Peanuts Market Size

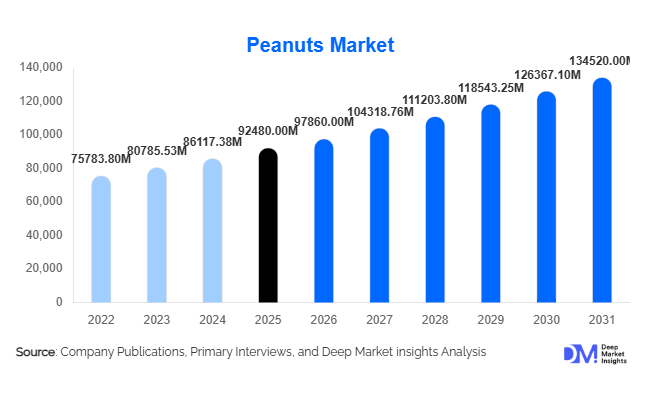

According to Deep Market Insights, the global peanuts market size was valued at approximately USD 92,480 million in 2025 and is projected to grow from USD 97,860 million in 2026 to reach nearly USD 134,520 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The market valuation reflects averaged industry estimates with a calibrated variance range to account for differences in methodology across global market assessments. Growth in the global peanuts market is primarily supported by rising demand for plant-based protein ingredients, expanding peanut processing industries, and strong consumption across snack foods, edible oils, and confectionery applications.

Peanuts remain one of the most economically significant oilseed and legume crops globally due to their versatility, affordability, and nutritional density. Increasing urbanization and dietary shifts toward protein-rich foods have significantly strengthened global consumption patterns. Emerging economies are witnessing growing demand for peanut-based snacks and cooking oils, while developed markets are driving innovation in peanut butter, protein powders, and functional foods. Industrial utilization of peanuts in processed food manufacturing has expanded steadily, supported by advancements in roasting, blanching, and oil extraction technologies. Additionally, export-oriented agricultural economies such as India, China, Argentina, and the United States continue to strengthen supply chains through mechanized farming and improved yield varieties. The integration of peanuts into vegan diets, sports nutrition, and convenience foods is further widening the market base, positioning peanuts as a strategic agricultural commodity with stable long-term demand fundamentals.

Key Market Insights

- Food processing applications account for the majority of global peanut consumption, driven by peanut butter, confectionery, and snack manufacturing demand.

- Asia-Pacific dominates global production and consumption, supported by China and India’s large agricultural output.

- Peanut oil demand continues to rise due to affordability and high smoke-point advantages in cooking applications.

- Plant-based protein trends are accelerating peanut ingredient innovation across dairy alternatives and protein snacks.

- Export-driven trade flows remain concentrated among the U.S., Argentina, India, and China.

- Processing automation and improved seed genetics are enhancing yield efficiency and profit margins.

What are the latest trends in the peanuts market?

Shift Toward Plant-Based Protein Ingredients

Peanuts are increasingly positioned as an economical plant protein source amid global dietary transitions toward vegetarian and flexitarian consumption. Food manufacturers are incorporating peanut flour, peanut protein isolates, and roasted peanut inclusions into energy bars, protein beverages, and meat alternatives. Compared with soy and almond protein, peanuts offer cost advantages and strong amino acid profiles, encouraging adoption in emerging markets. Functional food brands are actively reformulating products using peanut-derived ingredients to enhance protein content without significantly increasing retail prices.

Premiumization and Value-Added Peanut Products

The market is witnessing strong growth in premium peanut-based offerings such as flavored peanut butter, organic roasted peanuts, and specialty confectionery ingredients. Consumers increasingly prefer minimally processed and traceable agricultural products, prompting manufacturers to invest in origin certification and sustainable sourcing. Innovations such as honey-roasted variants, coated peanuts, and fortified spreads are expanding retail shelf presence globally. E-commerce platforms are also accelerating direct-to-consumer sales of specialty peanut products, strengthening margins for branded manufacturers.

