Pickleball Equipment Market Size

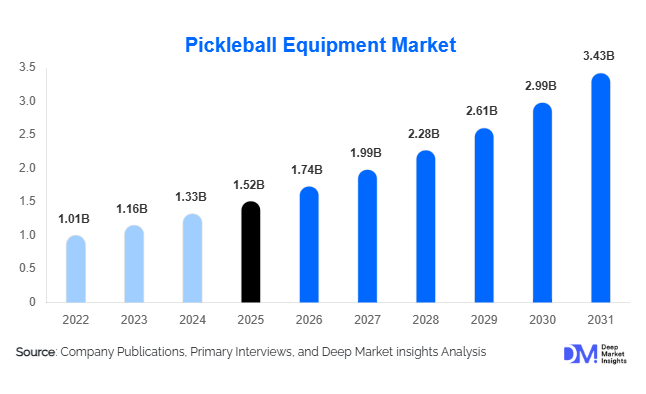

According to Deep Market Insights, the global pickleball equipment market size was valued at USD 1.52 billion in 2025 and is projected to grow from USD 1.74 billion in 2026 to reach USD 3.43 billion by 2031, expanding at a CAGR of 14.5% during the forecast period (2026–2031). The pickleball equipment market growth is primarily driven by the rapid increase in global pickleball participation, rising investments in sports infrastructure, growing popularity of professional pickleball leagues, and continuous innovation in paddle materials and performance-enhancing accessories. As pickleball evolves from a recreational activity into a competitive mainstream sport, demand for premium paddles, specialized footwear, balls, nets, and training accessories continues to accelerate across both developed and emerging markets.

Key Market Insights

- Pickleball is among the fastest-growing sports globally, creating sustained demand for paddles, balls, footwear, and court equipment across recreational and professional segments.

- Carbon fiber and thermoformed paddles are transforming the premium equipment segment, enabling manufacturers to increase average selling prices and margins.

- North America dominates the global market, accounting for approximately 63% of total equipment revenues, led by strong participation growth in the United States.

- Asia-Pacific is the fastest-growing regional market, supported by increasing adoption in India, China, Japan, South Korea, and Australia.

- Institutional demand from schools, clubs, municipalities, and hospitality operators is emerging as a significant revenue stream for equipment manufacturers.

- E-commerce and direct-to-consumer sales channels are reshaping purchasing behavior by improving product accessibility and accelerating international market penetration.

Pickleball Equipment Market Trends

Premium Paddle Technologies Driving Product Upgrades

The pickleball equipment industry is witnessing a strong shift toward premium paddle technologies. Manufacturers are investing heavily in carbon fiber faces, thermoformed construction methods, polymer honeycomb cores, and vibration-reduction systems to improve player performance. Advanced paddles offer superior spin generation, control, durability, and power, making them increasingly attractive to competitive and recreational players alike. As consumer awareness of performance benefits increases, many players are upgrading equipment more frequently than in traditional racket sports. This premiumization trend is expanding average selling prices across the industry and creating higher-margin opportunities for manufacturers. Brands are also introducing signature professional-athlete paddle lines, further strengthening consumer engagement and accelerating replacement cycles.

Expansion of Organized Pickleball Infrastructure

Dedicated pickleball courts, sports complexes, and club facilities are expanding rapidly worldwide. Municipal governments, private sports operators, educational institutions, and hospitality companies are investing in new court construction to accommodate growing participation rates. The increasing availability of dedicated playing facilities is encouraging greater equipment purchases and recurring replacement demand. Hotels, resorts, and residential communities are also integrating pickleball amenities to attract active consumers and sports-focused travelers. This infrastructure expansion is helping transform pickleball from a niche recreational activity into a mainstream sporting category with long-term growth potential.

Pickleball Equipment Market Drivers

Rapid Growth in Global Participation Rates

One of the strongest growth drivers for the pickleball equipment market is the significant increase in participation across multiple age groups. Originally popular among older adults, pickleball has gained substantial traction among younger consumers, families, and competitive athletes. Its accessibility, low learning curve, and social nature make it attractive to a broad demographic base. As new players enter the sport, demand for paddles, balls, nets, footwear, and training equipment continues to expand. The proliferation of local leagues, tournaments, and community programs further supports equipment sales and market growth.

