Pet Cognitive Health Supplements Market Size

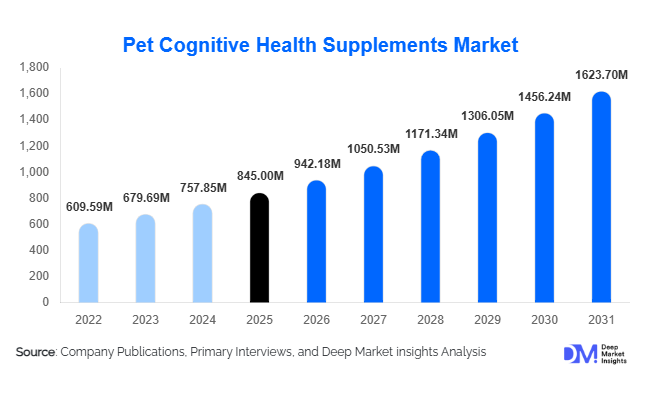

According to Deep Market Insights,the global pet cognitive health supplements market size was valued at USD 845 million in 2025 and is projected to grow from USD 942.18 million in 2026 to reach USD 1,623.70 million by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). Market growth is primarily driven by rising pet humanization, increasing life expectancy of companion animals, and growing awareness regarding cognitive dysfunction syndrome (CDS) in aging pets. As preventive veterinary care gains prominence, pet owners are increasingly investing in brain health supplements formulated with DHA, MCTs, antioxidants, amino acids, and botanical extracts to enhance memory, alertness, and behavioral stability in dogs and cats.

Key Market Insights

- Senior dogs represent the largest consumer group, accounting for nearly 46% of total 2025 demand, driven by higher diagnosis rates of cognitive decline.

- Combination cognitive formulations dominate product innovation, contributing approximately 32% of the global market share in 2025.

- Veterinary clinics remain the leading distribution channel, supported by strong professional endorsements and clinical screening practices.

- North America holds the largest regional share, accounting for nearly 38% of the global market in 2025.

- Asia-Pacific is the fastest-growing region, expanding at a CAGR above 14% due to rising premium pet care spending in China, Japan, and India.

- Direct-to-consumer and subscription-based models are improving recurring revenue and brand loyalty across developed markets.

What are the latest trends in the pet cognitive health supplements market?

Shift Toward Preventive Brain Health Supplementation

Pet cognitive supplements are increasingly being positioned as preventive wellness solutions rather than reactive treatments. Veterinary practitioners are recommending early supplementation for pets aged five years and above to delay cognitive decline. This shift is expanding the total addressable market by encouraging long-term daily usage. Brands are also investing in clinically backed ingredients such as DHA from algal oil and MCT formulations that support ketone-based brain energy metabolism. Preventive positioning has improved consumer perception, making cognitive supplements a routine part of senior pet nutrition.

Rise of Functional Chews and Palatable Formats

Chewable tablets and soft chews account for approximately 38% of total market revenue in 2025. Palatability plays a critical role in compliance, particularly for daily regimens. Manufacturers are incorporating natural flavors, grain-free bases, and functional treat formats that combine brain support with joint and immune benefits. The growing demand for multifunctional supplements reflects pet owners’ preference for simplified dosing and value-added formulations.

What are the key drivers in the pet cognitive health supplements market?

Growing Geriatric Pet Population

Improved veterinary care and premium nutrition have significantly increased pet life expectancy. In developed markets, over 40% of pet dogs are now categorized as senior. Cognitive dysfunction syndrome is prevalent in aging pets, directly driving demand for targeted supplementation. As awareness improves, early-stage diagnosis is becoming more common, increasing long-term supplement adoption rates.

Premiumization and Pet Humanization

Pet owners increasingly treat animals as family members, leading to higher spending on preventive healthcare. Global pet healthcare expenditure is rising consistently above inflation rates, with cognitive health emerging as a niche but rapidly expanding category. Owners are willing to pay premium prices for scientifically validated, natural, and veterinarian-recommended products, contributing to strong average profit margins ranging between 18–28%.

What are the restraints for the global market?

Regulatory Ambiguity Across Regions

Regulatory frameworks for pet nutraceuticals vary significantly across countries. Differences in labeling, health claims approval, and classification between supplements and veterinary drugs can create compliance complexity. This restricts rapid international expansion for smaller brands.

