Organic Yeast Market Size

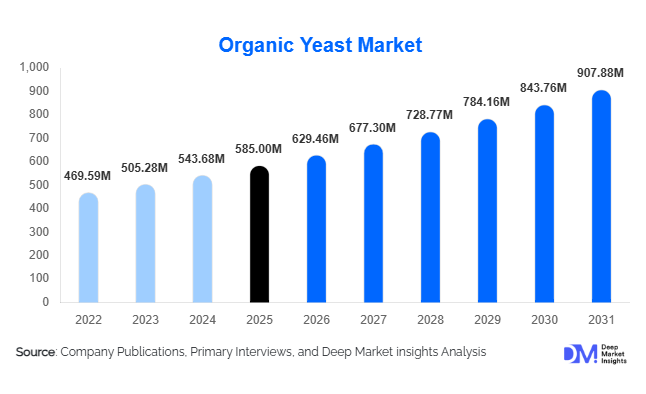

According to Deep Market Insights, the global organic yeast market size was valued at USD 585 million in 2025 and is projected to grow from USD 629.46 million in 2026 to reach USD 907.88 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The organic yeast market is primarily driven by accelerating demand for certified organic food ingredients, the expansion of clean-label bakery products, rising consumption of organic alcoholic beverages, and the increasing incorporation of nutritional yeast into plant-based and functional food formulations.

Key Market Insights

- Organic baker’s yeast dominates the market, accounting for nearly 38% of total revenue in 2025, supported by strong demand from organic bread and artisan bakery manufacturers.

- North America leads the global market, contributing approximately 32% of total revenue, driven by the U.S. organic food and craft brewing industries.

- Europe holds around 30% market share, supported by robust organic certification frameworks and high consumption of organic wine and bakery products.

- Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR due to increasing organic food exports and government-backed agricultural reforms.

- B2B distribution accounts for nearly 70% of total sales, reflecting industrial procurement by food processors, breweries, and nutraceutical manufacturers.

- The top five players control approximately 48% of the global market share, indicating moderate consolidation with strong technological and certification barriers to entry.

What are the latest trends in the organic yeast market?

Rising Adoption in Plant-Based and Functional Foods

Organic nutritional yeast is increasingly incorporated into vegan cheese, dairy alternatives, protein snacks, and fortified spreads due to its natural umami flavor and vitamin B-complex content. As the global plant-based food industry surpasses USD 45 billion, demand for certified organic fermentation inputs is rising proportionately. Food manufacturers are prioritizing clean-label fortification strategies, using organic yeast extracts instead of synthetic flavor enhancers. This shift is positioning organic yeast as a strategic ingredient in premium, health-oriented product lines.

Premiumization in Organic Craft Brewing and Wine

Organic brewer’s and wine yeast segments are expanding alongside premium organic alcohol production. Craft breweries and biodynamic wineries increasingly require traceable, certified fermentation strains such as Saccharomyces cerevisiae to maintain organic labeling integrity. The organic alcoholic beverage segment is growing at 8–10% annually, creating higher-margin opportunities for specialized yeast strains with improved fermentation efficiency and flavor stability.

What are the key drivers in the organic yeast market?

Growing Global Demand for Clean-Label Ingredients

Consumers are increasingly rejecting synthetic additives and genetically modified ingredients. Organic yeast aligns with USDA Organic and EU Organic certification requirements, making it a preferred fermentation agent for organic packaged foods. Organic bakery penetration in developed markets continues to expand, directly driving upstream yeast demand.

Expansion of Organic Alcoholic Beverage Production

Organic beer and wine production volumes are increasing across the U.S., France, Italy, and Germany. Breweries and wineries require certified organic yeast to ensure compliance across the supply chain. Export-driven premium alcohol production further strengthens consistent demand for high-performance organic fermentation strains.

What are the restraints for the global market?

Higher Production and Certification Costs

Organic yeast production requires certified organic substrates, dedicated processing lines, and compliance audits. These requirements increase operating costs by 15–25% compared to conventional yeast production, limiting price competitiveness in cost-sensitive markets.