Professionalization of the Sport

The emergence of professional pickleball leagues, sponsorship agreements, media coverage, and celebrity endorsements has elevated the sport's visibility globally. Competitive players increasingly seek advanced equipment that meets tournament standards and enhances performance. Professional events are influencing consumer purchasing behavior, particularly in premium paddle categories where athletes often serve as product ambassadors. This trend is strengthening brand recognition and creating opportunities for premium product differentiation.

Pickleball Equipment Market Restraints

Intense Market Fragmentation and Competitive Pressure

The paddle segment remains highly fragmented, with hundreds of brands competing for market share. While this promotes innovation, it also creates significant pricing pressure and margin challenges. Smaller manufacturers often struggle to differentiate products in an increasingly crowded marketplace, leading to discounting and promotional activity that can impact profitability.

Regulatory Compliance and Equipment Certification Challenges

Tournament governing bodies frequently update equipment standards and certification requirements. Manufacturers must continually invest in testing, compliance, and product redesign to maintain eligibility for competitive play. Sudden regulatory changes can create inventory risks and increase operational costs, particularly for smaller brands with limited product portfolios.

Pickleball Equipment Market Opportunities

Expansion into Emerging International Markets

While North America currently dominates the pickleball equipment industry, significant opportunities exist in Europe, Asia-Pacific, Latin America, and the Middle East. Countries such as India, China, Germany, Spain, Japan, and the United Kingdom are witnessing growing participation rates and increasing investments in court infrastructure. Manufacturers that establish early distribution networks and localized marketing strategies can secure long-term competitive advantages as these markets mature. Emerging economies also present opportunities for affordable and mid-range product offerings that cater to first-time participants.

Institutional and Commercial Equipment Demand

Sports clubs, schools, universities, municipal recreation centers, resorts, and corporate wellness programs are becoming important equipment buyers. Unlike individual consumers, institutional purchasers often procure paddles, balls, nets, and accessories in large volumes. As governments promote physical activity and organizations invest in recreational facilities, commercial demand is expected to generate recurring revenue opportunities for equipment suppliers. The hospitality sector represents a particularly attractive segment as resorts increasingly incorporate pickleball courts into their guest experiences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.52 Billion |

| Market Size in 2026 | USD 1.74 Billion |

| Market Size in 2031 | USD 3.43 Billion |

| CAGR | 14.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Paddles dominate the global pickleball equipment market, accounting for approximately 42% of total revenues in 2025, making them the largest product category worldwide. The segment’s leadership is primarily driven by higher average selling prices compared to other equipment categories, frequent product replacement cycles, and continuous innovation in paddle materials and construction technologies. Consumers increasingly upgrade from entry-level wooden and composite paddles to premium graphite and carbon fiber models that offer enhanced control, power, spin generation, and durability. The growing popularity of competitive and tournament-level pickleball is further accelerating demand for high-performance paddles, particularly among club and professional players who frequently replace equipment to maintain optimal performance. Manufacturers are also introducing thermoformed paddle designs, elongated paddle shapes, and advanced honeycomb polymer core technologies, contributing to higher consumer spending and market value growth.

Balls represent the second-largest product segment and benefit from recurring replacement demand, as balls experience wear and performance degradation with regular use. Growth in organized leagues, tournaments, and recreational participation continues to generate steady consumption volumes globally. Nets and court equipment are witnessing robust demand as governments, municipalities, schools, and private sports clubs invest in dedicated pickleball court construction and facility expansion projects. Meanwhile, specialized pickleball footwear is emerging as one of the fastest-growing product categories, driven by increasing awareness regarding injury prevention, lateral stability, court traction, and player comfort. Accessories including overgrips, grip tapes, equipment bags, protective eyewear, knee supports, and wearable performance tracking devices continue to gain traction as players seek personalized equipment solutions and enhanced playing experiences.

