Out Of Home Food And Beverage Market Size

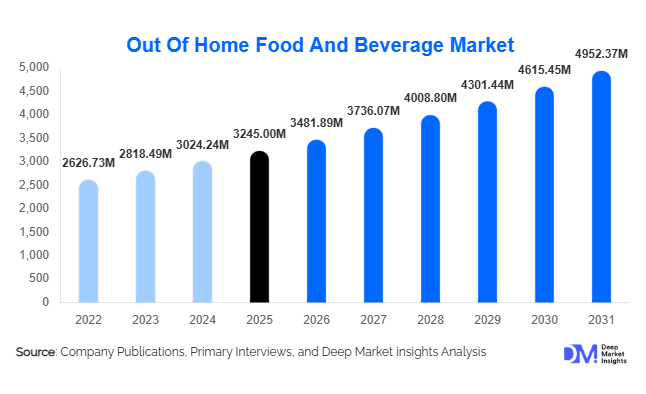

According to Deep Market Insights, the global out-of-home food and beverage market size was valued at USD 3,245 billion in 2025 and is projected to grow from USD 3,481.89 billion in 2026 to reach USD 4,952.37 billion by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). Market expansion is supported by rising urbanization, increasing disposable incomes, growing working populations, and lifestyle shifts favoring convenience dining and social consumption experiences outside households. Rapid growth of quick-service restaurants, café culture, cloud kitchens, travel retail dining, and premium casual dining concepts continues to reshape consumption patterns globally.

Key Market Insights

- Quick-service restaurants (QSRs) dominate global consumption, supported by affordability, digital ordering, and standardized menus.

- Digital ordering and delivery integration are transforming traditional dine-out models into hybrid online–offline consumption ecosystems.

- Asia-Pacific leads demand growth due to rapid urban expansion and rising middle-class consumption.

- Premium casual dining and specialty beverage chains are expanding rapidly in metropolitan markets worldwide.

- Travel and transit foodservice channels are recovering strongly following global mobility normalization.

- Technology adoption, including AI-driven demand forecasting, self-service kiosks, and contactless payments, is improving operational efficiency.

What are the latest trends in the out of home food and beverage market?

Experience-Led Dining and Premiumization

Consumers increasingly view out-of-home food consumption as an experiential activity rather than a purely functional purchase. Restaurants are investing in themed environments, chef-led menus, open kitchens, and experiential dining formats to attract repeat visits. Premium casual dining concepts blending affordability with elevated ambience are expanding globally. Urban millennials and Gen Z consumers prioritize atmosphere, customization, and social-media-friendly experiences, encouraging restaurants to redesign menus and interior formats. Beverage innovation, including artisanal coffee, craft beverages, and functional drinks, is also strengthening premiumization trends.

Digital Transformation of Foodservice Operations

Technology adoption has accelerated across ordering, kitchen operations, and customer engagement. Mobile ordering apps, QR-based menus, loyalty platforms, and AI-powered demand forecasting enable operators to reduce wait times and optimize inventory. Cloud kitchens and virtual restaurant brands are reshaping supply chains by separating production from dine-in infrastructure. Automation technologies such as robotic food preparation and predictive analytics are improving margins while supporting scalability across high-density urban markets.

What are the key drivers in the out of home food and beverage market?

Urbanization and Changing Lifestyles

Rapid urban migration and longer working hours have significantly increased reliance on external food consumption. Dual-income households and younger populations prefer convenience-based meal solutions, boosting demand for restaurants, cafés, and takeaway formats. Expansion of commercial districts and mixed-use developments continues to create new consumption hubs, accelerating foodservice penetration globally.

Growth of Organized Foodservice Chains

Global restaurant chains are expanding aggressively through franchising and standardized operating models. Organized players benefit from purchasing power, brand recognition, and operational efficiencies, allowing competitive pricing and consistent quality. Expansion into tier-2 and tier-3 cities across emerging economies is opening large untapped markets.

