Peanut Allergy Treatment Market Size

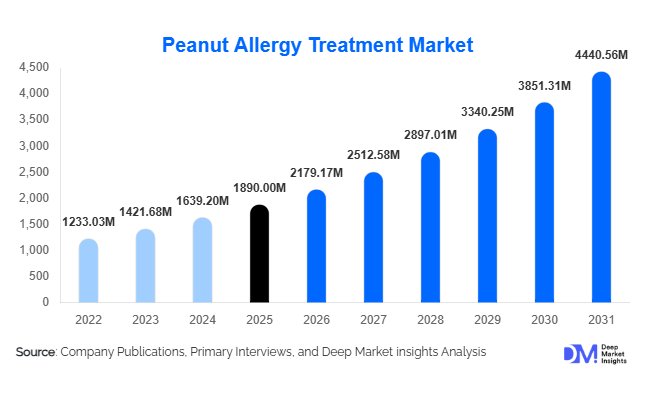

According to Deep Market Insights, the global peanut allergy treatment market size was valued at USD 1,890 million in 2025 and is projected to grow from USD 2,179.17 million in 2026 to reach USD 4,440.56 million by 2031, expanding at a CAGR of 15.3% during the forecast period (2026–2031). Market growth is primarily driven by the rising global prevalence of peanut allergies, increasing adoption of disease-modifying immunotherapies, and growing healthcare investments focused on preventive allergy management. The transition from emergency reaction treatment toward long-term immune tolerance therapies is significantly reshaping treatment protocols worldwide. Pharmaceutical innovation, expanding pediatric diagnosis programs, and favorable regulatory pathways for biologics and immunotherapies are further accelerating market expansion. Increasing awareness among caregivers and healthcare providers, combined with improved reimbursement frameworks in developed markets, continues to support adoption of standardized allergy treatments globally.

Key Market Insights

- Oral immunotherapy is transforming peanut allergy management, shifting treatment from emergency care toward long-term desensitization strategies.

- Pediatric patients account for the largest demand share, supported by early diagnosis and preventive treatment adoption.

- North America dominates the global market, driven by strong reimbursement systems and early therapy approvals.

- Asia-Pacific is the fastest-growing region, supported by rising allergy awareness and expanding specialty healthcare infrastructure.

- Biologic therapies and monoclonal antibodies are emerging as next-generation treatment options improving safety and efficacy outcomes.

- Digital monitoring and personalized dosing technologies are improving treatment adherence and patient outcomes globally.

What are the latest trends in the peanut allergy treatment market?

Shift Toward Disease-Modifying Immunotherapies

The peanut allergy treatment landscape is evolving from reactive emergency management toward therapies designed to modify immune response over time. Oral and epicutaneous immunotherapies are gaining strong clinical acceptance as they reduce the severity of allergic reactions and improve patient tolerance thresholds. Healthcare providers increasingly recommend early intervention strategies, particularly among pediatric populations, to prevent severe lifelong allergy risks. Pharmaceutical companies are investing heavily in standardized allergen formulations and long-term treatment protocols that provide measurable clinical outcomes. This transition is redefining patient care models and creating recurring revenue opportunities for therapy providers.

Integration of Biologics and Precision Medicine

Advances in immunology research are enabling targeted biologic therapies that regulate immune pathways responsible for allergic reactions. Anti-IgE monoclonal antibodies and cytokine-targeting drugs are increasingly used alongside immunotherapy to enhance safety and treatment success rates. Precision medicine approaches are allowing physicians to customize dosing schedules based on patient sensitivity levels, improving adherence and minimizing adverse events. Digital health tools, including mobile monitoring platforms and tele-allergy consultations, are supporting remote treatment supervision and expanding accessibility beyond hospital environments.

What are the key drivers in the peanut allergy treatment market?

