Pea Processed Ingredient Market Size

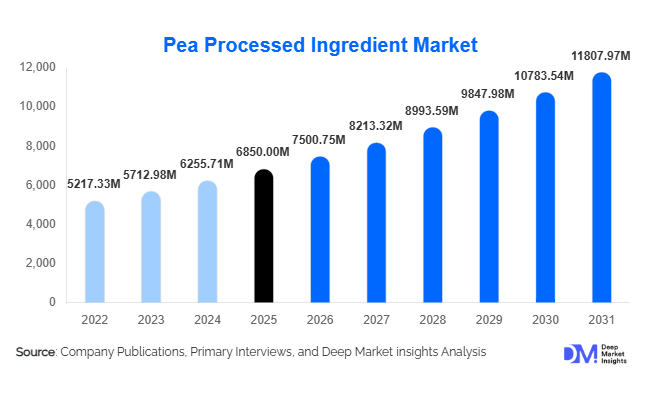

According to Deep Market Insights, the global pea processed ingredient market size was valued at USD 6,850 million in 2025 and is projected to grow from USD 7,500.75 million in 2026 to reach USD 11,807.97 million by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The market growth is primarily driven by accelerating demand for plant-based proteins, expanding applications in meat and dairy alternatives, and increasing adoption of clean-label, allergen-free ingredients across the food, beverage, and nutrition industries.

Key Market Insights

- Pea protein ingredients account for nearly 48% of the total market value, led by high-purity isolates used in plant-based meat and sports nutrition.

- Food & beverage applications dominate with approximately 62% share, supported by rapid growth in vegan and flexitarian product launches.

- North America leads with around 35% of global demand, driven by strong plant-based food penetration and advanced processing infrastructure.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR due to rising middle-class protein consumption and food processing investments.

- Wet fractionation technology holds about 55% share, enabling high-protein isolate production for premium food applications.

- Top five players control roughly 42% of global revenue, reflecting moderate consolidation and ongoing capacity expansion.

What are the latest trends in the pea processed ingredient market?

Shift Toward High-Purity and Functional Protein Isolates

Manufacturers are increasingly focusing on high-protein isolates exceeding 80–85% protein concentration, particularly for meat analogues, RTD beverages, and sports nutrition powders. Functional improvements such as enhanced emulsification, gelation, and solubility are making pea protein competitive with soy and whey. Companies are also investing in flavor-neutralization technologies to reduce earthy notes, thereby expanding beverage applications. Textured pea protein (TPP) is gaining momentum due to its ability to replicate meat-like fibers through high-moisture extrusion.

Sustainable Processing and Dry Fractionation Expansion

Dry fractionation technology is emerging as a sustainable alternative to traditional wet extraction. This process reduces water usage and lowers energy consumption, aligning with global sustainability targets. Food brands are increasingly marketing pea-based ingredients as environmentally responsible due to lower carbon and water footprints compared to animal protein. Integration of regenerative agriculture practices and traceability platforms is also strengthening supply chain transparency.

What are the key drivers in the pea processed ingredient market?

Growth of Plant-Based Meat and Dairy Alternatives

The global plant-based meat and dairy industries continue to expand at double-digit rates, significantly driving demand for pea protein isolates and textured protein. Pea ingredients offer non-GMO, gluten-free, and soy-free positioning, making them suitable for allergen-sensitive consumers. Large multinational food companies are increasingly incorporating pea protein into mainstream packaged foods, accelerating volume demand.

Rising Sports Nutrition and Functional Beverage Consumption

The sports nutrition industry is witnessing strong growth, particularly among flexitarian and vegan consumers seeking plant-based protein powders. Pea protein’s high lysine content and digestibility make it attractive for performance and recovery formulations. Functional beverages fortified with plant protein are also expanding, especially in North America and Europe.

What are the restraints for the global market?

