Packaged Coconut Water Market Size

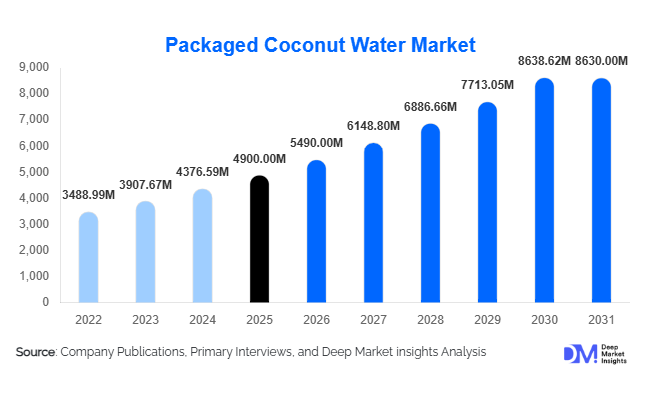

According to Deep Market Insights, the global packaged coconut water market size was valued at USD 4,900 million in 2025 and is projected to grow from USD 5,490 million in 2026 to reach USD 8,630 million by 2031, expanding at a CAGR of 12.0% during the forecast period (2026–2031). The market growth is primarily driven by rising global health consciousness, increasing demand for natural hydration beverages, rapid expansion of functional drinks, and growing penetration of premium organic beverage categories across developed and emerging economies.

Key Market Insights

- 100% pure coconut water dominates demand, supported by clean-label trends and consumer preference for minimally processed natural beverages.

- Supermarkets and hypermarkets remain the leading distribution channel, driven by strong brand visibility and impulse purchasing behavior.

- North America leads consumption, supported by high demand for premium and functional beverages in the U.S. and Canada.

- Asia-Pacific is the fastest-growing region, driven by strong production base, rising urban consumption, and expanding retail penetration.

- E-commerce channels are rapidly expanding, accounting for an increasing share of premium and niche coconut water sales globally.

- Sports and fitness applications are accelerating demand, as coconut water becomes a preferred natural electrolyte alternative.

What are the latest trends in the packaged coconut water market?

Premiumization and Organic Product Expansion

The packaged coconut water market is witnessing strong premiumization, with consumers increasingly shifting toward organic, non-GMO, and sustainably sourced variants. Brands are launching cold-pressed and minimally processed coconut water to enhance nutritional positioning. Premium products are gaining strong traction in North America and Europe, where consumers are willing to pay higher prices for clean-label hydration beverages. Organic certification, ethical sourcing, and eco-friendly packaging are becoming key differentiators in competitive retail environments, significantly increasing brand value and consumer loyalty.

Functional Beverage Innovation and Sports Nutrition Integration

Coconut water is increasingly being integrated into the functional beverage category, particularly in sports and wellness nutrition. Manufacturers are enhancing formulations with added electrolytes, vitamins, and natural flavors to target fitness-conscious consumers. This trend is driven by the growing global sports nutrition industry and rising gym culture. Coconut water is increasingly positioned as a natural alternative to synthetic sports drinks, strengthening its demand among athletes, fitness enthusiasts, and health-focused millennials.

What are the key drivers in the packaged coconut water market?

Rising Health and Wellness Awareness

Growing awareness of lifestyle diseases such as obesity and diabetes is significantly driving demand for healthier beverage alternatives. Consumers are increasingly replacing carbonated soft drinks with natural hydration options like coconut water, which is low in calories and rich in electrolytes. This shift toward preventive health and wellness consumption is one of the strongest structural growth drivers of the market globally.

Expansion of Modern Retail and E-Commerce Channels

The rapid expansion of supermarkets, hypermarkets, and online grocery platforms has significantly improved accessibility to packaged coconut water. E-commerce platforms, in particular, are enabling global reach for both large and niche brands. Digital retailing also supports premium product discovery, subscription-based purchasing, and direct-to-consumer engagement, accelerating market penetration across urban and semi-urban regions.

Growth of Fitness and Functional Beverage Consumption

The increasing popularity of fitness centers, gym memberships, and sports activities is driving strong demand for natural hydration beverages. Coconut water is widely used as a post-workout recovery drink due to its natural electrolyte composition. The growing functional beverage industry, expanding at a strong mid-single-digit to high-single-digit rate, is further supporting sustained demand growth.

What are the restraints for the global market?

Raw Material Supply Chain Volatility

Coconut production is highly dependent on climatic conditions and agricultural cycles, leading to inconsistent supply and price fluctuations. This creates instability in raw material sourcing and impacts production costs, especially for large-scale beverage manufacturers relying on consistent global distribution.

