Paper Packaging Market Size

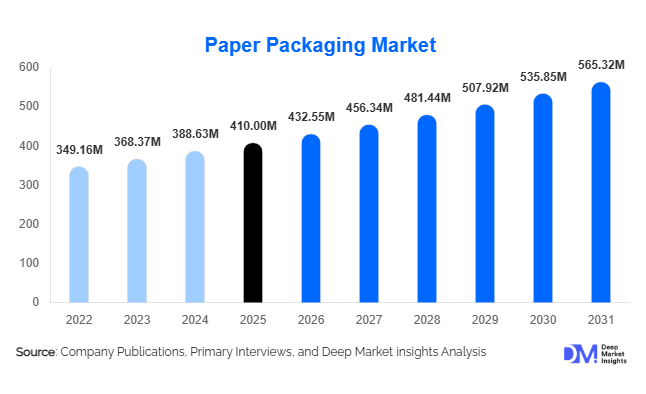

According to Deep Market Insights, the global paper packaging market size was valued at USD 410 million in 2026 and is projected to grow from USD 432.55 million in 2027 to reach USD 565.32million by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The paper packaging market growth is primarily driven by the accelerating shift toward sustainable and recyclable packaging solutions, rapid expansion of e-commerce logistics, and increasing regulatory restrictions on single-use plastics across major economies worldwide.

Key Market Insights

- Paper packaging is rapidly replacing plastic-based packaging across FMCG, retail, and food delivery sectors due to global sustainability mandates and circular economy initiatives.

- Corrugated packaging dominates global usage, supported by exponential growth in e-commerce shipments and global supply chain expansion.

- Asia-Pacific leads global production and consumption, driven by strong manufacturing bases in China and India and rising domestic demand.

- Recycled paper materials are gaining strong traction due to cost efficiency and increasing corporate ESG commitments.

- Food & beverage remains the largest end-use segment, driven by rising demand for packaged, processed, and ready-to-eat food products.

- Technological advancements in coated and barrier paper are expanding applications into moisture-sensitive and premium packaging categories.

What are the latest trends in the paper packaging market?

Shift Toward Sustainable and Plastic-Free Packaging

One of the most defining trends in the global paper packaging market is the rapid transition toward plastic-free and biodegradable packaging solutions. Governments across Europe, North America, and Asia-Pacific are implementing strict bans and taxation policies on single-use plastics, significantly boosting demand for paper-based alternatives. Companies are increasingly adopting recyclable corrugated boards, molded fiber packaging, and compostable cartons to meet regulatory requirements and sustainability commitments. This shift is also being reinforced by consumer preference for eco-friendly packaging, particularly in urban retail and e-commerce sectors.

Innovation in Barrier and Functional Paper Packaging

Advancements in material science are enabling paper packaging to compete with plastics in high-performance applications. Innovations such as water-resistant coatings, grease-proof layers, and bio-based barrier technologies are expanding the usability of paper packaging in food delivery, frozen foods, and pharmaceutical packaging. Digital printing and smart labeling technologies are also transforming paper packaging into a branding and communication tool, enabling QR integration, traceability, and anti-counterfeit features.

What are the key drivers in the paper packaging market?

Rapid Growth of E-Commerce and Logistics

The exponential rise of global e-commerce is a major driver of paper packaging demand. Online retail platforms require durable, lightweight, and cost-efficient packaging solutions, particularly corrugated boxes and mailer cartons. The surge in cross-border trade and last-mile delivery networks is further accelerating consumption. E-commerce packaging alone accounts for a significant portion of incremental demand, especially in emerging economies like India, Southeast Asia, and Latin America.

Global Sustainability Regulations and ESG Adoption

Stringent environmental regulations are pushing industries to adopt recyclable and sustainable packaging solutions. Extended Producer Responsibility (EPR) frameworks, plastic bans, and carbon reduction targets are driving companies toward paper-based packaging. Corporations are also integrating ESG goals into supply chain strategies, increasing demand for recycled fiber packaging and sustainable sourcing practices across industries.