Raw Material Price Volatility

Yellow pea production is concentrated in Canada, Russia, and parts of Europe. Weather-related crop variability impacts pricing stability and processing margins. Fluctuating raw material costs can affect contract pricing and profitability for ingredient manufacturers.

Sensory and Functional Challenges

Despite technological advancements, pea protein can impart off-flavors in certain beverage applications. Additional flavor masking and formulation adjustments increase production costs, limiting adoption in highly sensitive product categories.

What are the key opportunities in the pea processed ingredient industry?

Expansion in Emerging Asian Markets

Asia-Pacific presents a significant opportunity due to expanding middle-class populations and increasing protein intake. China and India are investing in domestic food processing infrastructure to reduce reliance on soy imports. Local production partnerships and capacity expansion can unlock high-growth regional demand.

Government-Backed Alternative Protein Initiatives

Governments across Europe and North America are supporting plant-based protein development through innovation grants and sustainability incentives. Pea protein aligns strongly with carbon reduction goals, offering companies access to green financing and public procurement programs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6850 Million |

| Market Size in 2026 | USD 7500.75 Million |

| Market Size in 2031 | USD 11807.97 Million |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pea protein ingredients dominate the global market with 48% share in 2025, making them the largest revenue-generating segment. This leadership is primarily driven by the rapid expansion of plant-based meat and dairy alternatives, where high-purity pea protein isolates (80–85% protein content) are preferred for their emulsification, gelation, and water-binding properties. The segment is also benefiting from growing demand in sports nutrition, ready-to-drink (RTD) protein beverages, and fortified snack products. Continuous improvements in flavor masking technologies and high-moisture extrusion capabilities are further accelerating isolate adoption across mainstream food categories.

Pea starch accounts for approximately 22% of total market value, supported by rising demand for clean-label thickening and binding agents in soups, sauces, noodles, and gluten-free bakery products. Its non-GMO positioning and neutral taste profile make it a competitive alternative to modified corn starch. Pea fiber represents nearly 12% of the market, gaining traction due to digestive health awareness and its ability to improve texture and moisture retention in processed foods. Pea flour contributes about 10%, particularly in snacks, extruded products, and bakery formulations where protein fortification and allergen-free positioning are required. Other pea derivatives collectively account for the remaining share, primarily serving niche industrial and specialty food applications.

Application Insights

The food & beverages segment leads with approximately 62% market share, driven by the structural growth of plant-based meat, dairy alternatives, protein-enriched beverages, and gluten-free packaged foods. The surge in flexitarian diets and clean-label product reformulation initiatives by multinational food brands has significantly boosted pea ingredient incorporation rates. Textured pea protein is increasingly used in burgers, sausages, and hybrid meat products, while isolates are expanding into protein bars and dairy-free yogurts.

Animal feed accounts for nearly 16% of total demand, as pea protein is used as a partial replacement for soybean meal due to price competitiveness and lower allergen risk. Nutraceuticals and dietary supplements contribute around 12%, and this segment is among the fastest-growing due to the rising adoption of vegan protein powders and functional health blends. Pet food applications represent approximately 8% share, supported by premiumization trends and increasing demand for hypoallergenic, plant-forward pet diets. Industrial applications such as biodegradable plastics, adhesives, and bio-based packaging remain relatively small but are projected to grow steadily as sustainability regulations intensify globally.

Distribution Channel Insights

Direct B2B contracts dominate the market with nearly 70% of global sales, reflecting the large-volume procurement patterns of multinational food processors and plant-based product manufacturers. Long-term supply agreements help stabilize pricing amid raw material volatility and ensure quality consistency. Ingredient distributors hold approximately 25% share, serving small and mid-sized food companies that require flexible volumes and technical formulation support. Online ingredient platforms and digital B2B marketplaces remain emerging channels, currently accounting for a limited share but expected to expand gradually as procurement digitization accelerates across the food manufacturing sector.