Player Category Insights

Recreational players accounted for approximately 58% of global pickleball equipment demand in 2025, making them the largest consumer segment across the industry. The dominance of this category is largely attributable to the sport’s accessibility, relatively low learning curve, and appeal across multiple age groups. Unlike many traditional racket sports, pickleball requires minimal training and can be played competitively or socially, encouraging rapid participation growth among beginners, families, retirees, and casual sports enthusiasts. The increasing availability of public courts and community programs has further expanded the recreational player base, generating substantial demand for entry-level and mid-range equipment.

Club players represent a rapidly expanding segment as dedicated pickleball clubs, leagues, and recreational associations continue to grow across North America, Europe, and Asia-Pacific. These players typically demonstrate higher equipment spending and more frequent replacement behavior than recreational users. Tournament participants are increasingly driving demand for premium paddles and performance-oriented accessories as competitive play becomes more widespread. Although professional players account for a relatively small share of total equipment sales, they exert a significant influence on product innovation and purchasing decisions through sponsorship agreements, athlete endorsements, and social media visibility. The continued professionalization of the sport is expected to accelerate equipment upgrades across all player categories over the forecast period.

Distribution Channel Insights

Sporting goods retailers remain the leading distribution channel, accounting for approximately 33% of global market revenues in 2025. Their continued dominance is supported by consumers’ preference for evaluating paddle weight, grip texture, balance, and construction quality before making purchasing decisions. Physical retail stores also benefit from expert staff recommendations, product demonstrations, and immediate product availability, which are particularly valuable for first-time buyers and recreational participants.

However, online channels are rapidly transforming the competitive landscape. E-commerce platforms are benefiting from broader product selection, competitive pricing structures, direct customer reviews, and greater accessibility in emerging markets. Brand-owned direct-to-consumer websites are becoming increasingly important as manufacturers seek to improve margins, strengthen customer relationships, and gather consumer insights through digital engagement. Specialty pickleball retailers are also gaining market share in mature markets by offering personalized product consultations, paddle testing programs, equipment customization services, and community-building initiatives. As pickleball participation expands internationally, omnichannel retail strategies that combine physical retail experiences with digital convenience are expected to become a key competitive differentiator.

End-User Insights

Individual consumers accounted for approximately 64% of global pickleball equipment demand in 2025, making them the largest end-user segment. The growth of recreational participation, rising consumer awareness, and increasing adoption among younger demographics continue to support strong retail demand across all major equipment categories. Individual consumers typically drive sales of paddles, balls, footwear, and accessories, while premium equipment purchases are becoming increasingly common as players advance their skill levels.

Sports clubs and academies represent one of the fastest-growing institutional end-user segments due to rising membership enrollment, structured coaching programs, and expanding league participation. Educational institutions are increasingly incorporating pickleball into physical education curricula and extracurricular sports activities, creating long-term demand for paddles, balls, and portable net systems. Hospitality operators, resorts, and residential communities are emerging as important growth drivers as pickleball becomes a sought-after recreational amenity among active consumers and sports-focused travelers. Corporate wellness programs are also contributing to market expansion, with employers adopting pickleball as a team-building and employee engagement activity. These institutional segments typically purchase equipment in bulk quantities, creating recurring revenue opportunities for manufacturers and distributors.

