Pharmaceutical Packaging Testing Market Size

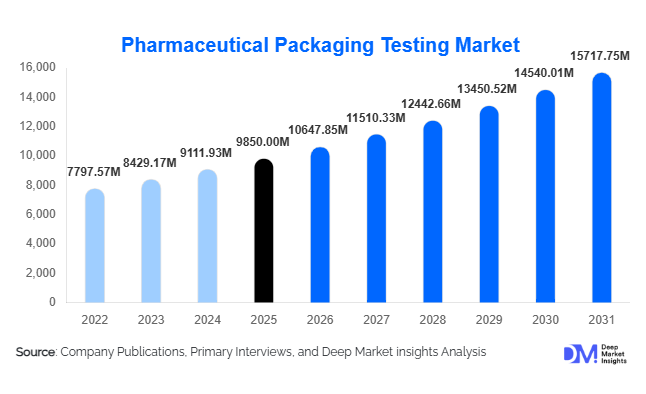

According to Deep Market Insights, the global pharmaceutical packaging testing market size was valued at USD 9,850 million in 2025 and is projected to grow from USD 10,647.85 million in 2026 to reach USD 15,717.75 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). Market growth is primarily driven by increasingly stringent regulatory requirements, the rapid expansion of biologics and injectable drug production, and the growing outsourcing of analytical and container closure integrity (CCI) testing services to specialized laboratories.

The market plays a vital role in ensuring drug stability, sterility, and compliance with global regulatory standards set by authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). With pharmaceutical innovation shifting toward complex biologics, mRNA vaccines, and combination drug-device products, packaging validation has become more sophisticated, requiring advanced extractables & leachables (E&L) analysis, deterministic CCI testing, and long-term stability studies. Emerging pharmaceutical manufacturing hubs across Asia-Pacific are further accelerating demand for both in-house testing equipment and outsourced laboratory services, positioning the market for steady long-term expansion.

Key Market Insights

- Outsourced testing services account for approximately 55% of the 2025 market share, as pharmaceutical companies adopt asset-light operational models.

- Physical testing leads by testing type, with nearly 32% market share, driven by mandatory compression, torque, and seal integrity validation.

- Plastic packaging materials dominate with 38% share, supported by increasing adoption of polymer-based vials, bottles, and prefilled syringes.

- North America holds 34% of the global market share, supported by strong regulatory enforcement and biologics manufacturing capacity.

- Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR due to export-driven pharmaceutical production in India and China.

- Top five companies collectively hold around 42% market share, reflecting moderate consolidation with strong global laboratory networks.

What are the latest trends in the pharmaceutical packaging testing market?

Shift Toward Deterministic Container Closure Integrity (CCI) Testing

The market is witnessing a strong transition from probabilistic methods such as dye ingress testing to deterministic technologies, including vacuum decay, high-voltage leak detection, and laser-based headspace analysis. Regulatory agencies increasingly prefer deterministic CCI methods due to higher sensitivity, repeatability, and quantitative validation. This shift is particularly significant in biologics and injectable drug packaging formats such as vials, prefilled syringes, and cartridges. Manufacturers are upgrading capital equipment to meet evolving compliance expectations, driving demand for high-precision instrumentation and automated inspection systems.

Rising Extractables & Leachables (E&L) Testing Demand

As drug formulations become more complex, especially biologics and cell & gene therapies, compatibility between packaging materials and drug substances has become critical. E&L studies are increasingly mandated during regulatory submissions. Advanced chromatographic and mass spectrometry-based analytical platforms are being deployed in specialized laboratories, boosting revenue for high-margin chemical testing services. The trend is particularly pronounced in polymer-based packaging formats where migration risks are closely monitored.

What are the key drivers in the pharmaceutical packaging testing market?

Stringent Regulatory Compliance

Regulatory frameworks worldwide require comprehensive validation of packaging materials to prevent contamination, degradation, and sterility breaches. Increased product recalls related to packaging failures have intensified compliance scrutiny. Regulatory harmonization under ICH guidelines has further standardized testing protocols, compelling manufacturers to conduct detailed validation before commercialization.