Rising Global Allergy Prevalence

The increasing incidence of peanut allergies worldwide represents a major growth driver for the market. Urbanization, dietary shifts, environmental exposure, and improved diagnostic practices have contributed to higher allergy detection rates, particularly among children. Growing awareness among parents and schools regarding severe allergic reactions has increased demand for long-term preventive therapies rather than emergency-only solutions.

Regulatory Support and Clinical Innovation

Regulatory agencies are accelerating approvals for innovative allergy therapies addressing unmet medical needs. Fast-track pathways and orphan drug incentives have encouraged pharmaceutical investment in immunotherapy and biologic development. Continuous clinical trial activity is expanding treatment indications across broader patient populations, supporting sustained market growth.

What are the restraints for the global market?

High Treatment Costs and Limited Accessibility

Peanut allergy immunotherapies require prolonged treatment cycles and clinical supervision, increasing overall healthcare costs. Limited reimbursement availability in developing economies restricts patient access, slowing adoption despite rising diagnosis rates. Pricing remains a challenge for widespread penetration outside developed healthcare systems.

Safety Concerns and Patient Compliance Challenges

Immunotherapy treatments involve controlled allergen exposure, which may trigger reactions during dose escalation phases. Patient anxiety, strict adherence requirements, and long treatment durations can affect compliance levels. Ensuring safety while maintaining treatment effectiveness remains a key industry challenge.

What are the key opportunities in the peanut allergy treatment industry?

Expansion into Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East represent significant untapped demand due to historically low diagnosis rates. Growing healthcare investments, urbanization, and increasing awareness programs are expanding treatment accessibility. Companies entering early can establish strong physician networks and localized distribution strategies.

Combination Therapies and Digital Health Integration

The integration of biologics with immunotherapy treatments presents substantial growth potential by improving safety outcomes and accelerating desensitization. Digital monitoring platforms, wearable allergy trackers, and telemedicine solutions enable remote supervision and personalized therapy adjustments. These innovations are expected to enhance patient adherence and expand treatment adoption globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1890 Million |

| Market Size in 2026 | USD 2179.17 Million |

| Market Size in 2031 | USD 4440.56 Million |

| CAGR | 15.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Treatment Type Insights

The peanut allergy treatment market is undergoing a significant transition from reactive emergency management toward long-term disease-modifying therapies, with oral immunotherapy emerging as the dominant treatment approach and accounting for nearly 38% of global demand. The leadership of oral immunotherapy is primarily driven by its clinically validated ability to induce immune desensitization through controlled allergen exposure, particularly among pediatric patients where early intervention improves long-term tolerance outcomes. Increasing regulatory approvals, standardized dosing protocols, and growing physician confidence have accelerated adoption across specialized allergy centers. Furthermore, improved patient adherence supported by structured escalation programs and caregiver education initiatives has strengthened the commercial viability of oral therapies.Epicutaneous immunotherapy is gaining substantial traction as a non-invasive treatment alternative, particularly for younger children and patients who demonstrate intolerance toward oral dose escalation. The development of skin-based delivery systems enables gradual allergen exposure with a favorable safety profile, reducing systemic reaction risks and improving treatment acceptance among risk-averse caregivers. Continuous innovation in patch technologies and enhanced drug delivery mechanisms are expected to expand clinical applicability over the coming years.Biologic therapies represent one of the fastest-evolving areas within peanut allergy treatment, offering targeted immune modulation by addressing underlying immunological pathways rather than symptoms alone. Monoclonal antibodies are increasingly being integrated alongside immunotherapy programs to improve desensitization success rates and reduce adverse reactions during treatment escalation phases. Growing investment in precision medicine, combined with expanding clinical trial pipelines, is expected to position biologics as a complementary cornerstone therapy for severe allergy profiles.Emergency management treatments, particularly epinephrine auto-injectors, continue to play a critical safety role across all patient groups. However, their market positioning is gradually shifting from primary management solutions toward supportive and rescue therapy functions as preventive and disease-modifying treatments gain widespread adoption. Increased awareness campaigns and school-based safety programs continue to sustain baseline demand for emergency interventions worldwide.

