Phytosterols Market Size

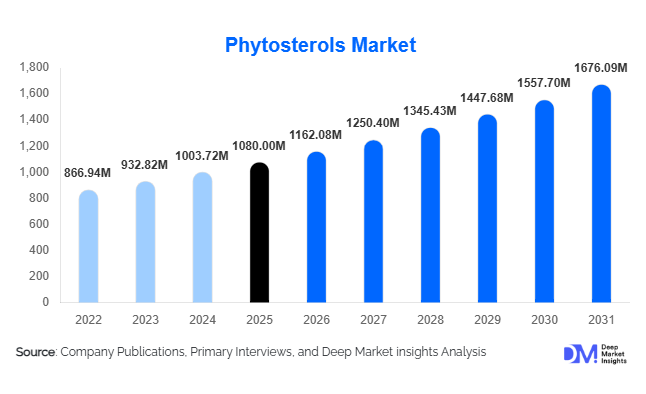

According to Deep Market Insights, the global phytosterols market size was valued at USD 1,080 million in 2025 and is projected to grow from USD 1,162.08 million in 2026 to reach USD 1,676.09 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The phytosterols market growth is primarily driven by increasing consumer awareness of cholesterol management, expanding demand for functional foods and nutraceuticals, and growing pharmaceutical utilization of plant sterol derivatives in cholesterol-lowering and steroid synthesis applications.

Key Market Insights

- Functional foods account for the largest revenue share, driven by fortified dairy, spreads, and cereals positioned for heart-health benefits.

- Beta-sitosterol dominates product demand, owing to strong clinical validation for LDL cholesterol reduction and broad pharmaceutical applications.

- North America leads the global market, supported by high nutraceutical consumption and regulatory-approved health claims.

- Asia-Pacific is the fastest-growing region, fueled by rising cardiovascular disease prevalence and expanding middle-class spending.

- Vegetable oil-derived phytosterols represent the majority supply source, benefiting from established oilseed processing infrastructure.

- B2B ingredient supply remains the dominant distribution channel, supported by long-term contracts with food and supplement manufacturers.

What are the latest trends in the phytosterols market?

Expansion of Plant-Based Functional Food Fortification

The rapid growth of plant-based diets is accelerating phytosterol incorporation into dairy alternatives, vegan spreads, protein bars, and fortified beverages. Food manufacturers are reformulating products to align with clean-label and cholesterol-lowering claims, strengthening phytosterols’ role as a scientifically validated bioactive ingredient. Microencapsulation technologies are improving solubility in beverages and expanding usage across ready-to-drink formats. This trend is particularly prominent in North America and Europe, where regulatory support for heart-health claims enhances retail penetration.

Pharmaceutical-Grade Purification and API Applications

High-purity phytosterols are increasingly used as intermediates in steroid drug synthesis and cholesterol-lowering formulations. Pharmaceutical-grade beta-sitosterol and stigmasterol production is expanding, supported by investments in advanced extraction and purification systems. Manufacturers are focusing on pharmacopeia-compliant production to capture higher-margin applications. Growing research into anti-inflammatory and immune-modulating properties may further broaden therapeutic uses.

What are the key drivers in the phytosterols market?

Rising Prevalence of Cardiovascular Diseases

Cardiovascular diseases remain a leading cause of global mortality, increasing demand for preventive nutrition solutions. Clinical studies demonstrating LDL cholesterol reduction of 7–10% with daily phytosterol intake have strengthened consumer and physician acceptance. This evidence-based positioning has driven product launches across supplements and fortified foods.

Growth of the Global Nutraceutical Industry

The global nutraceutical industry, valued at over USD 450 billion, continues to expand at 8–9% annually. Phytosterols are increasingly incorporated into capsules, tablets, and softgels targeting cholesterol management and prostate health. E-commerce penetration and direct-to-consumer supplement brands are further accelerating adoption.

What are the restraints for the global market?

Raw Material Price Volatility

Phytosterols are primarily extracted from soybean, rapeseed, and tall oil derivatives. Fluctuations in oilseed prices directly impact production costs, compressing margins and affecting pricing stability.

Regulatory Variability Across Regions

Health claim approvals differ significantly across regions, limiting uniform marketing strategies. Compliance requirements and labeling standards can delay product launches in emerging markets.