Expansion of FMCG and Processed Food Industry

The global growth of the FMCG and packaged food industry is significantly contributing to paper packaging demand. Urbanization, rising disposable incomes, and changing dietary habits are increasing consumption of packaged food products. Paper cartons, folding boxes, and food-grade packaging solutions are widely used across this sector, reinforcing long-term demand stability.

What are the restraints for the global market?

Volatility in Raw Material Prices

The paper packaging industry is highly dependent on pulp, recycled fiber, and energy inputs, making it vulnerable to price fluctuations. Supply chain disruptions, forestry limitations, and transportation costs directly impact production margins. This volatility creates pricing instability for manufacturers and end users, particularly in low-margin packaging segments.

Performance Limitations Compared to Plastic Packaging

Despite technological advancements, paper packaging still faces limitations in moisture resistance, durability, and long-term preservation compared to plastic alternatives. This restricts its adoption in certain applications such as chemical packaging, liquid-heavy products, and extended shelf-life food items, limiting full substitution potential in some industries.

What are the key opportunities in the paper packaging industry?

Expansion of Sustainable Packaging Innovation

There is a major opportunity in developing advanced sustainable packaging solutions such as fully compostable coatings, biodegradable laminates, and high-strength recycled fiber materials. Companies investing in R&D for next-generation paper packaging technologies are expected to gain competitive advantage in premium and regulated markets.

Growth in Emerging E-Commerce Markets

Rapid digitalization in emerging economies presents a significant opportunity for paper packaging manufacturers. Countries such as India, Brazil, Indonesia, and Vietnam are witnessing strong growth in online retail penetration, creating demand for corrugated boxes, protective packaging, and customized shipping solutions.

Smart and Functional Packaging Integration

The integration of smart technologies such as QR codes, NFC tags, and track-and-trace systems into paper packaging is creating new value-added applications. These innovations are especially relevant in pharmaceuticals, luxury goods, and food supply chains, enhancing product authenticity and consumer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 410 Million |

| Market Size in 2026 | USD 432.55 Million |

| Market Size in 2031 | USD 565.32 Million |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global paper packaging market continues to be significantly shaped by the dominance of corrugated packaging, which accounts for an estimated 42% share in 2025. This leadership position is primarily driven by the rapid expansion of global e-commerce ecosystems, increasing cross-border trade, and the growing need for durable, lightweight, and cost-efficient packaging solutions. Corrugated packaging is extensively used across logistics and transportation due to its high strength-to-weight ratio, cushioning properties, and adaptability to automated packaging systems. In addition, rising sustainability commitments among corporations are accelerating the replacement of plastic-based packaging with recyclable corrugated alternatives. The segment is further supported by technological advancements in digital printing, which enable high-quality branding and customization, making corrugated packaging not only functional but also a marketing tool for brands.Specialty paper packaging, which includes molded fiber packaging, coated papers, and high-performance paper-based solutions, represents approximately 15% of the market. This segment is experiencing the fastest growth among product types due to rising demand for premium, eco-friendly, and innovative packaging formats. The key driver behind this growth is the increasing consumer preference for sustainable packaging alternatives that minimize environmental impact while maintaining product protection. Molded fiber packaging, in particular, is gaining traction in electronics, cosmetics, and food delivery applications as companies transition away from single-use plastics. Technological advancements in pulp molding and coating processes are further enhancing product performance and expanding application scope.Flexible paper packaging accounts for the remaining share of the market and is widely used in lightweight applications such as snacks, confectionery, bakery products, and personal care items. The growth of this segment is driven by increasing demand for convenience packaging and portability, especially in urban markets. Rising health consciousness and on-the-go consumption patterns are encouraging manufacturers to adopt flexible, portion-controlled packaging formats. Additionally, innovations in grease-resistant and moisture-resistant paper materials are expanding the usability of flexible paper packaging in more demanding applications.

