Pet Cardiovascular Supplements Market Size

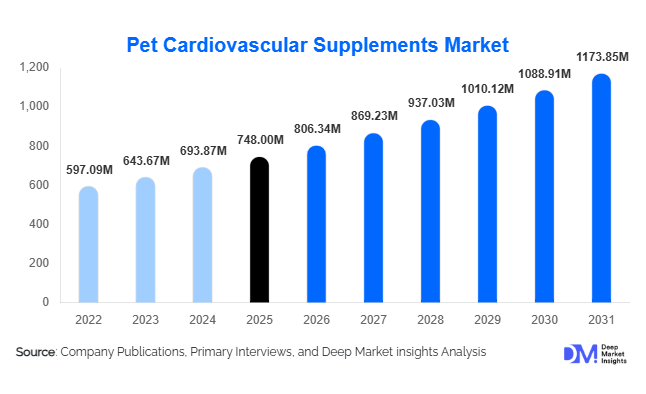

According to Deep Market Insights,the global pet cardiovascular supplements market size was valued at USD 748 million in 2025 and is projected to grow from USD 806.34 million in 2026 to reach USD 1,173.85 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The pet cardiovascular supplements market growth is primarily driven by the rising prevalence of heart diseases in companion animals, increasing pet humanization, and growing veterinary recommendations for adjunct cardiac support therapies. As pets live longer due to improved healthcare and nutrition, age-related cardiac disorders such as dilated cardiomyopathy and mitral valve disease are becoming more common, significantly expanding the addressable consumer base for targeted nutraceutical interventions.

Key Market Insights

- Condition-specific formulations are gaining traction, with omega-3, taurine, and CoQ10-based supplements leading product innovation.

- Veterinary clinics dominate distribution, accounting for over 40% of global revenue due to prescription-linked recommendations.

- Dogs represent the largest animal segment, contributing more than 70% of total market revenue.

- North America leads global demand, supported by high pet insurance penetration and premium spending patterns.

- Asia-Pacific is the fastest-growing region, driven by urbanization and rising companion animal adoption in China and India.

- E-commerce and subscription models are accelerating repeat purchases and improving consumer access to premium formulations.

What are the latest trends in the pet cardiovascular supplements market?

Shift Toward Preventive Cardiac Wellness

Pet owners are increasingly adopting preventive healthcare strategies, integrating cardiovascular supplements into routine wellness programs for aging and high-risk breeds. Rather than waiting for clinical diagnosis, consumers are proactively purchasing omega-3 and antioxidant blends to maintain heart health. Veterinary professionals are also recommending early supplementation for breeds predisposed to cardiomyopathy, strengthening demand within preventive care segments. This transition from reactive to proactive supplementation is expanding recurring revenue opportunities for manufacturers.

Clean-Label and Clinically Validated Formulations

Consumers are demanding transparency in ingredient sourcing, dosage validation, and clinical efficacy. Supplements featuring marine-sourced omega-3s, pharmaceutical-grade CoQ10, and standardized herbal extracts are outperforming generic multivitamin blends. Brands are investing in third-party testing, sustainable sourcing certifications, and published clinical trials to build credibility. The integration of bioavailable delivery systems, such as microencapsulation and enhanced absorption soft chews, is further differentiating premium products in competitive markets.

What are the key drivers in the pet cardiovascular supplements market?

Rising Prevalence of Cardiac Disorders in Companion Animals

Heart disease affects an estimated 10–15% of dogs during their lifetime, with incidence rates increasing significantly among pets over seven years of age. Improved veterinary diagnostics, including echocardiography and cardiac biomarker testing, are facilitating early detection and increasing supplement adoption as adjunct therapy. As global pet lifespans extend, demand for long-term cardiac support solutions is expected to rise steadily.

Premiumization and Pet Humanization

Pet owners increasingly perceive companion animals as family members, leading to higher healthcare expenditure per pet. Premium nutraceuticals with targeted cardiac benefits command strong price realization, with average annual price increases of 3–5%. High-income households in North America and Europe are particularly inclined toward clinically supported and veterinarian-endorsed products, supporting sustained market expansion.

What are the restraints for the global market?

Regulatory Variability and Quality Standardization

Pet supplements are regulated differently across regions, often classified under feed additive frameworks rather than pharmaceutical standards. This inconsistency may limit veterinary confidence and create barriers to international expansion. Companies must navigate labeling, dosage claims, and ingredient approval requirements that vary significantly between the U.S., EU, and Asia-Pacific markets.