End-Use Industry Insights

The food processing industry remains the largest consumer of pea processed ingredients, valued at over USD 4,000 million in 2025 and expanding at approximately 9% CAGR. Growth is largely attributed to product reformulation initiatives aimed at reducing animal protein dependency and meeting clean-label consumer expectations. The animal nutrition industry contributes nearly USD 1,100 million, supported by diversification away from soy-based feed inputs and growing aquaculture feed demand.

The nutraceutical and dietary supplement industry is among the fastest-growing end-use segments, expanding at over 10% CAGR, driven by rising consumer focus on plant-based protein supplementation and digestive health. Pet food demand continues to rise steadily due to premiumization, functional nutrition, and allergen-sensitive formulations. Additionally, industrial manufacturing sectors exploring biodegradable materials and bio-based polymers are creating incremental demand streams that may significantly contribute to long-term market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Pea Processed Ingredient Market Segmentations

By Product Type

- Pea Protein Ingredients

- Pea Starch

- Pea Fiber

- Pea Flour

- Other Pea-Derived Ingredients

By Application

- Food & Beverages

- Animal Feed

- Nutraceuticals & Dietary Supplements

- Pet Food

- Industrial Applications

By Distribution Channel

- Direct B2B Contracts

- Ingredient Distributors

- Online B2B Platforms

By End-Use Industry

- Food Processing Industry

- Animal Nutrition Industry

- Pharmaceutical & Nutraceutical Industry

- Pet Food Industry

- Industrial Manufacturing

Regional Insights

North America

North America holds approximately 35% of the global market share in 2025, making it the leading region. The United States drives the majority of demand due to its well-established plant-based food industry, strong venture capital funding in alternative proteins, and high consumer adoption of vegan and flexitarian diets. Canada plays a dual role as both a major yellow pea producer and a processing hub, benefiting from advanced fractionation infrastructure and export-oriented production. Government-backed protein innovation clusters and investments in alternative protein R&D are further strengthening regional growth.

Europe

Europe accounts for around 28% share of global revenue, led by Germany, France, the United Kingdom, and the Netherlands. Regional growth is strongly driven by stringent sustainability regulations, carbon reduction targets, and high consumer awareness regarding plant-based nutrition. The European Union’s Farm-to-Fork strategy and protein diversification initiatives are encouraging domestic pulse processing. Additionally, widespread demand for clean-label and allergen-free bakery products supports consistent uptake of pea starch and fiber ingredients.

Asia-Pacific

Asia-Pacific represents nearly 25% of global demand and is the fastest-growing region, expanding at over 11% CAGR. China and India are leading the growth due to expanding food processing capacity, rising disposable incomes, and increasing protein consumption. China is also investing in domestic plant protein processing to reduce soybean import dependence. Japan and Australia maintain steady demand in health-focused and functional food applications. Rapid urbanization, evolving dietary habits, and government incentives for food manufacturing modernization are key drivers of regional expansion.

Latin America

Latin America contributes approximately 7% of global revenue, with Brazil and Argentina emerging as both cultivation and consumption centers. Regional growth is supported by agricultural diversification initiatives and the gradual expansion of plant-based food offerings. Increasing export orientation and improving food processing infrastructure are expected to strengthen long-term demand.

Middle East & Africa

The Middle East & Africa region holds nearly 5% market share, led by the UAE and South Africa. Growth is primarily driven by rising health awareness, increasing imports of plant-based packaged foods, and expanding retail distribution networks. High-income consumers in the Gulf Cooperation Council (GCC) countries are contributing to demand for premium plant-based products. In Africa, gradual modernization of food processing sectors and growing urban populations are creating incremental opportunities for pea-based ingredients.

Key Players in the Pea Processed Ingredient Market

- Roquette Frères

- Ingredion Incorporated

- Cargill

- Cosucra Groupe Warcoing

- Emsland Group

- AGT Food and Ingredients

- Vestkorn Milling

- The Scoular Company

- Yantai Shuangta Food

- Axiom Foods

- Burcon NutraScience

- Shandong Jianyuan Group

- Meelunie

- Puris

- Puratos Group