High Pricing Compared to Conventional Beverages

Packaged coconut water remains significantly more expensive than bottled water and carbonated soft drinks. This price gap restricts adoption in price-sensitive markets, particularly in developing economies where consumers prioritize affordability over functional benefits.

What are the key opportunities in the packaged coconut water industry?

Expansion in Emerging Markets

Emerging economies such as India, Indonesia, Brazil, and Vietnam present strong growth opportunities due to rising disposable incomes and urbanization. Increasing awareness of health beverages and expanding modern retail infrastructure are enabling deeper market penetration. Local production initiatives and affordable packaging innovations are expected to significantly boost adoption in these regions.

Growth of Sustainable and Eco-Friendly Packaging

Increasing environmental awareness is creating opportunities for biodegradable, recyclable, and low-carbon packaging solutions. Brands adopting sustainable packaging formats are gaining competitive advantage, particularly in Europe and North America. This trend aligns with global ESG goals and strengthens long-term brand positioning in the premium beverage segment.

Functional and Value-Added Beverage Innovation

There is growing opportunity in developing fortified coconut water products with added vitamins, antioxidants, and plant-based functional ingredients. This allows manufacturers to position coconut water beyond hydration into wellness, immunity support, and sports nutrition categories, significantly expanding target consumer segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4900 Million |

| Market Size in 2026 | USD 5490 Million |

| Market Size in 2031 | USD 8630 Million |

| CAGR | 12% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global coconut water market is strongly led by the 100% pure coconut water segment, which accounts for approximately 48% of the total market share in 2025. This dominance is primarily driven by the accelerating consumer shift toward natural, clean-label, and minimally processed beverages. Modern consumers are increasingly aware of ingredient transparency and are actively avoiding artificial sweeteners, preservatives, and synthetic flavoring agents, which has significantly strengthened the demand for pure coconut water. In addition, rising health consciousness, particularly among urban populations, has positioned pure coconut water as a preferred hydration alternative to carbonated and sugar-heavy drinks. Its natural electrolyte composition, potassium richness, and perceived detoxifying properties further reinforce its popularity in both developed and emerging markets.The organic coconut water segment is experiencing strong growth momentum in premium retail and specialty health channels, particularly in North America and Europe. This growth is driven by increasing consumer willingness to pay premium prices for certified organic and sustainably sourced products. Concerns regarding pesticide usage, environmental sustainability, and ethical sourcing are shaping purchasing behavior. Organic certification is increasingly viewed as a trust signal, enhancing brand credibility and consumer loyalty. Meanwhile, concentrated coconut water variants, though still niche, are gradually gaining relevance in foodservice and industrial applications. Their growth is supported by advantages such as longer shelf life, reduced transportation costs, and ease of integration into ready-to-drink formulations and beverage manufacturing processes.

Application Insights

The household consumption segment remains the largest application category, accounting for over 52% of global demand. This dominance is driven by the integration of coconut water into daily hydration routines, particularly among health-conscious consumers who view it as a functional beverage rather than an occasional drink. Rising awareness of lifestyle-related diseases such as obesity and diabetes has encouraged consumers to replace sugary sodas and artificial juices with natural hydration alternatives. The increasing penetration of e-commerce platforms and retail availability has further made coconut water more accessible to households across both urban and semi-urban regions.The foodservice sector, including hotels, cafés, juice bars, and restaurants, is also contributing steadily to market expansion. Coconut water is increasingly being incorporated into premium beverage menus, cocktails, smoothies, and detox drinks. This trend is driven by consumer demand for healthier dining options and the hospitality industry’s focus on offering innovative, wellness-oriented beverage choices. Additionally, healthcare and wellness applications are gradually emerging, particularly in detox diets, clinical nutrition, and recovery hydration programs. Medical professionals and dietitians are increasingly recommending coconut water for its natural electrolyte balance, further strengthening its credibility in therapeutic nutrition contexts.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape, holding approximately 38% of the global market share. This leadership is attributed to strong product visibility, consumer trust, and the ability to offer multiple brands under one roof. Large retail chains also facilitate promotional pricing, sampling programs, and in-store branding, which significantly influence purchase decisions. The structured retail environment allows consumers to compare product variants easily, reinforcing the dominance of this channel in both developed and developing economies.Specialty health stores and convenience stores continue to play an important role, particularly in urban environments where consumers seek quick access to functional beverages. These channels are especially important for organic, premium, and imported coconut water brands that rely on targeted consumer segments. Foodservice distribution is also expanding steadily, supported by the growth of hospitality and tourism industries, as well as increasing incorporation of coconut water into ready-to-drink and freshly prepared beverages.