Price Sensitivity in Emerging Markets

Premium cognitive supplements often cost between USD 25–60 per monthly supply, limiting penetration in price-sensitive economies. Awareness gaps in developing regions further restrict mass adoption, particularly where basic pet nutrition still dominates spending.

What are the key opportunities in the pet cognitive health supplements industry?

Expansion in Asia-Pacific Urban Markets

Urban centers in China, India, and Southeast Asia are witnessing rapid growth in pet ownership. Rising disposable income and increasing exposure to Western pet care trends create strong opportunities for premium supplement brands. Localized manufacturing and smaller pack sizes can support mid-income adoption. Asia-Pacific is expected to become the second-largest regional market by 2031.

Gut-Brain Axis Product Innovation

Emerging research linking microbiome health with neurological performance presents strong innovation potential. Combination supplements integrating probiotics with DHA and antioxidants are gaining traction. Brands investing in clinical validation and differentiated formulations are expected to capture higher-value consumer segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 845 Million |

| Market Size in 2026 | USD 942.18 Million |

| Market Size in 2031 | USD 1623.70 Million |

| CAGR | 11.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The product landscape is led by omega fatty acid supplements, which account for nearly 47% of total market revenue in 2025, positioning them as the dominant segment. Their leadership is primarily driven by strong clinical validation supporting anti-inflammatory benefits, enhanced skin hydration, and improved coat luster, making them a preferred choice among veterinarians and pet owners alike. Increasing prevalence of allergic dermatitis and chronic skin conditions further reinforces demand for omega-3 and omega-6 formulations. Vitamins and mineral-based supplements, particularly those containing biotin, zinc, and vitamin E, form a substantial secondary segment supported by their role in strengthening the skin barrier and promoting cellular repair. Rising awareness around micronutrient deficiencies in pets has amplified adoption of these formulations in preventive care routines. Herbal and plant-based extracts are gaining traction in premium product portfolios as consumers increasingly seek natural, clean-label, and hypoallergenic alternatives. Ingredients such as turmeric, chamomile, and flaxseed are being incorporated to appeal to health-conscious pet parents. Collagen and protein complexes are emerging as complementary solutions, particularly for aging pets experiencing coat thinning, dryness, and reduced skin elasticity, with demand supported by the broader humanization trend in pet nutrition.

Form Insights

Soft chews lead the market with approximately 42% share in 2025, driven primarily by superior palatability, convenience, and improved compliance among pets. The leading segment’s growth is supported by increasing preference for treat-format supplements that simplify administration without causing stress to animals. Tablets and capsules maintain relevance, especially within veterinary-recommended channels where dosage precision and therapeutic positioning are prioritized. Powders continue to gain adoption due to their flexibility in mixing with daily meals, making them suitable for multi-pet households and customized feeding routines. Liquid supplements and topical oils, while comparatively niche, are expanding steadily as pet owners seek faster absorption, targeted dermatological relief, and localized application for acute skin concerns. Innovation in flavor masking, texture enhancement, and easy-dispense packaging continues to influence form-based competition across the market.

Distribution Channel Insights

Online retail accounts for around 36% of total sales, making it the leading distribution channel. Its dominance is supported by the rapid expansion of e-commerce platforms, subscription-based replenishment models, competitive pricing strategies, and access to a broader assortment of domestic and international brands. The convenience of home delivery and increasing digital literacy among consumers further accelerate online penetration. Veterinary clinics and hospitals contribute nearly 30% of total revenue, benefiting from strong professional endorsement and consumer trust in medically guided product selection. Pet specialty stores remain essential for premium product positioning, offering personalized recommendations and curated assortments that appeal to informed buyers. Supermarkets and hypermarkets focus on mid-range and mass-market offerings, leveraging high foot traffic and impulse purchases to capture value-conscious consumers. The integration of omnichannel strategies is becoming increasingly important in enhancing brand visibility and consumer engagement.

End-Use Application Insights

Allergy and itch management leads application demand with approximately 38% share in 2025, driven by the rising incidence of allergic dermatitis, environmental sensitivities, and food-related intolerances among pets. The leading segment’s growth is reinforced by increasing veterinary diagnoses and heightened owner awareness regarding early symptom management. Coat shine and fur health applications represent a substantial share of preventive supplementation, supported by growing emphasis on aesthetics and overall pet appearance as part of the humanization trend. Skin barrier repair solutions targeting chronic dryness, flakiness, and sensitivity are witnessing steady expansion, particularly among senior pets and breeds predisposed to dermatological conditions. Shedding control continues to serve as an important seasonal driver, especially in temperate climates where coat transitions during spring and autumn stimulate short-term spikes in supplement demand.