Growth of Biologics and Injectable Therapies

The global surge in monoclonal antibodies, biosimilars, and vaccines has significantly increased demand for sterile packaging validation. Vials and prefilled syringes require robust CCI and stability testing, driving consistent growth in microbiological and environmental testing segments. Biopharmaceutical expansion is particularly strong in North America and Asia-Pacific, supporting sustained testing demand.

What are the restraints for the global market?

High Capital Investment Requirements

Advanced analytical systems such as LC-MS/MS, gas chromatography, and deterministic CCI equipment require substantial capital investment. Smaller pharmaceutical firms often face financial barriers in adopting in-house testing systems, limiting growth in equipment sales.

Regional Regulatory Variations

Despite international harmonization efforts, region-specific documentation and testing standards increase compliance complexity. Pharmaceutical exporters must often duplicate validation studies to satisfy country-level regulatory nuances, increasing operational costs and slowing time-to-market.

What are the key opportunities in the pharmaceutical packaging testing industry?

Expansion in Emerging Pharmaceutical Manufacturing Hubs

Countries such as India, China, Brazil, and Saudi Arabia are investing heavily in pharmaceutical manufacturing infrastructure. Government initiatives like “Make in India” and “Made in China 2026” are strengthening domestic drug production, increasing demand for compliant packaging validation services.

Digitalization and Automation of Laboratories

Integration of AI-driven defect detection, cloud-based documentation systems, and automated stability chambers is enhancing efficiency and regulatory audit readiness. Laboratories offering integrated digital compliance solutions are gaining competitive advantages, especially among multinational pharmaceutical companies.

Testing Type Insights

Physical testing dominates the pharmaceutical packaging testing market with approximately 32% share in 2025, maintaining its leadership due to universal applicability across all primary and secondary packaging formats. Compression strength, burst resistance, torque testing, seal integrity, and drop testing are mandatory validation procedures for bottles, blister packs, vials, IV bags, and flexible pouches. The leading driver for this segment is regulatory standardization of mechanical integrity testing under global pharmacopeia guidelines, which requires manufacturers to validate packaging durability before commercialization. As pharmaceutical companies expand production volumes, particularly in generics and over-the-counter drugs, routine batch-wise mechanical testing continues to generate recurring revenue streams. In addition, automation of torque and seal strength testing systems is improving throughput in high-volume production facilities, reinforcing segment dominance.

Chemical testing, particularly extractables and leachables (E&L) studies, represents one of the fastest-growing sub-segments, driven by the rapid expansion of biologics, biosimilars, and sensitive injectable formulations. Increasing regulatory scrutiny around material-drug interactions in polymer-based packaging is accelerating advanced chromatographic and spectrometry-based analysis. Microbiological testing remains critical for sterile injectables and parenteral drugs, especially for container closure integrity validation. Environmental and stability testing is expanding in parallel, supported by global distribution networks requiring long-term shelf-life validation across multiple climatic zones.

Packaging Material Insights

Plastic packaging materials account for approximately 38% of total market revenue in 2025, making them the leading material segment. The primary driver behind plastic’s dominance is the growing adoption of lightweight, cost-efficient, and chemically stable polymer packaging such as HDPE bottles, polypropylene closures, COC/COP prefilled syringes, and multilayer barrier films. The shift toward self-administration devices, including autoinjectors and prefilled syringes, has further strengthened demand for polymer-based materials requiring rigorous compatibility and CCI testing.

Glass packaging remains highly significant, particularly Type I borosilicate glass vials used in injectable biologics and vaccines. However, concerns related to glass delamination and breakage risks are driving increased testing intensity rather than volume expansion. Metal packaging and flexible laminates continue to serve oral solid dosage forms, particularly blister packaging, where barrier property validation and seal strength testing remain essential. The transition toward sustainable and recyclable materials is also influencing testing protocols, creating additional validation requirements for new-generation packaging substrates.

Service Type Insights

Outsourced testing services lead the market with approximately 55% share in 2025, reflecting pharmaceutical manufacturers’ strategic shift toward asset-light operating models. The key driver for this segment is cost optimization and access to advanced analytical expertise without heavy capital expenditure. Deterministic CCI systems, LC-MS/MS platforms, and stability chambers require high upfront investment and skilled personnel, making third-party laboratory partnerships economically attractive.