Explore more data points, trends and opportunities Download Free Sample Report

Packaged Coconut Water Market Segmentations

By Product Type

- 100% Pure Coconut Water

- Flavored Coconut Water

- Organic Coconut Water

- Concentrated / From Concentrate Coconut Water

By Packaging Type

- Tetra Pak / Carton Packaging

- PET Bottles

- Aluminum Cans

- Pouches & Flexible Packaging

- Glass Bottles

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Health & Specialty Stores

- Foodservice & Institutional Supply

By End Use

- Household / Direct Consumption

- Sports & Fitness Nutrition

- Foodservice

- Healthcare & Wellness Applications

- Corporate & Institutional Consumption

Regional Insights

North America

North America holds approximately 32% of the global coconut water market, with the United States representing the largest contributor within the region. The growth of this market is primarily driven by strong demand for functional beverages, high disposable incomes, and a well-established wellness culture. Consumers in this region are highly responsive to clean-label products, plant-based nutrition, and natural hydration solutions, which has significantly boosted coconut water adoption. The rising prevalence of lifestyle-related health concerns such as obesity and diabetes has further encouraged the substitution of sugary beverages with natural alternatives.The regional growth is also supported by aggressive product innovation, strong retail penetration, and widespread availability across supermarkets, convenience stores, and online platforms. Marketing campaigns emphasizing hydration benefits, electrolyte balance, and fitness recovery have played a key role in strengthening consumer perception. Additionally, the increasing popularity of vegan and plant-based diets continues to reinforce coconut water’s position as a preferred beverage choice in North America.

Asia-Pacific

Asia-Pacific accounts for approximately 38% of the global market and represents the fastest-growing region. The region benefits from a strong coconut production base in countries such as India, Indonesia, Thailand, and the Philippines, which provides a significant supply advantage and cost efficiency. Rising urbanization, expanding middle-class populations, and increasing health awareness are key drivers of regional demand. Consumers are increasingly shifting from traditional sugary beverages to healthier hydration alternatives, particularly in urban centers.The growth of modern retail infrastructure, expanding e-commerce penetration, and increasing exports of coconut-based products are further accelerating market expansion. Government support for agricultural exports and value-added coconut processing industries is also contributing to regional growth. In addition, the strong cultural familiarity with coconut-based consumption in many Asia-Pacific countries enhances acceptance and consumption frequency, making the region both a major producer and consumer hub.

Europe

Europe represents around 18% of the global market, with strong demand concentrated in countries such as the United Kingdom, Germany, and France. The region’s growth is largely driven by sustainability trends, rising demand for organic beverages, and increasing consumer preference for plant-based and vegan-friendly products. European consumers are highly sensitive to product origin, certification, and environmental impact, which has encouraged manufacturers to focus on ethically sourced and sustainably packaged coconut water products.Strict regulatory frameworks regarding food safety and labeling also support demand for high-quality, certified products. The rising popularity of functional beverages, detox diets, and wellness-focused lifestyles has further contributed to market expansion. Additionally, premiumization trends in the beverage industry are driving demand for innovative coconut water variants, including flavored and fortified options.

Latin America

Latin America holds approximately 7% of the global market share, led by countries such as Brazil and Mexico. The region is experiencing steady growth due to increasing urbanization, rising disposable incomes, and greater exposure to global health and wellness trends. Coconut water consumption is gradually gaining traction as consumers adopt healthier beverage alternatives. In some countries, local coconut production also supports domestic supply chains, reducing dependency on imports and improving affordability.The growth of modern retail channels, along with increasing influence from international beverage brands, is further shaping consumer preferences. Although the market is still in a developing phase compared to other regions, long-term growth potential remains strong due to favorable climatic conditions for coconut cultivation and increasing health awareness among younger populations.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global coconut water market. Key demand is concentrated in countries such as the United Arab Emirates, Saudi Arabia, and South Africa. The presence of a large expatriate population with diverse dietary preferences contributes significantly to market demand. High-income consumer segments in the Gulf countries are increasingly adopting premium and imported beverage products, including coconut water, as part of their health-conscious lifestyle.The expansion of modern retail infrastructure, growth in tourism, and increasing penetration of international food and beverage brands are key drivers of regional market development. Additionally, rising awareness of hydration and wellness in hot climatic conditions has strengthened demand for natural electrolyte-rich beverages. Although the market is relatively small compared to other regions, increasing urbanization and lifestyle changes are expected to support steady long-term growth.

Key Players in the Global Packaged Coconut Water Market

- Vita Coco

- Harmless Harvest

- ZICO Beverages

- C2O Pure Coconut Water

- Amy & Brian Naturals

- Naked Juice

- Taste Nirvana

- GraceKennedy

- Green Coco Europe

- Coco Libre

- Real Coco