Explore more data points, trends and opportunities Download Free Sample Report

Pickleball Equipment Market Segmentations

By Product Type

- Paddles

- Balls

- Nets & Court Equipment

- Footwear

- Bags & Storage

- Protective & Performance Accessories

By Player Category

- Recreational Players

- Club Players

- Tournament Players

- Professional Players

By Price Segment

- Economy

- Mid-Range

- Premium

- Professional/Elite

By Material Technology

- Wood-Based Equipment

- Polymer Composite Equipment

- Carbon Fiber Equipment

- Graphite Equipment

- Smart/Sensor-Integrated Equipment

By Distribution Channel

- Sporting Goods Retailers

- Specialty Pickleball Stores

- Online Marketplaces

- Brand-Owned E-Commerce Platforms

- Institutional/Club Direct Sales

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 63% of global pickleball equipment revenues in 2025. The United States alone contributes nearly 54% of global demand and continues to serve as the industry's growth engine. The region’s dominance is driven by the highest participation rates globally, extensive court infrastructure, strong presence of professional leagues and tournaments, and high consumer spending on sporting goods. Continuous investments in community recreation facilities, public pickleball courts, and private club developments have created a robust ecosystem that supports recurring equipment purchases. Furthermore, widespread media coverage, celebrity endorsements, and increasing youth participation are driving demand beyond the sport’s traditional senior demographic. Canada is benefiting from expanding community sports programs and growing adoption across urban centers, while Mexico is emerging as a developing market supported by rising recreational sports participation and cross-border influence from the United States.

Europe

Europe accounted for approximately 16% of global market revenues in 2025 and is experiencing strong growth driven by increasing awareness of the sport and the region’s established racket sports culture. The United Kingdom, Germany, Spain, France, Italy, and the Netherlands are leading adoption across the continent. Growth is being supported by expanding pickleball associations, club development initiatives, and government investments in recreational sports infrastructure. Spain’s long-standing popularity of tennis and padel provides a favorable environment for pickleball adoption, while Germany and the United Kingdom benefit from strong club-based participation models and high discretionary spending on sporting activities. The growing focus on active aging programs, community wellness initiatives, and low-impact recreational sports is also accelerating participation among older demographics, creating sustained equipment demand across Europe.

Asia-Pacific

Asia-Pacific accounted for approximately 14% of global revenues in 2025 and is projected to be the fastest-growing regional market throughout the forecast period. Growth is being driven by rising disposable incomes, increasing sports participation rates, expanding middle-class populations, and growing investments in sports infrastructure. Australia currently leads regional demand due to its mature recreational sports culture and well-established pickleball community. Meanwhile, India and China are emerging as the most attractive long-term growth markets owing to their large population bases and rapidly expanding sports ecosystems. Educational institutions, residential communities, and sports clubs are increasingly incorporating pickleball facilities, supporting equipment sales across multiple consumer segments. In India, growing awareness campaigns, national tournaments, and private investments in sports academies are expected to drive participation growth at one of the highest rates globally. Japan and South Korea are also witnessing increased adoption among senior populations seeking accessible and low-impact recreational activities.

Latin America

Latin America accounted for approximately 4% of global market revenues in 2025, with Brazil, Mexico, Argentina, and Chile leading regional demand. Market growth is being supported by rising middle-class participation in organized sports, increasing awareness through social media and international tournaments, and gradual improvements in sports infrastructure. Brazil remains the largest market due to its strong sporting culture and expanding recreational sports ecosystem. Mexico benefits from its geographic proximity to the United States, where exposure to pickleball trends continues to increase awareness and participation. As private sports clubs and community recreation centers introduce dedicated pickleball facilities, equipment demand is expected to strengthen steadily across the region.

Middle East & Africa

The Middle East & Africa region represented approximately 3% of global demand in 2025 but is emerging as a promising growth market. The United Arab Emirates and Saudi Arabia are leading regional expansion through significant investments in sports infrastructure, wellness initiatives, and premium recreational facilities. Government programs aimed at increasing physical activity and diversifying sports participation are creating favorable conditions for pickleball adoption. The growing expatriate population, particularly in the Gulf Cooperation Council countries, is further supporting demand as many players introduce the sport from North America and Europe. South Africa remains the largest African market, benefiting from established sporting infrastructure, rising awareness among younger demographics, and increasing participation in recreational racket sports. The expansion of sports tourism and luxury residential developments incorporating pickleball courts is expected to further accelerate regional equipment demand over the coming years.

Key Players in the Pickleball Equipment Market

- Selkirk Sport

- Franklin Sports

- Wilson Sporting Goods

- HEAD Pickleball

- JOOLA

- Paddletek

- Engage Pickleball

- ONIX Sports

- ProLite Sports

- Gamma Sports

- Prince Sports

- Vulcan Sporting Goods

- Gearbox Sports

- Diadem Sports

- ProKennex