Raw Material Supply Volatility

Organic molasses and fermentation substrates depend on agricultural cycles and climate conditions. Crop yield fluctuations and trade restrictions can affect supply consistency, impacting pricing stability and margins for manufacturers.

What are the key opportunities in the organic yeast industry?

Asia-Pacific Manufacturing Expansion

Countries such as China and India are promoting organic agriculture through national initiatives, supporting domestic ingredient production. Local fermentation facilities can reduce import dependency and capitalize on rapidly growing organic packaged food exports. Asia-Pacific is projected to grow at nearly 10% CAGR, presenting strong long-term investment potential.

Integration into Nutraceutical and Probiotic Supplements

Strains like Saccharomyces boulardii are widely used in digestive health supplements. With the probiotic supplement industry exceeding USD 70 billion globally, organic-certified inputs are gaining preference in premium formulations. Manufacturers investing in clinically supported organic strains can achieve strong margin expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 585 Million |

| Market Size in 2026 | USD 629.46 Million |

| Market Size in 2031 | USD 907.88 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Organic baker’s yeast represents the largest segment, accounting for approximately 38% of global revenue in 2025. The segment’s leadership is driven primarily by the rapid expansion of certified organic bakery production in North America and Europe, where organic bread, artisan sourdough, and clean-label packaged baked goods are seeing double-digit retail shelf penetration. Large commercial bakeries are increasingly switching to certified fermentation inputs to maintain the integrity of USDA Organic and EU Organic labeling. Additionally, the growth of frozen organic dough and ready-to-bake products has strengthened demand for high-performance organic yeast strains that ensure consistent leavening, extended shelf life, and fermentation stability.

Organic yeast extract is gaining traction due to its ability to serve as a natural flavor enhancer in savory snacks, soups, sauces, and plant-based meat alternatives. As food manufacturers reformulate products to remove monosodium glutamate (MSG) and artificial additives, organic yeast extract is emerging as a strategic clean-label solution. Meanwhile, organic brewer’s and wine yeast segments are benefiting from the premiumization of organic craft beer and biodynamic wine exports, particularly from the U.S., France, Italy, and Germany. Organic feed yeast, though smaller in share, remains stable due to rising organic dairy and poultry farming, especially across Europe, where animal feed traceability regulations are stringent.

Application Insights

Organic bakery and confectionery applications account for nearly 42% of total global demand, making it the leading application segment. The growth driver for this segment is the increasing consumer shift toward clean-label, non-GMO, and preservative-free bakery items. Supermarket private-label organic bread lines and premium artisan bakeries are expanding across developed economies, reinforcing yeast procurement volumes.

Alcoholic beverage applications represent the fastest-growing segment, expanding at close to 9% annually. This growth is supported by the expansion of organic craft breweries and biodynamic vineyards, where fermentation traceability is essential. Nutraceutical applications are emerging rapidly, particularly for probiotic strains used in digestive health supplements. Rising consumer awareness of gut health, immunity, and plant-based nutrition is supporting premium organic yeast incorporation. Animal feed applications continue to grow moderately, particularly in organic-certified dairy and poultry production systems in Europe and North America.

Distribution Channel Insights

B2B industrial sales dominate the market, accounting for approximately 70% of total revenue. Large-scale food processors, breweries, and nutraceutical manufacturers procure organic yeast in bulk under long-term supply agreements. The primary driver for this channel’s dominance is industrial-scale organic food production and the need for consistent quality, certification compliance, and fermentation reliability.

On the B2C side, specialty organic retail stores and e-commerce platforms are gaining importance, particularly for active dry and instant organic yeast formats tailored for home baking. Post-pandemic baking trends and growing interest in homemade sourdough and clean-label cooking have sustained steady retail demand growth.

End-Use Industry Insights

The food processing industry remains the largest end-use sector, accounting for approximately 48% of global demand and valued at nearly USD 280 million in 2025. The primary driver for this segment is the rapid growth of organic packaged foods, including bread, snacks, ready meals, and plant-based alternatives. Food manufacturers are increasingly integrating organic yeast as a foundational fermentation ingredient to meet certification requirements.