Rise of Digital Payments and Delivery Ecosystems

The integration of digital wallets, super apps, and delivery platforms has lowered purchasing friction and expanded accessibility. Consumers increasingly combine dine-in, takeaway, and delivery behaviors, creating omnichannel revenue streams. Data-driven personalization further improves customer retention and order frequency.

What are the restraints for the global market?

Rising Input and Labor Costs

Volatility in agricultural commodities, energy prices, and wages has pressured restaurant margins globally. Operators face increasing operational costs related to rent, staffing shortages, and compliance requirements, forcing frequent menu price adjustments.

Health and Regulatory Pressures

Governments are introducing stricter regulations around nutrition labeling, food safety compliance, and sustainability practices. Growing consumer awareness regarding health and wellness also challenges traditional fast-food offerings, requiring menu reformulation and investment in healthier alternatives.

What are the key opportunities in the out of home food and beverage industry?

Expansion in Emerging Urban Markets

Rapidly growing cities across Asia, Africa, and Latin America present substantial opportunities for organized foodservice expansion. Rising disposable income and youthful demographics are accelerating adoption of branded dining formats. International chains entering secondary cities can capture early market leadership.

Technology Integration and Smart Kitchens

Automation, AI-driven kitchen management, and predictive analytics allow operators to reduce food waste and improve efficiency. Smart kitchens enable scalable operations with lower labor dependence, particularly valuable in high-cost developed markets.

Health-Focused and Functional Menu Innovation

Demand for plant-based meals, low-calorie options, and functional beverages provides strong innovation potential. Restaurants introducing transparency, clean-label ingredients, and nutrition-focused menus can attract health-conscious consumers while maintaining pricing power.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3245 Million |

| Market Size in 2026 | USD 3481.89 Million |

| Market Size in 2031 | USD 4952.37 Million |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

The global foodservice market demonstrates strong structural diversification across service formats, with quick-service restaurants (QSRs) maintaining a dominant position and accounting for approximately 38% of total market revenue in 2025. The leadership of the QSR segment is fundamentally supported by its ability to deliver affordability, operational efficiency, and consistent customer experiences across geographies. Standardized menus, streamlined kitchen operations, and scalable franchise models allow brands to expand rapidly while maintaining cost control and uniform service quality. The increasing integration of digital technologies such as mobile ordering, AI-driven menu optimization, and automated kitchen workflows further strengthens the operational advantage of quick-service operators. Additionally, changing consumer lifestyles characterized by time constraints, dual-income households, and demand for convenience-driven dining solutions continue to reinforce the dominance of this segment globally.The primary growth driver for the leading QSR segment lies in its unmatched scalability and adaptability to evolving consumer behavior. Franchise-led expansion enables rapid penetration into emerging urban centers, suburban markets, and travel hubs while minimizing capital risks for parent companies. Furthermore, QSR brands are increasingly diversifying menus to include healthier options, plant-based alternatives, and regionally customized offerings, enabling them to attract broader consumer demographics. Digital loyalty programs and app-based engagement strategies also play a crucial role in driving repeat purchases and enhancing customer retention.Fast casual dining represents the second-largest service category, gaining traction due to its premium positioning and perceived value proposition that combines quality ingredients with faster service compared to traditional casual dining. Consumers increasingly seek transparency in sourcing, customizable meal options, and elevated dining experiences without significant price premiums. This segment benefits particularly from urban professionals and younger consumers willing to pay moderately higher prices for freshness, personalization, and ambiance.Cafés and beverage chains are experiencing accelerated expansion worldwide, supported by the rapid globalization of coffee culture and the transformation of cafés into social and professional interaction spaces. Urban consumers increasingly utilize cafés as workspaces, meeting locations, and leisure environments, extending average dwell times and boosting revenue per customer. Specialty beverages, seasonal menu innovations, and premium beverage customization trends are strengthening customer engagement. In Asia-Pacific markets especially, café chains are expanding aggressively through localized menu innovation and experiential retail concepts that blend dining, lifestyle branding, and digital engagement.