Price Sensitivity in Emerging Economies

Premium cardiovascular supplements can be relatively expensive due to specialized ingredients and quality assurance processes. In price-sensitive regions, adoption may remain limited unless manufacturers introduce localized production or tiered pricing strategies. Currency fluctuations and raw material volatility can further impact affordability.

What are the key opportunities in the pet cardiovascular supplements industry?

Integration with Veterinary Preventive Care Programs

There is strong potential for collaboration between supplement manufacturers and veterinary networks to incorporate cardiac nutraceuticals into annual wellness plans. Subscription-based refill models and age-specific heart health kits can drive recurring revenue while improving compliance. Preventive care integration is expected to expand particularly in insured pet populations.

Expansion in Emerging Asia-Pacific Markets

China, India, and Southeast Asian nations are witnessing rapid growth in companion animal adoption and veterinary infrastructure development. Establishing early brand presence through partnerships with regional veterinary chains and online marketplaces can create long-term competitive advantages. Mid-tier product lines tailored to local purchasing power represent a significant untapped opportunity.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 748 Million |

| Market Size in 2026 | USD 806.34 Million |

| Market Size in 2031 | USD 1173.85 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Omega-3 fatty acid supplements dominate the global pet cardiovascular supplements market, accounting for approximately 26% of total revenue in 2025. Their leading position is primarily driven by clinically recognized cardioprotective benefits, including triglyceride reduction, anti-inflammatory action, and improved endothelial function. The growing prevalence of obesity-related cardiac complications in companion animals, combined with increasing veterinarian recommendations for long-term heart health management, further strengthens demand. In addition to cardiovascular benefits, omega-3 supplements provide joint, cognitive, and dermatological support, making them a multifunctional solution that enhances product value perception among pet owners. Taurine and CoQ10 supplements follow closely, particularly in therapeutic settings where they are frequently prescribed for dilated cardiomyopathy and other cardiac deficiencies. Combination formulations integrating antioxidants, L-carnitine, and herbal extracts are gaining traction as manufacturers focus on synergistic blends designed to improve clinical outcomes, extend product differentiation, and support comprehensive heart health protocols.

Formulation Format Insights

Chewable tablets and soft chews represent the largest formulation segment, contributing nearly 38% of total market revenue in 2025. The dominance of this format is primarily driven by superior palatability, ease of administration, and improved compliance rates among dogs, which account for the majority of supplement consumption. Treat-style supplementation aligns with pet humanization trends, where owners prefer convenient, stress-free delivery formats that resemble functional treats rather than medicinal products. Capsules and powders continue to maintain relevance in veterinary-prescribed regimens where precise dosage and ingredient concentration are prioritized. Liquid formulations are particularly favored for small breeds and cats due to flexible dosing capabilities and ease of mixing with food, supporting steady demand across feline-focused product lines.

Animal Type Insights

Dogs account for approximately 72% of global market revenue in 2025, making them the leading animal segment. This dominance is driven by a higher incidence of cardiovascular disorders in certain dog breeds, increased routine health screenings, and significantly higher per-pet healthcare expenditure compared to other companion animals. The strong emotional attachment between dog owners and pets further accelerates adoption of preventive and therapeutic supplements. Cats represent a smaller but steadily growing segment, particularly in developed markets where awareness of feline hypertrophic cardiomyopathy and taurine deficiency-related conditions is increasing. Growth in this segment is supported by expanding feline insurance coverage and greater veterinary emphasis on early diagnosis. Other companion animals, while niche, are gradually contributing incremental demand as veterinary care standards improve and exotic pet ownership rises in urban markets.

Distribution Channel Insights

Veterinary clinics and hospitals dominate the distribution landscape, holding approximately 41% of the global market share in 2025. This leadership is primarily driven by professional endorsement, which significantly influences purchasing decisions, especially for therapeutic and adjunct cardiac treatments. Veterinarian trust and diagnostic-based recommendations enhance product credibility and justify premium pricing. Retail pet specialty stores continue to play a supporting role by offering branded and preventive supplement options. Online channels represent the fastest-growing distribution segment, fueled by subscription-based refill models, competitive pricing strategies, wider product assortments, and increasing digital purchasing behavior among pet owners. The expansion of direct-to-consumer nutraceutical brands through e-commerce platforms is further accelerating channel diversification.

