Pea Protein Powder Market Size

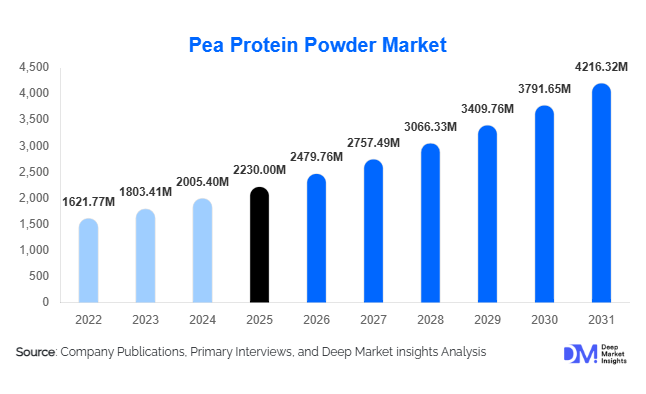

According to Deep Market Insights,the global pea protein powder market size was valued at USD 2,230 million in 2025 and is projected to grow from USD 2,479.76 million in 2026 to reach USD 4,216.32 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The pea protein powder market growth is primarily driven by rising adoption of plant-based diets, increasing demand for allergen-free protein ingredients, and rapid expansion of plant-based meat and dairy alternative industries worldwide. Growing consumer focus on sustainability, clean-label nutrition, and functional food innovation continues to position pea protein as a preferred alternative to soy and dairy proteins across global food systems.

Key Market Insights

- Plant-based protein consumption is accelerating globally, with pea protein emerging as a leading hypoallergenic alternative to soy and whey proteins.

- Food and beverage applications dominate demand, particularly dairy alternatives, meat substitutes, and functional snacks.

- North America leads global consumption due to advanced plant-based food ecosystems and strong consumer awareness.

- Asia-Pacific is the fastest-growing region, supported by urbanization, rising disposable income, and expanding food processing industries.

- Technological advancements in protein extraction are improving taste neutrality and solubility, enabling wider beverage applications.

- Sustainability advantages, including lower water usage and carbon footprint compared with animal proteins, are boosting adoption among manufacturers.

What are the latest trends in the pea protein powder market?

Shift Toward Clean-Label and Allergen-Free Nutrition

Consumers increasingly prefer minimally processed, transparent-label food products, driving adoption of pea protein powder as a clean-label ingredient. Unlike soy and dairy proteins, pea protein is naturally gluten-free, lactose-free, and non-allergenic, making it suitable for a broader consumer base. Food manufacturers are reformulating legacy products to remove artificial additives and allergens while maintaining protein fortification levels. This trend is especially strong in North America and Europe, where regulatory scrutiny and consumer awareness around ingredient sourcing continue to increase. Brands are also highlighting non-GMO certification and traceability, positioning pea protein as a premium functional ingredient aligned with wellness-focused consumption patterns.

Expansion of Plant-Based Meat and Dairy Innovation

Rapid innovation within plant-based foods is reshaping demand dynamics for pea protein powder. Manufacturers are leveraging its emulsification and texturizing properties to replicate meat textures and improve mouthfeel in dairy alternatives. New-generation plant-based burgers, sausages, protein beverages, and ready-to-drink shakes increasingly rely on pea protein isolates for improved nutritional profiles. Advances in flavor masking and fermentation technologies are addressing earlier sensory challenges, enabling wider usage across beverages and clinical nutrition products. Product diversification across ready meals, fortified bakery products, and high-protein snacks is further accelerating ingredient adoption globally.

What are the key drivers in the pea protein powder market?

Rising Demand for Plant-Based Diets

Growing awareness of environmental sustainability and health benefits associated with plant-based nutrition is significantly driving pea protein consumption. Flexitarian consumers are reducing animal protein intake while maintaining protein consumption levels, boosting demand for plant-derived alternatives. Pea protein offers a balanced amino acid profile and aligns well with vegan and ethical consumption trends, encouraging widespread adoption across mainstream food categories.

Growth of Sports and Functional Nutrition

The global fitness and wellness movement is expanding protein consumption beyond athletes into everyday consumers. Pea protein powder is increasingly incorporated into protein shakes, meal replacements, and recovery products due to its digestibility and compatibility with vegan diets. Aging populations seeking muscle maintenance and metabolic health solutions are also contributing to sustained demand growth within functional nutrition applications.

What are the restraints for the global market?

Raw Material Price Volatility

The pea protein supply chain depends heavily on agricultural output of yellow peas, making pricing vulnerable to climate variability and crop yield fluctuations. Supply disruptions can increase production costs and compress manufacturer margins, particularly for small and mid-scale processors.