Route of Administration Insights

Oral administration leads the peanut allergy treatment market with approximately 45% share, supported by strong patient familiarity, ease of administration, and the ability to transition treatment from clinical supervision to home-based maintenance phases. The leading position of oral administration is driven by its scalability within healthcare systems, allowing physicians to initiate therapy in controlled environments while enabling long-term adherence through homecare protocols. Advancements in formulation stability, dosing precision, and patient monitoring technologies have further enhanced treatment safety and convenience, reinforcing adoption across both developed and emerging healthcare markets.Injectable administration is experiencing steady expansion, largely fueled by the growing adoption of biologic therapies designed to target immune system pathways responsible for allergic responses. Injectable biologics are particularly valuable for patients with severe or multi-allergen sensitivities, offering improved symptom control and reduced risk of systemic reactions. Increased physician preference for combination therapy approaches and expanding reimbursement frameworks are supporting the gradual penetration of injectable treatments.Transdermal patches and sublingual therapies are emerging as important alternatives that diversify treatment accessibility. These approaches address unmet needs among patients unable to tolerate oral immunotherapy escalation protocols and offer improved safety perception among caregivers. Continued research into controlled allergen delivery and reduced adverse event profiles is expected to drive broader clinical acceptance, contributing to long-term market diversification.

End-Use Insights

Allergy and immunology clinics represent the leading end-use segment, accounting for nearly 36% of global demand, primarily due to the specialized supervision required during immunotherapy initiation and dose escalation phases. The dominance of this segment is supported by the availability of trained allergists, advanced diagnostic capabilities, and emergency response infrastructure necessary for managing potential allergic reactions. Increasing establishment of dedicated allergy centers and integrated care models is strengthening the role of specialty clinics as primary treatment hubs.Hospitals continue to play a vital role in diagnosis, acute reaction management, and treatment initiation, particularly for high-risk patients requiring intensive monitoring. The presence of multidisciplinary care teams and access to advanced diagnostic technologies ensures hospitals remain central to early-stage treatment pathways.Homecare settings are emerging as the fastest-growing end-use environment, driven by advancements in telemedicine, digital health monitoring, and remote patient supervision platforms. Once patients stabilize during clinical initiation, maintenance therapy increasingly shifts toward home-based administration, improving treatment adherence while reducing healthcare system burden. The expansion of connected healthcare ecosystems is expected to accelerate this transition significantly.Academic and research institutions are also contributing to market expansion through ongoing clinical trials, therapy optimization studies, and innovation in immunomodulatory treatments. Collaborations between pharmaceutical companies and research organizations are accelerating therapy development and supporting evidence-based adoption globally.

Age Group Insights

The pediatric population dominates market demand with approximately 52% share, supported by growing awareness of early diagnosis benefits and clinical evidence demonstrating that early immune intervention improves long-term tolerance development. The leading position of this segment is driven by increased screening programs, school-based allergy awareness initiatives, and strong parental willingness to pursue preventive treatment strategies. Pediatric-focused clinical trials and regulatory approvals tailored toward younger populations further reinforce segment growth.Adolescents represent an expanding treatment population as therapy continuation into teenage years becomes increasingly common. Improved long-term safety data and structured treatment maintenance programs are encouraging sustained therapy adherence, reducing the risk of severe allergic reactions during a life stage associated with higher exposure risks.Adult treatment adoption is gradually increasing, supported by the introduction of biologic therapies capable of managing severe and persistent allergy cases. Growing diagnosis rates among adults and increased awareness of treatment availability are expected to drive steady expansion of this segment over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Peanut Allergy Treatment Market Segmentations