End-Use Insights

Therapeutic and adjunct treatment applications account for nearly 58% of total market share in 2025, reflecting strong adoption among pets diagnosed with cardiovascular conditions. Growth in this segment is driven by rising veterinary diagnostic capabilities, improved early detection rates, and increasing life expectancy among companion animals, which elevates the prevalence of age-related cardiac disorders. Preventive cardiac health management is emerging as the fastest-growing end-use segment, supported by wellness programs, breed-specific risk awareness campaigns, and routine screening initiatives. As pet owners increasingly shift toward proactive healthcare strategies, demand for long-term maintenance supplements continues to strengthen. Additionally, the expanding global veterinary services industry, valued at over USD 110 billion in 2026, indirectly supports cardiovascular supplement demand by increasing clinical touchpoints and treatment recommendations.

Explore more data points, trends and opportunities Download Free Sample Report

Pet Cardiovascular Supplements Market Segmentations

By Product Type

- Omega-3 Fatty Acid Supplements

- Taurine-Based Supplements

- Coenzyme Q10 (CoQ10) Supplements

- L-Carnitine Supplements

- Antioxidant Blends

- Herbal & Botanical Extracts

- Combination/Multifunctional Cardiac Formulations

By Formulation Format

- Chewable Tablets & Soft Chews

- Capsules & Tablets

- Powders & Granules

- Liquid Formulations & Tinctures

- Functional Treats/Edible Supplements

By Animal Type

- Dogs

- Cats

- Other Companion Animals

By Distribution Channel

- Veterinary Clinics & Hospitals

- Pet Specialty Retail Stores

- Online & E-commerce Platforms

- Pharmacies & Mass Merchandisers

By Application

- Preventive Cardiac Health Management

- Therapeutic & Adjunct Treatment for Diagnosed Conditions

Regional Insights

North America

North America leads the global pet cardiovascular supplements market, accounting for approximately 38% of total revenue in 2025. The United States alone contributes nearly 30% of global demand, supported by advanced veterinary infrastructure, high pet insurance penetration, and strong consumer willingness to invest in premium pet healthcare products. The region benefits from widespread awareness of breed-specific cardiac risks, strong nutraceutical market maturity, and well-established regulatory frameworks that enhance product credibility. The rapid expansion of e-commerce and subscription-based pet supplement services further accelerates market growth. Canada demonstrates steady expansion driven by rising preventive healthcare awareness, increasing urban pet ownership, and growth in specialty veterinary services.

Europe

Europe captures approximately 29% of the global market in 2025, led by Germany, the United Kingdom, and France. Germany accounts for nearly 7% of global revenue, supported by strong consumer acceptance of nutraceuticals and a well-developed pet care ecosystem. The United Kingdom benefits from premium pet spending patterns, increasing adoption of preventive healthcare, and a mature veterinary services sector. Across the region, stringent quality standards and regulatory oversight enhance consumer trust in supplement efficacy. Aging pet populations, expanding pet insurance coverage, and increasing focus on preventive wellness programs collectively drive steady regional growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 9.5%. Rapid urbanization, rising disposable incomes, and shifting cultural attitudes toward companion animal ownership are key growth drivers. China accounts for approximately 8% of global demand in 2025, fueled by premiumization trends and expanding online retail infrastructure. India is emerging rapidly due to growing middle-class pet adoption, increased veterinary clinic penetration, and improving awareness of pet preventive healthcare. Japan and Australia remain stable and mature markets characterized by high-quality standards, aging pet populations, and strong demand for premium and clinically formulated supplements.

Latin America

Brazil and Mexico lead demand in Latin America, supported by expanding middle-class demographics and increasing pet humanization trends. Although the regional share remains below 8% in 2025, steady growth is anticipated as veterinary infrastructure improves and awareness of chronic pet health conditions rises. Economic stabilization in key markets, coupled with expanding specialty pet retail chains and online platforms, is expected to enhance supplement accessibility and drive incremental adoption across urban centers.

Middle East & Africa

The Middle East & Africa region represents a developing but promising market. The United Arab Emirates and South Africa serve as primary growth hubs, supported by premium pet retail expansion, increasing expatriate pet ownership, and rising urban adoption rates. Growing awareness of preventive healthcare and expanding veterinary clinic networks contribute to gradual market penetration. While overall market share remains modest compared to developed regions, increasing disposable income levels and the introduction of international supplement brands are expected to support long-term growth potential.

Key Players in the Pet Cardiovascular Supplements Market

- Nutramax Laboratories

- Zoetis Inc.

- NOW Foods

- Nordic Naturals

- Ark Naturals

- Virbac

- Vetoquinol

- PetHonesty

- Zesty Paws

- NaturVet

- Swedencare AB

- Animal Essentials

- VetriScience Laboratories

- Beaphar

- Thorne Vet