What are the key drivers in the peanuts market?

Rising Global Snack Consumption

Urban lifestyles and convenience-oriented eating habits have significantly increased demand for ready-to-eat snacks. Peanuts serve as a core ingredient in packaged snacks due to their affordability, shelf stability, and nutritional value. Expansion of modern retail and quick-commerce platforms has further accelerated consumption across Asia-Pacific and Latin America.

Expansion of Peanut Oil Applications

Peanut oil continues to gain traction in foodservice and household cooking owing to its high smoke point and favorable flavor profile. Rapid growth in quick-service restaurants across emerging economies has supported bulk peanut oil demand, particularly in Asia.

Improved Agricultural Productivity

Advancements in seed technology, irrigation practices, and mechanized harvesting have improved yield per hectare. Government-backed agricultural modernization programs are enhancing supply consistency, reducing price volatility, and supporting market expansion.

What are the restraints for the global market?

Climate Sensitivity and Yield Volatility

Peanut cultivation remains highly dependent on rainfall patterns and soil conditions. Climate variability, drought risks, and pest outbreaks can significantly impact production volumes, creating supply instability and price fluctuations.

Allergen Concerns and Regulatory Restrictions

Peanut allergies remain a significant concern in developed markets, leading to stringent labeling requirements and limiting adoption in certain food categories. Manufacturers must invest in allergen management systems, increasing operational costs.

What are the key opportunities in the peanuts industry?

Growth of Peanut-Based Functional Foods

The expansion of sports nutrition and functional foods presents a major opportunity for peanut processors. Peanut protein powders and fortified spreads are gaining popularity among health-conscious consumers. Manufacturers entering nutraceutical and wellness food segments can capture premium margins while diversifying revenue streams.

Emerging Market Consumption Expansion

Rapid population growth and rising disposable income across Southeast Asia and Africa are creating new consumption hubs. Governments promoting oilseed self-sufficiency are encouraging domestic peanut processing industries, opening opportunities for investment in local crushing and roasting facilities.

Technology Integration in Processing

Automation in sorting, grading, and roasting processes is improving efficiency and reducing post-harvest losses. Digital traceability systems and AI-based quality inspection technologies are enabling exporters to meet strict international quality standards, strengthening global trade competitiveness.

Product Type Insights

The global peanuts market demonstrates a highly diversified product structure shaped by evolving consumption patterns, industrial applications, and regional dietary preferences. Among all product categories, raw peanuts continue to dominate the market landscape, accounting for nearly 38% of the global market share in 2025. The leadership of this segment is primarily driven by its versatility across multiple downstream industries. Raw peanuts serve as the foundational agricultural commodity for oil extraction, peanut butter manufacturing, flour production, confectionery processing, and protein ingredient formulation. Their relatively lower processing cost compared to value-added variants enables large-scale procurement by processors and exporters, especially across Asia-Pacific and Latin America. In addition, growing investments in peanut crushing facilities and edible oil production capacities in developing economies continue to strengthen demand for unprocessed kernels.The sustained expansion of the raw peanut segment is further supported by increasing global edible oil consumption, particularly in emerging economies where peanut oil remains a staple cooking medium. Industrial buyers favor raw peanuts due to flexibility in processing customization, allowing manufacturers to optimize roasting levels, oil yields, and ingredient formulations according to specific product requirements. Furthermore, improved seed varieties, mechanized harvesting practices, and better storage infrastructure have enhanced supply consistency, reinforcing the segment’s dominant position within global trade networks.Processed peanuts, including roasted, salted, coated, and flavored variants, account for approximately 27% of market share and represent one of the fastest-evolving segments within the industry. Growth in this category is closely linked to the global expansion of packaged snack consumption and changing urban lifestyles. Increasing working populations, rising disposable incomes, and demand for convenient, ready-to-eat protein snacks have accelerated product innovation among food manufacturers. Companies are increasingly introducing flavored peanuts tailored to regional taste preferences, such as spicy variants in Asia, honey-roasted products in North America, and gourmet seasoning blends in Europe.The processed peanut segment also benefits from the premiumization trend in snack foods, where consumers increasingly seek healthier alternatives to traditional fried snacks. Peanuts offer a natural combination of protein, healthy fats, and micronutrients, positioning them as a functional snack aligned with wellness-oriented consumption behavior. Growth in modern retail channels and online grocery platforms has significantly enhanced brand visibility and accessibility, allowing manufacturers to expand market penetration across urban and semi-urban regions.Peanut oil represents nearly 22% of global market share, supported by strong culinary traditions and expanding foodservice demand across Asia-Pacific and parts of Africa. The leading driver of this segment is the growing preference for oils with high smoke points and favorable fatty acid profiles suitable for deep frying and high-temperature cooking. Peanut oil’s stability, flavor neutrality, and perceived health benefits contribute to sustained adoption among households and commercial kitchens. Rapid expansion of quick-service restaurants, street food culture, and packaged food manufacturing has further strengthened demand for bulk edible oils.Additionally, rising awareness regarding plant-based cooking ingredients and increasing substitution away from animal fats in several regions are encouraging peanut oil consumption.