Functional and Taste Limitations

Despite technological improvements, pea protein may still exhibit earthy flavor notes and lower solubility compared with whey protein in certain beverage applications. Additional processing required to enhance sensory performance increases costs, creating adoption challenges in price-sensitive markets.

What are the key opportunities in the pea protein powder industry?

Emerging Market Expansion

Rapid urbanization and changing dietary habits across Asia-Pacific and Latin America present strong growth opportunities. Rising lactose intolerance rates and increasing protein consumption are encouraging manufacturers to introduce plant-based formulations tailored to regional taste preferences. Establishing local processing facilities in emerging economies can reduce logistics costs and improve supply reliability.

Technological Innovation in Protein Processing

Advanced extraction, fermentation, and enzymatic hydrolysis technologies are improving protein functionality and expanding application scope. Companies investing in proprietary processing techniques can produce higher-purity isolates with superior taste and solubility, enabling premium pricing and long-term supply agreements with multinational food manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2230 Million |

| Market Size in 2026 | USD 2479.76 Million |

| Market Size in 2031 | USD 4216.32 Million |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The pea protein powder market is primarily led by pea protein isolate, which accounts for the largest revenue share owing to its high protein concentration, neutral flavor profile, and superior solubility across multiple food and beverage applications. The increasing demand for clean-label, allergen-free, and highly functional plant proteins has positioned isolates as the preferred ingredient in dairy alternatives, ready-to-drink beverages, and plant-based meat analogs. Food manufacturers increasingly favor isolates due to their ability to deliver improved emulsification, texture stability, and protein fortification without compromising taste or formulation consistency. Pea protein concentrates continue to maintain significant adoption within cost-sensitive food applications, including bakery products, snacks, and processed foods, where moderate protein enrichment is sufficient while maintaining pricing competitiveness. Textured pea protein is experiencing accelerated growth driven by rapid expansion of the plant-based meat industry, as it enables manufacturers to replicate fibrous meat-like textures and improve sensory performance in alternative protein products. Meanwhile, hydrolyzed pea protein is emerging as a specialized segment, particularly in clinical nutrition, infant nutrition, and medical dietary formulations where enhanced digestibility and rapid amino acid absorption are essential. The growing focus on high-performance nutrition, functional foods, and sustainable protein sourcing is expected to reinforce isolate segment leadership throughout the forecast period.

Application Insights

Food and beverage applications represent the dominant share of global pea protein powder consumption, primarily driven by rising demand for dairy alternatives, plant-based meat substitutes, protein-enriched snacks, and functional beverages. Manufacturers are increasingly incorporating pea protein to meet consumer preferences for vegan, lactose-free, and allergen-friendly products while supporting nutritional fortification initiatives. The nutritional supplements segment is witnessing rapid expansion as fitness-conscious consumers, athletes, and lifestyle-focused individuals shift toward plant-based protein powders as alternatives to whey and soy proteins. Growing awareness of muscle recovery, weight management, and holistic wellness is further accelerating supplement adoption. Animal nutrition applications are emerging steadily, particularly in premium pet food and aquaculture formulations where plant-based protein ingredients provide sustainability advantages and diversified protein sourcing. Personal care applications remain comparatively niche but are gaining traction as cosmetic and skincare manufacturers experiment with plant-derived proteins to enhance product functionality, including hair strengthening, skin conditioning, and natural formulation positioning. Continuous innovation across food science and functional ingredient development is expected to broaden application scope over the coming years.

Distribution Channel Insights

B2B industrial distribution channels dominate the pea protein powder market, as large-scale food and beverage manufacturers procure bulk quantities for product development and commercial production. Long-term supply agreements between ingredient suppliers and multinational food companies are enhancing procurement stability while supporting predictable demand patterns. Retail distribution is expanding steadily, supported by growing consumer interest in plant-based nutrition products and increasing availability of branded protein powders through supermarkets, specialty health stores, and wellness outlets. E-commerce platforms are becoming a critical growth engine, enabling emerging brands and direct-to-consumer nutrition companies to reach global audiences without extensive physical retail investments. Digital marketplaces also facilitate product education, subscription models, and personalized nutrition offerings, strengthening consumer engagement and accelerating adoption. The integration of omnichannel distribution strategies is expected to further enhance market accessibility and brand visibility worldwide.

End-Use Industry Insights

The food processing industry remains the largest end-use sector for pea protein powder, supported by continuous innovation in plant-based foods, reformulation initiatives, and rising demand for protein fortification across mainstream food categories. The leading driver for this segment is the global shift toward sustainable and alternative protein ingredients that align with environmental and health-conscious consumption trends. The sports nutrition industry represents one of the fastest-growing end-use segments, fueled by increasing adoption of vegan protein supplements among athletes and active consumers seeking clean-label performance nutrition solutions. The plant-based meat industry is expanding rapidly and significantly increasing industrial demand for textured pea protein, as manufacturers seek scalable protein solutions capable of delivering realistic texture and nutritional equivalence to animal protein. Additionally, emerging applications within clinical nutrition and premium pet food sectors are diversifying market opportunities, supported by growing emphasis on digestibility, functional nutrition, and specialized dietary formulations, thereby enhancing long-term market resilience.