Contract testing laboratories offer scalability, regulatory documentation support, and faster turnaround times, especially beneficial for small and mid-sized pharmaceutical firms and emerging biotech companies. In-house testing equipment sales remain strong among large multinational corporations with dedicated quality control infrastructure and continuous production pipelines. However, even these companies increasingly outsource specialized E&L or microbiological validation studies to external experts for regulatory submissions in multiple geographies.

End-Use Industry Insights

Pharmaceutical manufacturers account for approximately 47% of total market demand in 2025, driven primarily by large-scale generics and branded drug production. The leading driver in this segment is the global expansion of oral solid dosage manufacturing and export-oriented compliance testing. High-volume production requires repetitive mechanical, chemical, and stability validation across product batches, sustaining consistent testing demand.

Biopharmaceutical companies represent the fastest-growing end-use segment, expanding at nearly 10% CAGR, supported by the increasing pipeline of injectable monoclonal antibodies, biosimilars, and advanced therapies. These products require highly sensitive container closure integrity and compatibility validation, increasing per-product testing intensity. Contract Development and Manufacturing Organizations (CDMOs) are also expanding rapidly due to pharmaceutical outsourcing trends, creating additional demand for integrated packaging validation services. Growth in combination drug-device products further enhances demand for multi-dimensional testing protocols.

| By Testing Type | By Packaging Material | By Service Type | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global pharmaceutical packaging testing market share in 2025, led predominantly by the United States. The primary growth driver in this region is stringent regulatory enforcement and high biologics manufacturing output. The presence of advanced R&D infrastructure, strong FDA compliance monitoring, and a large concentration of multinational pharmaceutical companies sustains consistent testing demand. Increasing investments in cell and gene therapy manufacturing facilities across the U.S. are further intensifying requirements for deterministic CCI and extractables testing. Canada contributes through vaccine production and specialty pharmaceutical exports.

Europe

Europe accounts for approximately 27% market share in 2025, with Germany, France, the United Kingdom, and Switzerland as key contributors. The region’s leading growth driver is strong generics exports combined with harmonized EMA regulatory frameworks, which mandate rigorous packaging validation for cross-border drug distribution. Germany remains a major generics exporter, increasing demand for stability and compliance testing. The U.K. and Switzerland contribute significantly through high-value biologics and specialty pharmaceutical manufacturing. Sustainability initiatives within the EU are also driving testing requirements for recyclable and alternative packaging materials.

Asia-Pacific

Asia-Pacific holds about 24% share of the global market and is the fastest-growing region at nearly 10% CAGR. The dominant regional growth driver is the rapid expansion of export-oriented pharmaceutical manufacturing. India is the fastest-growing country (around 11% CAGR), supported by large-scale generics exports to the U.S. and Europe, necessitating compliance with international testing standards. China continues expanding domestic biologics production capacity, increasing demand for advanced chemical and microbiological validation. Japan and South Korea contribute through high-quality pharmaceutical production and innovation-driven testing adoption.

Latin America

Latin America contributes nearly 8% of global demand, with Brazil and Mexico serving as primary pharmaceutical production hubs. The key driver in this region is growing domestic drug manufacturing and regional regulatory strengthening. Increasing government focus on reducing pharmaceutical imports is stimulating local production, which in turn requires standardized packaging validation to meet both domestic and export requirements. Infrastructure modernization in Brazil is gradually enhancing testing capacity.

Middle East & Africa

The Middle East & Africa region accounts for roughly 7% of the global market share. Growth is driven by government-backed pharmaceutical localization initiatives in countries such as Saudi Arabia and the United Arab Emirates, aimed at reducing import dependency. Investments in domestic drug production facilities are increasing the demand for packaging integrity and stability testing. South Africa plays a leading role in Sub-Saharan Africa through generics manufacturing and vaccine distribution. Over time, regulatory modernization across the region is expected to further formalize testing requirements, supporting steady market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Pharmaceutical Packaging Testing Market

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group

- Charles River Laboratories

- West Pharmaceutical Services

- Nelson Labs

- TÜV SÜD

- Element Materials Technology

- WuXi AppTec

- Pace Analytical

- SteriPack

- NamSA

- Microbac Laboratories

- Kymanox