Application Insights

From an application perspective, the food processing industry remains the dominant consumer of peanuts globally, accounting for nearly 52% market share in 2025. The leading driver of this segment is the expanding global processed food ecosystem, including bakery products, confectionery, ready-to-eat snacks, spreads, sauces, and protein bars. Peanuts provide manufacturers with a cost-effective ingredient offering flavor enhancement, texture improvement, and nutritional enrichment. Their adaptability across sweet and savory formulations makes them indispensable within industrial food production.Rapid urbanization and increasing reliance on packaged foods have significantly increased demand for peanut-based ingredients among large-scale processors. Confectionery manufacturers, in particular, rely heavily on peanuts as inclusions in chocolates, candies, and coated snacks due to favorable pricing compared with tree nuts such as almonds and cashews. Continuous innovation in product formulations, including reduced-sugar snacks and high-protein bakery items, further reinforces peanut utilization across food manufacturing operations.Oil crushing applications account for approximately 26% of total demand, supported by expanding edible oil consumption worldwide. The primary growth driver for this segment is rising cooking oil demand in densely populated developing countries, where affordability and availability strongly influence consumer choices. Peanut crushing generates both edible oil and protein-rich meal, improving economic efficiency for processors and supporting integrated value chains.Direct snack consumption represents around 15% of applications, reflecting strong retail demand for roasted and flavored peanut products. Increasing awareness of healthy snacking alternatives has encouraged consumers to replace traditional high-carbohydrate snacks with protein-rich options. Marketing strategies emphasizing natural ingredients, clean-label products, and energy-boosting nutrition continue to drive expansion in this category.Meanwhile, animal feed and industrial applications collectively account for the remaining share but are witnessing steady growth due to rising utilization of peanut meal as a protein supplement in livestock feed formulations. As global meat and dairy production expands, demand for cost-effective feed ingredients continues to rise, indirectly supporting peanut processing industries. Industrial applications, including cosmetics and bio-based products, are also emerging niches contributing incremental demand.