Explore more data points, trends and opportunities Download Free Sample Report

Pea Protein Powder Market Segmentations

By Product Type

- Pea Protein Isolate

- Pea Protein Concentrate

- Textured Pea Protein

- Hydrolyzed Pea Protein

By Application

- Food & Beverage Products

- Nutritional Supplements

- Plant-Based Meat Alternatives

- Animal Nutrition & Pet Food

- Personal Care & Cosmetics

By Distribution Channel

- B2B Ingredient Supply

- Online Retail & E-commerce

- Supermarkets & Hypermarkets

- Health & Specialty Stores

- Direct Manufacturer Sales

By End-Use Industry

- Food Processing Industry

- Sports & Functional Nutrition

- Plant-Based Dairy Industry

- Clinical & Medical Nutrition

- Pet Food Industryx

Regional Insights

North America

North America holds the largest share of the global pea protein powder market, accounting for approximately 34% of total demand. The United States leads regional consumption due to strong innovation in plant-based foods, advanced food processing infrastructure, and high consumer awareness regarding sustainable nutrition. Canada plays a pivotal role as a major producer of yellow peas, ensuring reliable raw material supply and strengthening regional supply chain integration. Regional growth is further driven by increasing investment in alternative protein startups, strong venture capital activity, expanding vegan and flexitarian populations, and widespread adoption of protein-fortified functional foods. Favorable regulatory support for plant-based labeling, continuous product launches by major food brands, and rising demand for allergen-free protein ingredients continue to reinforce North America’s leadership position.

Europe

Europe represents nearly 29% of global demand, led by Germany, the United Kingdom, France, and the Netherlands. Regional growth is strongly supported by stringent sustainability regulations, carbon reduction initiatives, and widespread consumer adoption of vegan and vegetarian lifestyles. European food manufacturers are actively reformulating products to comply with clean-label standards and environmental targets, significantly increasing demand for plant-derived proteins such as pea protein. Government-backed sustainability programs, growing investment in alternative protein research, and expanding private-label plant-based product portfolios are further accelerating adoption. Additionally, rising consumer preference for locally sourced and non-GMO ingredients continues to strengthen market expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, driven by China, India, Japan, and Australia. Rapid urbanization, rising disposable income, and expanding middle-class populations are increasing demand for affordable and nutritious protein sources. Growing awareness of plant-based diets, combined with rising lactose intolerance rates across Asian populations, is encouraging adoption of plant-derived proteins. China is investing heavily in domestic protein processing capacity and alternative protein innovation to reduce reliance on imports, while India is witnessing growing demand for cost-effective plant proteins aligned with vegetarian dietary patterns. Expansion of modern retail channels, increasing penetration of e-commerce platforms, and government initiatives promoting food security and sustainable agriculture further support regional growth momentum.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico, supported by expanding food processing industries and increasing consumer awareness of health and wellness nutrition. Rising urbanization and growing middle-income populations are driving demand for functional foods and protein-enriched products. Regional manufacturers are gradually integrating plant-based ingredients into traditional food categories, while international brands are expanding distribution networks to capture emerging opportunities. Improvements in retail infrastructure, growing fitness culture, and increasing exposure to global dietary trends are contributing to gradual but consistent market expansion across the region.

Middle East & Africa

The Middle East and Africa region is gradually expanding, with growth led by the United Arab Emirates and South Africa. Increasing demand for premium imported health foods, rising wellness awareness, and expanding expatriate populations are supporting adoption of plant-based protein products. Regional growth is further driven by the expansion of modern retail formats, e-commerce penetration, and growing investments in food diversification strategies aimed at reducing dependence on animal protein imports. Increasing focus on lifestyle-related health management and demand for functional nutrition products among younger consumer demographics are expected to support sustained market development in the coming years.

Key Players in the Pea Protein Powder Market

- Roquette Frères

- Ingredion Incorporated

- Cargill Incorporated

- Puris Holdings

- Cosucra Groupe Warcoing

- Burcon NutraScience Corporation

- Axiom Foods Inc.

- Nutri-Pea Limited

- Shandong Jianyuan Group

- Emsland Group

- Sotexpro SA

- Kerry Group plc

- ADM (Archer Daniels Midland Company)

- Glanbia plc

- Fenchem Biotek Ltd.