Packaging Testing Market Size

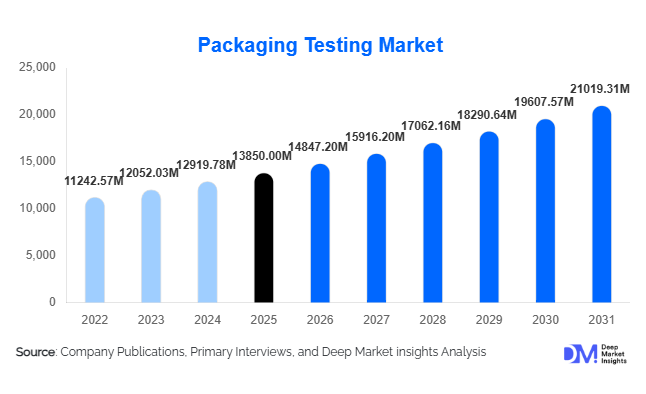

According to Deep Market Insights, the global packaging testing market size was valued at USD 13,850 million in 2025 and is projected to grow from USD 14,847.20 million in 2026 to reach USD 21,019.31 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The packaging testing market growth is primarily driven by increasing regulatory scrutiny in food and pharmaceutical packaging, rapid expansion of global e-commerce logistics, and rising demand for sustainable and recyclable packaging materials. As global trade volumes increase and product supply chains become more complex, manufacturers are prioritizing packaging validation to minimize product recalls, prevent transit damage, and ensure compliance with international safety standards.

Key Market Insights

- Food & beverage packaging accounts for the largest share of testing demand, supported by stringent food safety and migration regulations.

- Third-party testing laboratories dominate the market, capturing nearly 57% of total revenue due to regulatory credibility and specialized infrastructure.

- Asia-Pacific leads the global market, driven by pharmaceutical exports and manufacturing growth in China and India.

- Physical testing remains the largest test type, supported by rising e-commerce parcel shipments and transit simulation requirements.

- Sustainability-focused testing services, including recyclability validation and barrier performance analysis, are emerging as premium offerings.

- Digitalization and automation in laboratories, including AI-enabled analytics and IoT-based stress testing systems, are enhancing operational efficiency.

What are the latest trends in the packaging testing market?

Sustainability and Circular Packaging Validation

Packaging manufacturers are increasingly shifting toward biodegradable, recyclable, and lightweight materials to meet global sustainability mandates. This shift has intensified demand for recyclability testing, compostability validation, and life-cycle performance analysis. Extended Producer Responsibility (EPR) regulations across Europe and North America are compelling brands to validate material recovery efficiency and environmental compliance. Testing laboratories are expanding capabilities in barrier property testing for mono-material plastics and fiber-based alternatives, ensuring that sustainable materials maintain product safety and shelf life.

Automation and Smart Testing Technologies

Advanced permeability analyzers, robotic compression testing systems, and AI-powered defect detection tools are transforming laboratory operations. Automated data capture and predictive analytics improve test accuracy and reduce turnaround times. IoT-enabled sensors embedded in packaging during transit simulations are increasingly used to collect real-time performance data. These innovations are helping laboratories manage rising test volumes while maintaining high precision standards, particularly for pharmaceutical stability and sterile packaging validation.

What are the key drivers in the packaging testing market?

Stringent Regulatory Compliance in Food and Pharmaceuticals

Global food safety authorities and pharmaceutical regulators mandate rigorous packaging validation to prevent contamination, migration, and product degradation. Migration limits for food-contact materials and sterility testing for injectable drugs are expanding the scope of mandatory laboratory services. Pharmaceutical exports from India, China, Germany, and the U.S. further amplify cross-border compliance requirements.

Expansion of E-commerce and Global Trade

Rising cross-border parcel shipments have increased demand for drop, compression, and vibration testing. Online retail growth above 9% annually has driven packaging optimization to reduce product returns and damage-related losses. Transit simulation and durability testing are now integral components of packaging development cycles.

What are the restraints for the global market?

High Capital Investment Requirements

Advanced barrier testing systems, microbiological laboratories, and automated environmental chambers require substantial capital expenditure. Smaller laboratories face financial constraints in upgrading infrastructure to meet international standards.

Fragmented Regulatory Frameworks

Variations in packaging standards across regions increase compliance complexity. Divergent testing protocols between North America, Europe, and Asia add operational costs for global manufacturers and service providers.

What are the key opportunities in the packaging testing industry?

Pharmaceutical Export Growth in Emerging Markets

India and China are rapidly expanding pharmaceutical exports to regulated markets. This trend creates high-margin opportunities for accredited third-party laboratories specializing in sterility, stability, and migration testing. Investments in GLP-certified laboratories in emerging economies are expected to accelerate.

E-commerce Transit Simulation Services

With global parcel volumes rising sharply, demand for transit simulation and vibration testing is expanding. Packaging testing providers integrating IoT-based monitoring and predictive failure analysis can secure long-term contracts with major retail and logistics firms.