Application Insights

The food and beverage industry remains the largest application segment, accounting for nearly 38% of total paper packaging consumption. This dominance is driven by the global expansion of packaged food consumption, rising urbanization, and the rapid growth of food delivery and takeaway services. The increasing preference for hygienic, safe, and sustainable packaging is also reinforcing demand across this sector. Quick-service restaurants and online food delivery platforms are major contributors, as they require large volumes of disposable yet eco-friendly packaging solutions. Additionally, governments across various regions are implementing bans on single-use plastics in food applications, further strengthening the shift toward paper-based packaging.Industrial packaging accounts for around 18% of the market and is driven by manufacturing, automotive, and export-oriented industries. The key growth factor in this segment is the need for durable and protective packaging for heavy or bulk goods. Global supply chain expansion and increasing international trade are further supporting demand. Additionally, industries are increasingly adopting recyclable packaging solutions to meet corporate sustainability goals and regulatory compliance requirements.Healthcare and pharmaceutical packaging represents approximately 9% of the market, driven by stringent regulatory standards, increasing healthcare expenditure, and rising demand for safe and tamper-evident packaging. The COVID-19 pandemic further accelerated the adoption of paper-based pharmaceutical packaging due to heightened hygiene awareness. Personal care and other niche applications continue to grow steadily as brands transition toward environmentally responsible packaging formats and respond to evolving consumer expectations.

Distribution Channel Insights

Business-to-business (B2B) direct sales dominate the global paper packaging market, primarily due to long-term contractual relationships between packaging manufacturers and large-scale end-use industries such as FMCG, e-commerce, and industrial manufacturing. These contracts ensure consistent demand, pricing stability, and customized packaging solutions tailored to specific client requirements. The primary driver of this channel is operational efficiency and economies of scale, which benefit both suppliers and buyers.Online procurement platforms are emerging as a rapidly growing distribution channel, particularly among small and medium-sized enterprises. The growth of this channel is driven by digitalization, increased price transparency, and the ability to compare multiple suppliers efficiently. These platforms also enable faster procurement cycles and improved supply chain flexibility.Packaging distributors and wholesalers continue to play a critical role in regional supply chains, especially in developing economies where direct manufacturer access is limited. Their growth is supported by fragmented demand patterns and the need for localized inventory distribution. Additionally, direct-to-consumer and customized packaging services are gaining momentum, driven by the rise of D2C brands that require flexible, small-batch, and branded packaging solutions.

End-Use Insights

The FMCG industry remains the dominant end-use segment due to its consistent demand for high-volume packaging solutions across food, beverages, personal care, and household products. The primary driver for this segment is continuous product consumption and frequent replenishment cycles, which ensure steady packaging demand.E-commerce is the fastest-growing end-use segment, fueled by global digital transformation and changing consumer shopping behavior. The rise of mobile commerce, subscription services, and cross-border online retail is significantly increasing packaging requirements. Food processing industries also contribute substantial demand, supported by the growing consumption of packaged and processed food products worldwide.Pharmaceutical packaging continues to expand due to strict compliance requirements, increasing global healthcare access, and the growing need for safe drug distribution systems. Industrial manufacturing remains a stable contributor, while emerging applications in luxury goods, electronics, and sustainable industrial packaging are opening new growth avenues.