What are the key opportunities in the phytosterols industry?

Emerging Market Preventive Healthcare Programs

Countries such as China, India, and Brazil are promoting preventive healthcare to reduce long-term cardiovascular treatment costs. This creates opportunities for phytosterol-fortified staple foods and affordable supplement formulations tailored to middle-income consumers.

Microencapsulation and Beverage Integration

Technological innovation enabling the stable dispersion of phytosterols in beverages and dairy alternatives opens new application categories. Companies investing in advanced emulsification and encapsulation technologies can secure premium positioning in functional beverage segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1080 Million |

| Market Size in 2026 | USD 1162.08 Million |

| Market Size in 2031 | USD 1676.09 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Beta-sitosterol accounts for approximately 42% of the 2025 market share, making it the leading product segment in the global phytosterols market. Its dominance is primarily driven by extensive clinical validation demonstrating LDL cholesterol reduction benefits, which has strengthened its inclusion in heart-health supplements and fortified foods. Beta-sitosterol is also widely used in pharmaceutical synthesis as a precursor for steroid-based APIs, further supporting stable bulk demand from drug manufacturers. The ingredient’s strong regulatory acceptance in North America and Europe, combined with high consumer awareness of cholesterol management, reinforces its leadership position. Blended phytosterols follow as a cost-effective alternative for large-scale food fortification programs, particularly in spreads and dairy applications. Meanwhile, phytostanols, though representing a smaller share, are gaining traction in premium cardiovascular formulations due to their enhanced cholesterol absorption inhibition properties, especially in European markets where clinical nutrition adoption is strong.

Form Insights

Powdered phytosterols represent nearly 55% of the global market, driven by their versatility, longer shelf life, and ease of incorporation into capsules, tablets, cereals, and powdered beverage mixes. Powder form is preferred in B2B supply contracts due to simplified transportation, storage stability, and compatibility with automated blending systems. Granules and oil suspensions are primarily utilized in margarine, dairy products, and spreads, where fat-soluble dispersion is required. The fastest-growing form segment is microencapsulated phytosterols, supported by advancements in encapsulation technology that enhance solubility and bioavailability in ready-to-drink beverages and functional dairy alternatives. This innovation is expanding phytosterols’ reach into liquid applications, which historically faced formulation limitations.

Source Insights

Vegetable oil-derived phytosterols hold approximately 68% market share, supported by the abundant availability of soybean, rapeseed (canola), sunflower, and corn oil processing infrastructure across the United States, China, Brazil, and Europe. Large-scale oilseed crushing facilities enable cost-efficient sterol extraction as a by-product, ensuring supply consistency and competitive pricing. Tall oil-derived sterols form a significant secondary source, particularly in North America and Scandinavia, where pulp and paper industries provide feedstock. The growth of vegetable oil refining capacity in Asia-Pacific continues to strengthen raw material supply security and reduce dependence on imports, further consolidating this segment’s dominance.

Application Insights

Functional foods account for around 38% of total market revenue, making them the leading application segment. The segment’s growth is driven by rising consumer preference for preventive healthcare through everyday dietary intake. Regulatory-backed heart-health claims in key markets such as the U.S. and EU have enabled strong penetration of phytosterol-enriched dairy products, spreads, cereals, and snack bars. Dietary supplements follow closely and represent the fastest-growing segment, expanding at a CAGR of nearly 8–9%, supported by direct-to-consumer brands and e-commerce distribution. Pharmaceutical applications provide a stable baseline demand due to phytosterols’ role in steroid intermediate synthesis and cholesterol-lowering formulations. Cosmetics and animal nutrition are emerging niches, with phytosterols being incorporated into anti-aging formulations and premium pet nutrition products.

Distribution Channel Insights

B2B ingredient supply dominates with roughly 72% market share, reflecting long-term procurement contracts between phytosterol manufacturers and food, nutraceutical, and pharmaceutical companies. Large-volume industrial buyers prioritize stable pricing, quality certifications, and pharmacopeia compliance, which favors vertically integrated producers. Retail and e-commerce channels primarily serve finished supplement brands rather than raw sterol suppliers. However, the expansion of direct-to-consumer nutraceutical startups is indirectly increasing bulk phytosterol demand at the ingredient level.