Explore more data points, trends and opportunities Download Free Sample Report

Pet Cognitive Health Supplements Market Segmentations

By Product Type

- Omega-3 & DHA-Based Supplements

- MCT (Medium Chain Triglyceride) Formulations

- Antioxidant Blends

- Amino Acid & Neurotransmitter Support

- Herbal & Botanical Extracts

- Probiotic & Gut-Brain Axis Formulations

- Combination / Multi-Ingredient Cognitive Formulas

By Pet Type

- Dogs

- Cats

- Others

By Form

- Chewable Tablets & Soft Chews

- Capsules & Pills

- Powders

- Liquid Drops & Oils

- Functional Cognitive Treats

By Distribution Channel

- Veterinary Clinics & Hospitals

- Pet Specialty Stores

- Online Retail & E-commerce

- Supermarkets/Hypermarkets

- Direct-to-Consumer

By Ingredient Origin

- Synthetic Formulations

- Natural/Plant-Based

- Marine-Based

By End User

- Household Pet Owners

- Veterinary & Clinical Use

- Animal Shelters & Boarding Facilities

Regional Insights

North America

North America holds approximately 38% of the global market in 2025, with the United States accounting for nearly 82% of regional demand. Growth in this region is driven by high pet ownership rates, strong disposable income levels, and the continued premiumization of pet nutrition products. Well-established veterinary infrastructure and widespread professional endorsement significantly influence purchasing decisions. The region also benefits from advanced e-commerce ecosystems and subscription-based supplement models that encourage recurring revenue streams. Increasing demand for clean-label, non-GMO, and sustainably sourced ingredients further supports innovation and product differentiation across the North American market.

Europe

Europe represents around 27% of global revenue, led by Germany, the United Kingdom, and France. Regional growth is driven by strong regulatory frameworks that ensure product safety and formulation transparency, fostering consumer trust. A pronounced preference for eco-certified, organic, and sustainably sourced ingredients influences purchasing behavior, particularly in Western Europe. Rising awareness of preventive pet healthcare and increasing expenditure on companion animals contribute to steady demand expansion. The presence of established pet specialty retail networks and veterinary pharmacies further strengthens distribution efficiency and market penetration across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 11% CAGR. China and India serve as primary growth engines due to rapid urbanization, rising middle-class income, and increasing pet humanization trends. Growing awareness of preventive pet healthcare and expanding access to veterinary services are accelerating supplement adoption. In addition, the proliferation of online marketplaces and cross-border e-commerce platforms enhances product availability in emerging urban centers. Japan and Australia represent mature yet stable markets characterized by demand for premium, scientifically formulated, and veterinary-recommended products. The region’s expanding pet population and evolving lifestyle patterns continue to create substantial long-term growth opportunities.

Latin America

Latin America accounts for approximately 6% of global market share, with Brazil and Mexico leading regional demand. Growth is supported by increasing urban pet ownership, gradual expansion of veterinary infrastructure, and improving consumer awareness regarding skin and coat health management. Rising disposable incomes and greater penetration of organized retail channels are enhancing accessibility to both mid-range and premium supplement offerings. While price sensitivity remains a consideration, demand for functional and preventive pet health solutions continues to strengthen across major metropolitan areas.

Middle East & Africa

The Middle East & Africa region holds about 4% share of the global market, with the UAE and South Africa emerging as high-potential growth centers. Market expansion is driven by rising disposable incomes, increasing adoption of companion animals, and a growing inclination toward premium pet care products. Expansion of modern retail infrastructure and veterinary services in urban hubs is improving product accessibility. Additionally, the influence of expatriate populations and exposure to Western pet care trends are contributing to gradual but steady growth in supplement consumption across the region.

Key Players in the Pet Cognitive Health Supplements Market

- Nestlé Purina PetCare

- Mars Petcare

- Zoetis Inc.

- Virbac

- Elanco Animal Health

- Nutramax Laboratories

- Vetoquinol

- Ceva Santé Animale

- Swedencare AB

- Zesty Paws

- NaturVet

- NOW Foods

- GNC Holdings

- PetHonesty

- Ark Naturals