Explore more data points, trends and opportunities Download Free Sample Report

Paper Packaging Market Segmentations

By Product Type

- Corrugated Packaging

- Folding Cartons

- Flexible Paper Packaging

- Molded Fiber Packaging

- Coated & Specialty Paper Packaging

By Material Type

- Virgin Paper & Pulp

- Recycled Paper Fiber

- Kraft Paper

- Specialty Paper Grades

By Packaging Format

- Boxes & Cartons

- Wraps & Sleeves

- Bags & Sacks

- Trays & Containers

- Protective Packaging Materials

By Application

- Food & Beverage Packaging

- E-commerce & Retail Packaging

- Industrial Packaging

- Healthcare & Pharmaceutical Packaging

- Personal Care & Cosmetics Packaging

By Distribution Channel

- B2B Direct Sales

- Packaging Distributors & Wholesalers

- Online Procurement Platforms

- Direct-to-Brand Supply Contracts

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global paper packaging market with approximately 45% market share in 2025. The region’s leadership is driven by rapid industrialization, large-scale manufacturing activity, and strong export-oriented economies. China remains the largest contributor due to its extensive packaging manufacturing ecosystem and dominance in global supply chains. India represents the fastest-growing market, fueled by expanding e-commerce penetration, rising disposable incomes, and strong government initiatives promoting sustainable packaging practices. Japan and South Korea contribute significantly through advanced packaging technologies, high-quality production standards, and strong demand from electronics and premium consumer goods industries. The key growth drivers in Asia-Pacific include urbanization, rising consumer consumption, digital retail expansion, and increasing adoption of eco-friendly packaging solutions across industries.

North America

North America holds around 25% market share, with the United States leading regional demand. The primary growth driver in this region is the well-established e-commerce ecosystem, which continues to expand rapidly and requires high volumes of corrugated and protective packaging. Strong FMCG and retail industries further support demand for paper packaging solutions. Canada contributes steadily, supported by advanced recycling infrastructure and strong environmental policies that encourage sustainable packaging adoption. The region is characterized by high innovation levels, with companies investing in smart packaging technologies, lightweight materials, and fully recyclable packaging systems. Increasing consumer awareness regarding environmental sustainability is also accelerating the shift away from plastic packaging toward paper-based alternatives.

Europe

Europe accounts for nearly 22% market share, driven by strict environmental regulations and strong circular economy policies. Germany, the United Kingdom, and France are the leading markets within the region. The key driver of growth is regulatory enforcement aimed at reducing carbon emissions and plastic waste, which is pushing industries toward recyclable and biodegradable packaging solutions. High consumer awareness and demand for sustainable products further reinforce market expansion. Additionally, Europe is witnessing strong innovation in fiber-based packaging technologies, including advanced molded fiber and compostable packaging materials. The region’s mature retail and e-commerce sectors also contribute to steady demand for paper packaging solutions.

Latin America

Latin America is an emerging market led by Brazil and Mexico, where growth is primarily driven by retail sector expansion and increasing industrialization. The key driver in this region is rising consumer demand for packaged food and beverages, supported by urban population growth and improving economic conditions. Additionally, export-oriented industries are increasingly adopting paper packaging to comply with international sustainability standards. The region is also witnessing gradual adoption of environmentally friendly packaging practices, although infrastructure limitations remain a challenge. Nevertheless, growing foreign investment and modernization of supply chains are expected to strengthen market growth over the forecast period.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, led by the UAE, Saudi Arabia, and South Africa. The primary growth driver is the expansion of logistics infrastructure and retail sectors, supported by economic diversification initiatives in Gulf countries. Increasing import of packaged goods and rising tourism activity are also contributing to packaging demand. In Africa, industrialization and intra-regional trade are gradually increasing, creating new opportunities for paper packaging adoption. The region is also beginning to see a shift toward sustainable packaging solutions, driven by global supply chain requirements and environmental awareness initiatives. Despite infrastructural challenges, long-term growth potential remains strong due to ongoing urbanization and economic development.

Key Players in the Global Paper Packaging Market

- International Paper

- Smurfit WestRock

- Mondi Group

- Stora Enso

- Packaging Corporation of America

- Oji Holdings

- Nippon Paper Industries

- Nine Dragons Paper

- Sappi Limited

- Georgia-Pacific

- Huhtamaki

- Mayr-Melnhof Karton

- Klabin S.A.

- Lee & Man Paper Manufacturing

- UPM-Kymmene Corporation