Food Category Insights

Meals and main courses remain the leading food category, accounting for nearly 46% of global market share in 2025. This dominance is largely driven by sustained consumer reliance on out-of-home dining for lunch and dinner occasions, particularly among urban populations and working professionals. Increasing workforce participation, longer commuting times, and evolving household structures continue to shift meal consumption patterns toward restaurant-based solutions. Full-meal offerings provide higher average transaction values compared to snacks or beverages, making them a central revenue generator for foodservice operators.The leading driver for the meals and main courses segment is the growing substitution of home cooking with convenient restaurant dining solutions. Consumers increasingly prioritize time efficiency and culinary variety, encouraging frequent dining outside the home. Restaurants are responding by expanding menu diversity, introducing global cuisines, and offering nutritionally balanced meal combinations that appeal to health-conscious consumers. Additionally, value meal bundling strategies and subscription-style meal programs are enhancing customer loyalty while stabilizing demand patterns.Beverages represent the fastest-growing category globally, supported by innovation across specialty coffee, premium teas, functional drinks, and non-alcoholic beverages. Rising demand for premiumization and experiential consumption plays a central role in category expansion. Beverage-focused outlets benefit from high margins, frequent purchase cycles, and strong brand differentiation opportunities. Consumers increasingly view beverages not merely as complementary items but as standalone consumption experiences, driven by social media influence and lifestyle branding.Snack-based consumption is also rising steadily as eating habits become more flexible and less structured around traditional meal times. Increased mobility, urban commuting, and on-the-go lifestyles contribute to growing demand for portable food options. Operators are expanding snack portfolios to include healthier alternatives, fusion flavors, and globally inspired offerings, enabling them to capture incremental consumption occasions throughout the day.

Distribution Channel Insights

Dine-in services continue to dominate global foodservice distribution channels, holding approximately 52% market share. Despite rapid digital transformation, consumers still value physical dining experiences that provide social interaction, ambiance, and experiential engagement. Restaurants increasingly focus on interior design, themed environments, and experiential dining concepts to differentiate themselves and maintain dine-in traffic. Social dining remains deeply embedded in cultural behaviors across regions, reinforcing the long-term relevance of physical restaurant spaces.The primary driver behind the continued dominance of dine-in channels is experiential consumption. Consumers increasingly seek dining occasions that combine food with entertainment, socialization, and lifestyle expression. Restaurants are evolving into multi-functional venues offering live events, interactive menus, and immersive culinary experiences that cannot be replicated through delivery formats alone.However, takeaway and delivery channels are witnessing the fastest growth, fueled by widespread adoption of digital ordering platforms and mobile applications. Cloud kitchens, virtual brands, and hybrid restaurant models are reshaping operational structures by enabling businesses to serve delivery demand without extensive physical infrastructure. Partnerships between restaurants and third-party delivery aggregators significantly expand market reach while improving accessibility for consumers.The integration of omnichannel strategies is becoming a defining industry trend. Restaurants increasingly balance dine-in, takeaway, and delivery operations to optimize revenue streams and improve resilience against demand fluctuations. Advanced data analytics allows operators to forecast demand patterns, personalize promotions, and streamline logistics, further accelerating distribution channel transformation.

Location Type Insights

Standalone restaurants account for roughly 44% of global revenue, supported by strong neighborhood-level demand and localized customer loyalty. Independent street-facing outlets benefit from accessibility, community engagement, and flexible operational formats. These locations often adapt menus and pricing strategies according to local preferences, enabling sustained customer relationships and repeat visits.The leading driver for standalone restaurant dominance is proximity-based convenience combined with brand familiarity. Consumers frequently choose dining locations near residential or workplace areas, making neighborhood restaurants integral to daily consumption habits. Operators increasingly leverage localized marketing strategies and hyperlocal delivery services to strengthen their competitive positioning.Mall-based outlets continue to benefit from high consumer footfall generated by integrated retail ecosystems. Shopping centers serve as lifestyle destinations where dining complements entertainment and retail experiences. As malls evolve into experiential hubs incorporating cinemas, gaming zones, and family entertainment centers, foodservice operators gain access to diversified consumer segments and longer visitation durations.Travel hubs including airports, railway stations, and transit terminals are witnessing accelerated recovery and expansion. Rising global tourism, business travel normalization, and increased domestic commuting are driving demand for quick-service and beverage-oriented formats within transportation environments. Operators prioritize speed, menu simplification, and digital payment integration to cater to time-sensitive travelers.

