultural food practices combined with increasing availability of packaged, ready-to-consume pickle products that reduce preparation time for consumers.Foodservice applications are expanding rapidly as global QSR chains, casual dining restaurants, and street-food vendors increasingly incorporate pickled ingredients to enhance flavor complexity and menu differentiation. Burgers, wraps, tacos, sandwiches, and fusion cuisine concepts rely heavily on pickled vegetables for texture contrast and acidity balance. Growth is further supported by standardized supply agreements between pickle manufacturers and large restaurant chains, ensuring volume stability.Industrial applications are also witnessing steady expansion, particularly within ready-meal manufacturing, packaged sandwiches, frozen snacks, and meal-kit solutions. Food processors increasingly use pickled ingredients as functional components that improve taste longevity while reducing the need for artificial preservatives. Rising global demand for convenience foods and longer shelf-life packaged meals continues to strengthen this segment’s contribution to overall market expansion.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 46% of global sales, maintaining leadership due to high product visibility, diversified brand assortments, and consumer preference for one-stop shopping experiences. The leading segment driver is strong shelf placement combined with impulse purchasing behavior, particularly for condiment and accompaniment products that consumers frequently purchase alongside staple groceries. Private-label expansion by large retail chains is also increasing affordability and accessibility across price-sensitive markets.Online retail represents the fastest-growing distribution channel, registering double-digit growth rates as consumers increasingly adopt digital grocery platforms. Direct-to-consumer specialty pickle brands are leveraging e-commerce to introduce niche flavors, regional varieties, and health-focused fermented products to wider audiences. Subscription-based food delivery models and improved cold-chain logistics are further enabling expansion of premium and refrigerated pickle categories.Traditional grocery stores and local retail outlets continue to play a critical role in emerging economies, where purchasing behavior remains highly localized and relationship-driven. Small retailers provide access to regionally produced pickles and freshly prepared varieties that appeal to consumers seeking traditional taste profiles. Their continued relevance is supported by proximity-based shopping habits and strong penetration in rural and semi-urban markets.

End-Use Insights

The household sector continues to dominate overall end-use demand, supported by consistent daily consumption patterns and increasing availability of packaged products tailored for smaller family units and urban lifestyles. However, foodservice represents the fastest-growing end-use category, with an estimated annual growth rate exceeding 8%. The leading driver for this segment is the rapid global expansion of QSR chains and casual dining establishments, which rely heavily on pickled ingredients to standardize flavor profiles across locations.Growing consumption of burgers, wraps, sandwiches, and globally inspired fusion foods has significantly increased institutional demand for bulk pickle supplies. Additionally, export-driven consumption is gaining momentum, particularly for kimchi from South Korea and Indian pickles supplied to diaspora populations across North America, Europe, and the Middle East. International migration patterns and cultural food nostalgia are reinforcing cross-border demand.Processed food manufacturers are increasingly integrating pickled components into ready-to-eat meals, frozen foods, salad kits, and snack products. This integration not only enhances flavor complexity but also contributes to product differentiation in competitive packaged food categories. As convenience-driven consumption continues rising globally, industrial end-use demand is expected to expand steadily.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global pickle market with approximately 41% market share in 2025, supported by deeply embedded culinary traditions across countries such as India, China, Japan, and South Korea. Pickles are consumed daily as essential accompaniments rather than occasional condiments, ensuring stable baseline demand. Regional growth is driven by rapid urbanization, rising disposable incomes, and increasing adoption of packaged and branded food products. Expansion of organized retail networks and e-commerce grocery platforms is improving accessibility to commercially packaged pickles. Additionally, growing health awareness is accelerating demand for fermented varieties such as kimchi and tsukemono, while export opportunities for traditional Asian pickles continue expanding globally.

North America

North America accounts for nearly 23% of global demand, led primarily by the United States where cucumber pickles are integral components of fast-food culture. Regional growth is driven by high consumption within QSR chains, strong penetration of private-label retail brands, and increasing consumer interest in functional and probiotic foods. The rising popularity of fermented products aligned with gut-health trends is reshaping product innovation strategies. Additionally, premiumization trends, including artisanal flavors, organic ingredients, and low-sodium formulations, are encouraging value growth across mature markets.

Europe

Europe demonstrates stable and mature demand supported by longstanding culinary traditions in countries such as Germany, Poland, and France. Eastern Europe continues to generate high consumption volumes due to traditional home-style diets incorporating pickled vegetables regularly. Western Europe, meanwhile, drives innovation through organic, clean-label, and gourmet pickle offerings. Regional growth is supported by increasing consumer preference for natural preservation methods, sustainability-focused packaging, and locally sourced ingredients. Expansion of specialty food retailers and premium supermarket segments is further accelerating value-based growth across the region.

Middle East & Africa

The Middle East & Africa region is witnessing rising demand driven by rapid urban population growth, expanding hospitality sectors, and increasing exposure to international cuisines. Countries such as Turkey, Saudi Arabia, and the UAE demonstrate strong consumption across both retail and foodservice channels. Regional growth drivers include expansion of modern retail infrastructure, rising tourism activity, and increasing reliance on imported packaged foods. Local manufacturers are also scaling production to meet demand from restaurants and catering services, particularly as dining-out culture expands across urban centers.

Latin America

Latin America represents an emerging growth region led by Brazil and Mexico, where expanding retail infrastructure and Western dietary influence are reshaping consumption habits. Growth is supported by increasing penetration of supermarkets, rising disposable income levels, and growing demand for convenience foods. Fast-food expansion and evolving urban lifestyles are encouraging adoption of pickled condiments within everyday meals. While overall growth remains moderate compared to Asia-Pacific, accelerating processed food consumption and product innovation are expected to strengthen regional market momentum over the forecast period.

Investment & CapEx Trends

Governments are supporting food processing industries through agricultural modernization initiatives and export promotion programs. Policies such as India’s food processing incentives and China’s manufacturing modernization initiatives are encouraging pickle production scale-up. Private investments are focused on automated fermentation facilities, packaging upgrades, and cold-chain improvements. Food manufacturers are increasing CapEx toward sustainable packaging and production efficiency to meet export standards.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Pickles and Pickle Product Market

- Kraft Heinz Company

- Conagra Brands Inc.

- McCormick & Company Inc.

- Del Monte Foods Inc.

- Mt. Olive Pickle Company

- B&G Foods Inc.

- Best Maid Products Inc.

- Reitzel SA

- Orkla ASA

- Hengstenberg GmbH & Co. KG

- Tokyo Pickling Co., Ltd.

- Desai Foods Pvt. Ltd.

- Nilons Enterprises Pvt. Ltd.

- Patak’s (AB World Foods)

- Kimchi Corporation Korea