By Treatment Type

- Oral Immunotherapy

- Epicutaneous Immunotherapy

- Sublingual Immunotherapy

- Biologic Therapies

- Emergency Management Treatments

- Adjunct Combination Therapies

By Route of Administration

- Oral

- Injectable

- Transdermal Patch

- Sublingual

By End-Use

- Hospitals

- Allergy Immunology Clinics

- Homecare Settings

- Research Academic Institutes

By Age Group

- Pediatric

- Adolescents

- Adults

- Older Adults

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Allergy Clinics

Regional Insights

North America

North America accounts for approximately 42% of the global peanut allergy treatment market, led primarily by the United States, which benefits from high diagnosis rates, advanced healthcare infrastructure, and strong insurance reimbursement frameworks supporting immunotherapy adoption. Regional growth is further driven by early regulatory approvals for novel therapies, widespread availability of allergy specialists, and strong patient advocacy networks promoting proactive treatment adoption. Increasing prevalence of food allergies among children, combined with high healthcare expenditure and rapid integration of biologic therapies, continues to strengthen market leadership. Canada is witnessing steady growth supported by expanding pediatric allergy programs, government-funded healthcare access, and national awareness initiatives aimed at improving early intervention and preventive care outcomes.

Europe

Europe holds nearly 28% market share, with Germany, the United Kingdom, and France serving as major contributors due to robust clinical research ecosystems and structured allergy management frameworks. Regional growth is supported by harmonized treatment guidelines, strong collaboration between academic institutions and pharmaceutical companies, and rising investments in immunology research. Preventive healthcare policies and reimbursement support for innovative therapies are encouraging adoption across Western Europe, while increasing awareness campaigns and improved diagnostic capabilities are expanding treatment access in Central and Eastern European countries. Growing emphasis on personalized medicine and long-term disease management strategies further strengthens regional market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at an estimated CAGR of around 18%, driven by rapidly increasing allergy prevalence associated with urbanization, environmental changes, and evolving dietary habits. Countries including China, Japan, South Korea, and India are experiencing rising diagnosis rates as healthcare awareness improves and specialty allergy clinics expand across urban centers. Government investments in healthcare infrastructure, growing middle-class populations, and increasing access to advanced diagnostics are accelerating treatment adoption. Additionally, pharmaceutical companies are expanding regional clinical trials and partnerships to address unmet needs, while telehealth adoption and digital health platforms are improving patient access to specialist care across geographically diverse populations.

Latin America

Latin America is witnessing gradual but consistent market expansion, led by Brazil and Mexico where improving private healthcare investments are enhancing access to advanced allergy treatments. Regional growth is supported by increasing physician education programs, rising awareness of food allergy risks, and expansion of urban healthcare infrastructure. Growing participation of multinational pharmaceutical companies and improved regulatory pathways are facilitating the introduction of innovative therapies. Expanding middle-income populations and greater healthcare insurance penetration are expected to further support treatment accessibility over the forecast period.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth driven by healthcare modernization initiatives, particularly in the United Arab Emirates and Saudi Arabia, where investments in specialty healthcare services are expanding allergy diagnosis and treatment capabilities. Rising expatriate populations, increased adoption of Western dietary patterns, and improved physician training programs are contributing to higher diagnosis rates. Government-led healthcare diversification strategies and expansion of private healthcare providers are improving access to advanced therapies. In Africa, gradual improvements in diagnostic infrastructure and growing awareness initiatives are expected to support long-term market development despite existing healthcare access challenges.

Key Players in the Peanut Allergy Treatment Market

- Aimmune Therapeutics

- DBV Technologies

- Genentech Inc.

- Novartis AG

- Sanofi S.A.

- Regeneron Pharmaceuticals Inc.

- Stallergenes Greer

- HAL Allergy Group

- Allergy Therapeutics plc

- ALK-Abelló A/S

- Viatris Inc.

- Pfizer Inc.

- AstraZeneca plc

- Teva Pharmaceutical Industries Ltd.

- Johnson & Johnson