End-Use Insights

Individual consumers dominate global foodservice demand, contributing nearly 68% of total consumption. Personal dining occasions across daily meals, social gatherings, and leisure activities form the backbone of industry revenue. Urbanization, lifestyle changes, and increased disposable income continue to expand consumer spending on out-of-home food experiences.The leading driver for individual consumer dominance is lifestyle transformation driven by urban employment patterns and changing social behaviors. Younger demographics increasingly prioritize convenience, variety, and experiential dining, resulting in higher dining frequency. Digital discovery platforms and social media influence further encourage experimentation with new cuisines and restaurant formats.Corporate catering and institutional foodservice segments are expanding steadily as organizations reintroduce workplace dining programs following hybrid work stabilization. Companies increasingly view food services as part of employee wellness and productivity strategies, supporting consistent demand for organized catering solutions.The tourism and hospitality sector represents the fastest-growing end-use segment, supported by increasing international travel flows and investments in hospitality infrastructure. Hotels, resorts, and integrated entertainment complexes increasingly collaborate with established foodservice brands to enhance guest experiences and diversify revenue streams.

End-Use Industry Analysis

The hospitality and tourism industry remains a central growth engine for global out-of-home food consumption. As international travel continues recovering and expanding, hotels and resorts are investing heavily in diversified dining concepts to attract guests and increase on-site spending. Many hospitality operators outsource restaurant management to specialized foodservice companies, enabling operational efficiency while maintaining premium service standards.Corporate offices and co-working environments are emerging as significant demand centers for organized foodservice. Employers increasingly incorporate dining amenities to enhance workplace satisfaction, encourage collaboration, and support employee retention. Technology-enabled ordering systems, pre-planned meal subscriptions, and smart cafeteria solutions are reshaping institutional dining models.Export-driven tourism markets across Southeast Asia and the Middle East are generating substantial foodservice revenues due to rising international visitor spending. Culinary tourism is gaining importance as travelers actively seek authentic local food experiences, encouraging restaurants to integrate regional cuisine storytelling and cultural elements into dining offerings.Additionally, the expansion of entertainment venues such as multiplex cinemas, theme parks, sports arenas, and cultural attractions is creating new consumption environments. These venues increasingly rely on branded quick-service and beverage operators to manage high-volume demand efficiently, supporting sustained growth opportunities for foodservice providers.