End-Use Industry Insights

The global packaged functional food industry, valued at over USD 300 billion, remains the largest end-use sector for phytosterols, driven by consistent consumer demand for heart-health positioning. The nutraceutical industry, exceeding USD 450 billion globally, is the fastest-growing end-use segment, benefiting from preventive healthcare awareness and rising online supplement sales. Pharmaceutical demand remains steady due to phytosterols’ importance in steroid drug manufacturing, particularly in hormone and anti-inflammatory drug synthesis. Export-driven demand is strong in North America and Europe, where large-scale sterol producers supply ingredient volumes to Asia-Pacific supplement manufacturers. China has emerged as a significant importer of high-purity phytosterols for domestic nutraceutical production, reinforcing cross-border trade flows.

Explore more data points, trends and opportunities Download Free Sample Report

Phytosterols Market Segmentations

By Product Type

- Beta-Sitosterol

- Campesterol

- Stigmasterol

- Blended Phytosterols

- Phytostanols

By Form

- Powder

- Granules

- Oil/Suspension

- Microencapsulated & Emulsified Forms

By Source

- Vegetable Oils

- Tall Oil

- Nuts & Seed Extracts

By Application

- Functional Foods

- Dietary Supplements

- Pharmaceuticals

- Cosmetics & Personal Care

- Animal Nutrition

By Distribution Channel

- B2B Ingredient Supply

- Contract Manufacturing

- Retail & E-commerce

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, led by the United States. Regional growth is driven by high dietary supplement penetration, strong cardiovascular disease awareness, and regulatory approval of phytosterol health claims by authorities such as the FDA. The U.S. benefits from a mature nutraceutical ecosystem and large-scale soybean oil refining capacity, ensuring raw material availability. Canada contributes to steady growth through functional dairy and cereal fortification programs. Additionally, advanced pharmaceutical manufacturing infrastructure supports demand for high-purity sterol intermediates.

Europe

Europe accounts for nearly 29% of the global market, with Germany, France, the UK, and the Netherlands leading demand. Growth is primarily supported by EFSA-approved health claims, which allow strong marketing of cholesterol-lowering food products. European consumers exhibit high adoption of functional spreads and dairy products enriched with plant sterols. Sustainability trends and clean-label preferences further strengthen demand for plant-derived bioactives. Northern European countries also benefit from tall oil-based sterol extraction, enhancing regional production capacity.

Asia-Pacific

Asia-Pacific represents around 27% of the market and is the fastest-growing region at approximately 9% CAGR. China and India are major growth engines due to expanding middle-class populations, rising cardiovascular disease prevalence, and increasing preventive healthcare spending. Government initiatives supporting domestic nutraceutical manufacturing and oilseed processing capacity are reducing import dependency. Japan remains a mature market with strong demand for functional foods under its FOSHU regulatory framework. Growing e-commerce penetration in Southeast Asia is further accelerating supplement sales.

Latin America

Latin America holds about 6% market share, with Brazil and Mexico driving regional growth. Expansion of soybean cultivation and oil refining capacity in Brazil supports domestic sterol extraction. Rising urbanization, increasing processed food consumption, and expanding supplement awareness are contributing to gradual demand growth. However, regulatory harmonization remains a challenge across certain countries.

Middle East & Africa

This region accounts for approximately 4% of global demand. The UAE and Saudi Arabia show rising supplement consumption driven by lifestyle-related health awareness and increasing incidence of obesity and cardiovascular disorders. Growing retail penetration of imported functional foods and premium nutraceutical brands is supporting demand. South Africa represents a developing market within the region, benefiting from expanding food processing and health-conscious urban consumers.

Key Players in the Phytosterols Market

- BASF SE

- Arboris LLC

- Cargill Incorporated

- ADM

- DuPont de Nemours Inc.

- Wilmar International

- Gustav Parmentier GmbH

- Raisio plc

- Fenchem Biotek Ltd.

- Enzymotech Ltd.

- Matrix Fine Sciences

- Advanced Organic Materials SA

- Unilever

- Lipofoods

- Pharmachem Laboratories Inc.