Distribution Channel Insights

The distribution landscape of the global peanuts market reflects the agricultural commodity nature of the industry combined with the growing importance of branded consumer products. Indirect distribution channels, including commodity traders, exporters, wholesalers, and agricultural cooperatives, continue to dominate global trade volumes. The leading driver behind this dominance is the large-scale bulk movement of peanuts across international supply chains, particularly between producing countries such as China, India, Argentina, and importing regions in Europe and the Middle East.Commodity trading networks play a critical role in price discovery, logistics coordination, and quality standardization. These intermediaries facilitate cross-border transactions, manage storage infrastructure, and ensure supply continuity for industrial buyers. Long-term contracts between producers and processors help stabilize procurement costs and reduce supply volatility, reinforcing reliance on indirect channels.However, direct and branded retail distribution is expanding rapidly, supported by the modernization of food retail ecosystems. Supermarkets, hypermarkets, convenience stores, and e-commerce grocery platforms are increasingly promoting packaged peanut products with higher margins. The leading growth driver for retail expansion is consumer preference for branded, hygienically packaged, and traceable food products.Online grocery platforms are particularly influential in accelerating premium peanut product sales, enabling smaller brands to reach broader audiences without extensive physical retail infrastructure. Digital marketing, subscription snack services, and direct-to-consumer models are reshaping distribution strategies, especially in urban markets where convenience and product variety strongly influence purchasing behavior.

End-Use Industry Analysis

The food & beverage industry remains the largest end-use sector for peanuts, generating consumption demand valued at over USD 55 billion in 2025. The primary driver behind this dominance is the widespread incorporation of peanuts into multiple food categories ranging from snacks and confectionery to sauces, spreads, and ready meals. Manufacturers value peanuts for their nutritional density, flavor profile, and cost efficiency compared to alternative nuts and protein ingredients.The snack food industry is expanding at an annual growth rate exceeding 7%, driven by global shifts toward high-protein and energy-rich snacking habits. Increasing participation in fitness activities and growing awareness of balanced nutrition have encouraged consumers to adopt protein-based snacks, positioning peanuts as a preferred ingredient due to affordability and natural nutritional benefits.Within the confectionery sector, peanuts are increasingly utilized in chocolate bars, coated candies, and dessert toppings. Manufacturers favor peanuts because they provide texture contrast and flavor enhancement while maintaining competitive pricing structures. Rising demand for indulgent yet affordable confectionery products across emerging markets further strengthens this segment.Foodservice demand is also expanding steadily as global quick-service restaurant chains and casual dining establishments incorporate peanut-based sauces, toppings, and cooking oils into menus. Growth in urban dining culture, food delivery services, and international cuisine adoption supports incremental peanut consumption across hospitality channels.Export-driven demand continues to play a crucial role in shaping global market dynamics. Major producing countries such as China, India, and Argentina supply large volumes to Europe and Southeast Asia, ensuring year-round availability despite seasonal production cycles. Improvements in logistics infrastructure, cold storage facilities, and quality certification standards are facilitating smoother international trade flows.Emerging applications in plant-based dairy alternatives, protein powders, and functional foods represent a transformative opportunity for the industry. As consumers increasingly shift toward sustainable and plant-derived nutrition, peanuts are gaining recognition as an economical protein source suitable for innovative formulations. Continued investment in research and product development is expected to unlock new industrial applications over the forecast period.

| By Product Type | By Application | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global peanuts market, accounting for approximately 46% of market share in 2025, supported by strong agricultural production capacity, large consumer populations, and deeply embedded culinary traditions. China remains the world’s largest producer and consumer, with demand driven primarily by peanut oil consumption, snack manufacturing, and domestic food processing industries. The country benefits from extensive cultivation areas, government-backed agricultural modernization programs, and advanced processing infrastructure.India represents another major contributor to regional growth, supported by favorable climatic conditions, expanding export opportunities, and policy initiatives encouraging oilseed production. Government incentives aimed at improving farmer income, irrigation systems, and seed quality are strengthening productivity levels. Rising domestic consumption of peanut-based snacks and increasing demand from international buyers further enhance India’s market position.Southeast Asian countries such as Vietnam and Indonesia are experiencing rapid growth in peanut oil consumption due to rising urban populations and expanding foodservice sectors. Increasing disposable income levels, modernization of retail networks, and growing demand for affordable edible oils act as key regional growth drivers. Additionally, the presence of large processing hubs and proximity to major export markets provide Asia-Pacific with significant logistical advantages, reinforcing its leadership in global supply chains.