The alcoholic beverage industry is the fastest-growing end-use segment, expanding at nearly 9% annually. Growth is fueled by premium organic beer and wine production, especially in export-driven markets. The nutraceutical industry is gaining momentum due to increasing global digestive health awareness and demand for organic-certified probiotic ingredients. Additionally, organic animal nutrition contributes to stable growth, particularly in Europe’s regulated organic livestock markets and North America’s specialty dairy exports.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Yeast Market Segmentations

By Product Type

- Organic Baker’s Yeast

- Organic Brewer’s Yeast

- Organic Nutritional Yeast

- Organic Wine Yeast

- Organic Feed Yeast

- Organic Yeast Extract

By Application

- Organic Bakery & Confectionery

- Organic Alcoholic Beverages

- Organic Dietary Supplements

- Organic Animal Feed & Aquaculture

- Organic Savory & Processed Foods

By Distribution Channel

- B2B Industrial Sales

- Specialty Organic Stores

- Supermarkets & Hypermarkets

- Online & Direct-to-Consumer

By End-Use Industry

- Food Processing Industry

- Alcoholic Beverage Industry

- Nutraceutical Industry

- Animal Nutrition Industry

Regional Insights

North America

North America holds approximately 32% of the global organic yeast market share in 2025, with the United States accounting for nearly 80% of regional consumption. The primary regional growth drivers include strong organic retail penetration, well-established USDA Organic certification systems, and rapid expansion of the craft brewing industry. The U.S. also benefits from advanced fermentation technology infrastructure and strong demand from nutraceutical companies producing probiotic supplements. Canada contributes steady growth supported by organic grain production, bakery exports, and rising organic dairy farming. High disposable income and mature distribution networks further sustain regional dominance.

Europe

Europe accounts for nearly 30% of global revenue, led by Germany, France, Italy, and the United Kingdom. The region’s growth is driven by strict EU organic regulations, strong consumer preference for sustainable food systems, and widespread availability of organic products in retail chains. Germany remains Europe’s largest organic bakery market, while France and Italy drive demand for organic wine fermentation yeast due to their global wine export leadership. Additionally, Europe’s well-developed organic livestock farming sector supports stable feed yeast demand. Government incentives promoting organic agriculture and sustainability initiatives further reinforce long-term growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at nearly 10% CAGR. China is investing heavily in domestic organic agriculture and fermentation capacity to reduce reliance on imports, supported by national food security and manufacturing initiatives. India is emerging as an organic bakery export hub, driven by rising domestic consumption and expanding processed food exports. Japan and Australia represent mature premium markets with steady demand for organic health foods and nutraceutical ingredients. Increasing middle-class income levels, urbanization, and export-oriented food manufacturing are key regional growth drivers.

Latin America

Brazil and Argentina lead regional demand, supported by abundant organic sugarcane production used as fermentation substrate and expanding organic livestock farming. Growth in export-oriented processed foods and gradual consumer awareness of organic labeling standards are strengthening demand. While overall regional market share remains moderate, improving agricultural infrastructure and trade partnerships are expected to enhance long-term growth prospects.

Middle East & Africa

The Middle East & Africa region currently holds a smaller share of global revenue but demonstrates rising potential. The UAE leads regional imports of premium organic food products, driven by high-income consumers and a strong hospitality sector. South Africa is emerging as a regional production and consumption hub, supported by organic wine exports and growing retail penetration. Increasing urbanization, rising health awareness, and expanding premium food imports are the key drivers stimulating gradual organic yeast adoption across the region.

Key Players in the Organic Yeast Market

- Lesaffre

- AB Mauri

- Lallemand Inc.

- Angel Yeast Co., Ltd.

- Chr. Hansen

- Leiber GmbH

- Biorigin

- Kerry Group

- Associated British Foods

- Pakmaya

- DSM-Firmenich

- Ohly

- Alltech

- Synergy Flavors

- BASF