Explore more data points, trends and opportunities Download Free Sample Report

Out Of Home Food And Beverage Market Segmentations

By Outlet Type

- Quick Service Restaurants

- Full-Service Restaurants

- Cafés & Coffee Chains

- Street Food Vendors & Kiosks

- Cloud Kitchens & Delivery-Only Brands

- Institutional Catering & Contract Foodservice

By Food Category

- Meals & Main Courses

- Snacks & Fast Food

- Beverages

- Bakery & Confectionery Products

- Desserts & Ice Cream

By Service Model

- Dine-In Services

- Takeaway/Take-Out

- Home Delivery

- Drive-Thru

- Grab-and-Go & Convenience Consumption

By Distribution Channel

- Direct Restaurant Sales

- Online Food Delivery Platforms

- Corporate & Institutional Contracts

- Travel, Leisure & Transit Locations

Regional Insights

North America

North America accounted for approximately 27% of global market share in 2025, maintaining a mature yet innovation-driven foodservice ecosystem. The United States leads regional performance due to its highly organized restaurant industry, advanced franchise infrastructure, and widespread adoption of digital ordering technologies. Consumer familiarity with chain restaurants and strong brand loyalty support consistent revenue generation across service formats.Regional growth is primarily driven by technological innovation and premiumization trends. High digital penetration enables seamless integration of mobile ordering, delivery logistics, and loyalty programs, improving operational efficiency and customer engagement. Rising demand for healthier menus, plant-based alternatives, and sustainability-focused dining concepts also contributes to market evolution. Canada complements regional growth through expanding café culture, multicultural cuisine adoption, and increasing consumer willingness to spend on premium casual dining experiences.

Europe

Europe represents around 23% of global market share, characterized by diverse culinary traditions and strong café culture embedded in social lifestyles. Countries including the United Kingdom, Germany, France, Italy, and Spain drive regional demand through high urbanization and tourism activity.Regional growth is supported by sustainability-driven innovation and premium experiential dining. European consumers increasingly prioritize locally sourced ingredients, ethical supply chains, and environmentally responsible operations, encouraging restaurants to adopt sustainable practices. Outdoor dining culture, heritage cuisine preservation, and strong tourism flows further stimulate restaurant demand. Additionally, digital reservation platforms and delivery services are modernizing traditional dining markets while maintaining cultural authenticity.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region, holding nearly 34% global share in 2025. Rapid urbanization, rising middle-class income levels, and demographic advantages position the region as a long-term growth engine for global foodservice expansion. China leads regional demand through large-scale urban population growth and a highly developed delivery ecosystem.Regional growth drivers include expanding organized restaurant chains, increasing smartphone penetration, and strong youth demographics that favor dining out and digital food ordering. India represents one of the fastest-growing markets, supported by rapid QSR expansion, evolving consumption patterns, and increasing participation of international brands. Japan and South Korea contribute high per-capita spending levels through premium dining formats, technological integration, and strong consumer demand for quality-driven culinary experiences. The rapid rise of café culture and specialty beverage consumption across Southeast Asia further strengthens regional growth momentum.

Middle East & Africa

The Middle East demonstrates strong growth led by the United Arab Emirates and Saudi Arabia, supported by large-scale tourism investments, urban megaprojects, and mall-centric retail ecosystems. Dining experiences are closely integrated with shopping and entertainment environments, driving consistent restaurant traffic.Key regional growth drivers include government-led economic diversification initiatives, expanding expatriate populations, and rising disposable incomes. International franchise brands continue entering major Gulf markets, contributing to rapid industry modernization. In Africa, emerging demand across South Africa, Nigeria, and Kenya is driven by urban population expansion, improving retail infrastructure, and increasing exposure to organized dining formats. The gradual formalization of foodservice operations and rising youth demographics present long-term growth opportunities.

Latin America

Latin America accounts for roughly 8% of global market share, led primarily by Brazil and Mexico. The region is experiencing steady expansion supported by growing middle-class populations and increasing urban consumption patterns.Regional growth drivers include the rapid expansion of franchise-based quick-service restaurant chains, improving digital payment adoption, and rising popularity of delivery platforms. Consumers increasingly seek affordable dining options combined with localized flavors, encouraging global brands to adapt menus to regional tastes. Economic recovery trends and expanding retail infrastructure are further enhancing foodservice accessibility across metropolitan areas, positioning Latin America as an emerging growth market within the global industry landscape.

Key Players in the Out Of Home Food And Beverage Market

- McDonald's Corporation

- Starbucks Corporation

- Yum! Brands Inc.

- Restaurant Brands International Inc.

- Domino's Pizza Inc.

- Subway IP LLC

- Chipotle Mexican Grill Inc.

- Darden Restaurants Inc.

- Compass Group PLC

- Sodexo S.A.

- Aramark Corporation

- Jollibee Foods Corporation

- Whitbread PLC

- The Wendy’s Company

- Inspire Brands Inc.