North America

North America accounts for nearly 18% of global market share, led primarily by the United States, which functions as both a major exporter and one of the largest consumers of peanut-based products. The leading driver of regional growth is strong demand for peanut butter, supported by longstanding consumer familiarity and expanding health-conscious dietary trends. Peanuts are widely perceived as a nutritious, affordable protein source, aligning with increasing adoption of fitness-oriented lifestyles.Innovation within the food industry continues to drive market expansion, with manufacturers introducing organic, low-sugar, and fortified peanut products targeting premium consumer segments. Growth in plant-based diets and functional foods further strengthens demand for peanut ingredients across protein bars, smoothies, and alternative dairy products. Advanced farming technologies, mechanized harvesting, and efficient supply chain systems enable consistent production quality and export competitiveness.

Europe

Europe represents approximately 14% of global market share and remains heavily dependent on imports due to limited domestic cultivation. Germany, the Netherlands, and the United Kingdom function as major processing and redistribution hubs, importing shelled peanuts primarily for confectionery and snack manufacturing. The leading driver of regional growth is strong demand for processed and value-added peanut products within premium snack and chocolate categories.European consumers increasingly prioritize clean-label foods, sustainability certifications, and ethically sourced ingredients, encouraging importers to establish transparent supply chains. Rising popularity of plant-based diets across Western Europe also supports growth in peanut butter and peanut-based protein products. Expansion of private-label snack brands by large retail chains further accelerates peanut consumption throughout the region.

Latin America

Latin America, led by Argentina and Brazil, serves primarily as an export-oriented production region within the global peanuts market. Argentina stands out as one of the fastest-growing exporters due to high-quality peanut varieties, advanced processing facilities, and strong compliance with international quality standards. The leading driver for regional growth is increasing global demand for premium-grade peanuts used in confectionery and snack manufacturing.Investment in modern agricultural practices, improved irrigation systems, and export-focused infrastructure has enhanced productivity and global competitiveness. Brazil is also expanding domestic consumption alongside growing food processing industries. Favorable trade agreements and rising demand from Europe and Asia continue to strengthen Latin America’s role as a critical supplier within global peanut trade networks.

Middle East & Africa

The Middle East and Africa collectively account for nearly 10% of global market share, characterized by a combination of emerging production centers and strong import demand. Countries such as Nigeria and Sudan are expanding peanut cultivation due to favorable agro-climatic conditions and increasing government focus on agricultural diversification. The leading growth driver in African markets is rising investment in oilseed farming aimed at improving food security and export revenues.Meanwhile, Gulf countries drive significant import demand fueled by growing populations, expanding retail sectors, and strong snack consumption culture. Urbanization, rising disposable incomes, and increasing availability of packaged foods are accelerating peanut product adoption across the region. Africa is projected to be the fastest-growing regional market, with growth exceeding 7.5% CAGR, supported by improving agricultural productivity, expanding processing capabilities, and rising intra-regional trade.Overall, regional market expansion is shaped by a combination of population growth, dietary diversification, industrial food processing development, and expanding global trade networks. As supply chains become more integrated and demand for plant-based protein sources increases worldwide, peanuts are expected to maintain a strategically important role within the global agricultural and food ingredients economy throughout the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Global Peanuts Market

- Olam Group

- Golden Peanut and Tree Nuts

- China National Cereals, Oils and Foodstuffs Corporation (COFCO)

- Archer Daniels Midland Company

- Bunge Limited

- Hampton Farms

- Birdsong Peanuts

- Virginia Diner Inc.

- Shandong Jinsheng Cereals & Oils Group

- Gansu Dunhuang Seed Group

- Grupo Maní Argentina

- John B. Sanfilippo & Son, Inc.

- Mount Franklin Foods

- Royal Nut Company

- Durak Findik (Peanut Processing Division)