Test Type Insights

Physical testing accounts for approximately 34% of the global packaging testing market in 2025, making it the largest and most established segment. The dominance of physical testing is primarily driven by the rapid expansion of global e-commerce, cross-border trade, and industrial manufacturing. Compression strength, drop, vibration, and burst testing are universally mandated across supply chains to ensure packaging integrity during transportation and warehousing. With parcel shipment volumes increasing annually and return-related losses impacting retailer profitability, transit simulation testing has become a standard requirement for consumer goods, electronics, and industrial products. Additionally, international logistics standards and retailer compliance programs further reinforce the need for consistent mechanical performance validation.

Barrier and permeability testing represents the second-largest segment, driven by oxygen and moisture sensitivity requirements in food, beverages, and pharmaceuticals. As manufacturers increasingly adopt lightweight and sustainable materials, maintaining product shelf life has become critical, boosting demand for oxygen transmission rate (OTR) and water vapor transmission rate (WVTR) testing. Microbiological and shelf-life testing are the fastest-growing sub-segments, supported by stricter regulatory controls in pharmaceutical sterile packaging and processed food preservation. The growing biologics and injectable drug market is further accelerating demand for stability and sterility validation services globally.

Material Insights

Plastic packaging dominates with nearly 41% market share in 2025, reflecting its widespread use in flexible pouches, rigid containers, pharmaceutical blister packs, and protective films. The leading position of plastics is driven by their versatility, lightweight properties, and cost efficiency, which make them integral to food preservation and healthcare packaging. However, the transition toward recyclable and mono-material plastics has intensified demand for advanced barrier and migration testing to ensure compliance with food-contact safety standards and environmental regulations.

Paper & paperboard testing is expanding steadily due to global sustainability initiatives and bans on single-use plastics in several regions. Corrugated box performance testing is particularly benefiting from e-commerce growth. Metal and glass packaging testing remains stable, supported by beverage, aerosol, and specialty pharmaceutical applications where durability and chemical resistance are critical. The increasing focus on sustainable alternatives is reshaping testing requirements across all material categories.

End-Use Industry Insights

Food & beverages lead the packaging testing market, contributing around 38% of total revenue in 2025. The segment’s leadership is driven by stringent food safety regulations, migration limits for food-contact materials, and the need for extended shelf life in global trade. Rising consumption of processed foods and ready-to-eat products further fuels testing demand.

Pharmaceuticals represent the fastest-growing segment, expanding at above 8% CAGR, supported by global drug exports, biologics packaging requirements, and increased vaccine production. Strict sterility and stability protocols, especially for injectable and temperature-sensitive drugs, require advanced microbiological and barrier validation services. Cosmetics and personal care are emerging as high-value segments due to premium packaging formats and regulatory requirements related to chemical compatibility and consumer safety.

| By Test Type | By Material Type | By End-Use Industry | By Service Provider |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 36% of the global market in 2025, making it the largest regional contributor. China holds nearly 14% of global demand, supported by its dominant manufacturing base and export-driven packaging industry. India contributes about 8%, with strong growth in pharmaceutical exports and food processing. Key drivers for regional growth include rapid industrialization, expanding middle-class consumption, increasing foreign direct investment in manufacturing, and government-backed quality infrastructure initiatives. India remains the fastest-growing market in the region, expanding above 9% CAGR, driven by regulatory harmonization with U.S. and European standards and growth in biologics production.

North America

North America holds around 28% market share, with the United States contributing nearly 22% globally. Growth in this region is driven by strict regulatory enforcement by food and pharmaceutical authorities, high adoption of advanced laboratory automation, and strong e-commerce penetration. The U.S. pharmaceutical sector, valued at over USD 600 billion, significantly boosts sterility and stability testing demand. Additionally, sustainability-focused packaging regulations and corporate ESG commitments are increasing recyclability and migration testing volumes.

Europe

Europe represents approximately 24% of the global market, led by Germany, France, and the United Kingdom. The region’s growth is strongly influenced by stringent environmental regulations under circular economy policies and Extended Producer Responsibility (EPR) frameworks. High consumer awareness regarding sustainable packaging drives demand for recyclability validation and eco-compliance testing. Europe also benefits from advanced laboratory infrastructure and strong cross-border trade within the EU, necessitating harmonized packaging standards.

Latin America

Latin America accounts for nearly 7% of the global market, with Brazil and Mexico leading regional demand. Growth drivers include rising processed food exports, expansion of pharmaceutical manufacturing capabilities, and modernization of regulatory frameworks. Increasing foreign investment in manufacturing and the expansion of regional trade agreements are supporting greater adoption of packaging validation services.

Middle East & Africa

The Middle East & Africa contribute around 5% of the global market. The United Arab Emirates and Saudi Arabia are key growth hubs, driven by increasing food imports, expanding pharmaceutical distribution networks, and regulatory modernization initiatives. Infrastructure investments in logistics and warehousing are supporting transit testing demand. In Africa, South Africa leads regional adoption, supported by its established food and beverage industry and growing export compliance requirements.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Packaging Testing Market

- SGS SA

- Bureau Veritas

- Intertek Group plc

- Eurofins Scientific

- TÜV SÜD

- TÜV Rheinland

- UL Solutions

- Element Materials Technology

- Mérieux NutriSciences

- ALS Limited

- Smithers

- West Pharmaceutical Services

- Amcor plc

- Sealed Air Corporation