Organic Wheat Flour Market Size

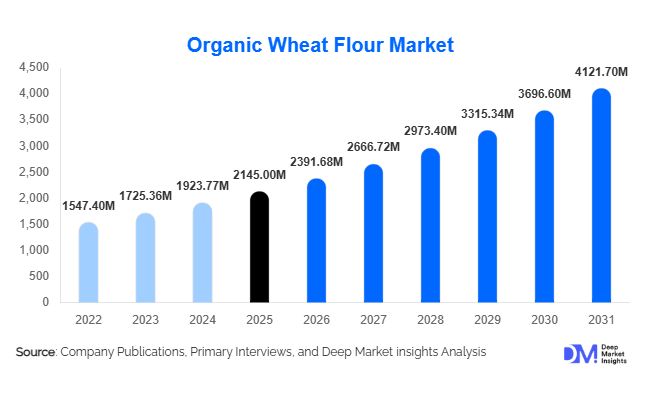

According to Deep Market Insights, the global organic wheat flour market size was valued at USD 2,145 million in 2025 and is projected to grow from USD 2,391.68 million in 2026 to reach USD 4,121.70 million by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). Market growth is driven by rising consumer preference for clean-label food products, increasing awareness regarding pesticide-free agricultural practices, and expanding demand for organic bakery and packaged food products worldwide. The transition toward healthier diets, coupled with regulatory support for organic farming across North America, Europe, and Asia-Pacific, is accelerating adoption across both retail and industrial food processing sectors.

Key Market Insights

- Clean-label and chemical-free food consumption trends are significantly boosting demand for certified organic wheat flour globally.

- Bakery and packaged food manufacturers are increasingly reformulating products using organic ingredients to meet premium consumer demand.

- North America leads global consumption, supported by strong organic certification frameworks and high consumer purchasing power.

- Asia-Pacific is the fastest-growing region, driven by urbanization and expanding middle-class health awareness in India and China.

- Private-label organic brands are expanding rapidly through supermarkets and online grocery platforms.

- Digital traceability and farm-to-table transparency are becoming key differentiators among leading producers.

What are the latest trends in the organic wheat flour market?

Shift Toward Clean-Label and Functional Organic Foods

Consumers are increasingly scrutinizing ingredient lists and avoiding synthetic additives, leading to strong adoption of organic wheat flour in bakery, snacks, and ready-to-eat meals. Food manufacturers are positioning organic wheat flour as a premium ingredient aligned with health, sustainability, and ethical sourcing values. Functional organic flour variants enriched with fiber, ancient grain blends, and high-protein formulations are gaining traction, especially among urban consumers focused on wellness and preventive nutrition.

Expansion of Organic Private Labels and E-commerce Sales

Retailers are expanding private-label organic flour offerings to capture growing demand while maintaining competitive pricing. Online grocery platforms are accelerating accessibility to certified organic wheat flour products globally. Subscription-based grocery models and direct-to-consumer supply chains are reducing dependency on traditional distribution networks, improving margins for producers while enhancing consumer convenience.

What are the key drivers in the organic wheat flour market?

Growing Health Awareness and Organic Food Consumption

Rising awareness regarding pesticide residues and food safety concerns is encouraging consumers to shift toward certified organic grain products. Organic wheat flour is perceived as nutritionally superior and environmentally sustainable, making it a preferred choice among health-conscious consumers. Increasing adoption of plant-based and whole-food diets further strengthens demand.

Expansion of Organic Farming and Government Support

Government incentives promoting organic agriculture, including subsidies, certification assistance, and sustainable farming programs, are increasing organic wheat cultivation globally. Policies supporting regenerative agriculture and soil health improvement are encouraging farmers to transition from conventional to organic practices, strengthening supply chains.

Growth of Organic Bakery and Processed Food Industry

Industrial food processors are incorporating organic wheat flour into bread, biscuits, pasta, and snack production to capture premium market segments. Rising demand for organic packaged foods across supermarkets and foodservice channels is directly supporting flour consumption growth.

What are the restraints for the global market?

Higher Production and Certification Costs

Organic wheat cultivation involves lower yields and strict certification requirements, increasing production costs compared to conventional wheat flour. These higher costs translate into premium pricing, limiting adoption among price-sensitive consumers in developing markets.

Supply Chain and Raw Material Volatility

Organic wheat supply remains vulnerable to climatic variations, limited certified farmland, and inconsistent yields. Supply-demand imbalances can cause price volatility, affecting manufacturer margins and procurement stability.

What are the key opportunities in the organic wheat flour industry?

Expansion in Emerging Markets

Rapid urbanization and increasing disposable income across Asia-Pacific and Latin America present significant growth opportunities. Rising health awareness and expansion of organized retail are enabling wider penetration of organic staples such as wheat flour.

Integration with Sustainable and Regenerative Agriculture

Companies investing in regenerative farming practices and carbon-neutral supply chains can strengthen brand positioning while meeting sustainability targets demanded by global retailers and consumers.

Innovation in Value-Added Organic Flour Products

Opportunities exist in fortified organic flour, gluten-sensitive blends, and specialty baking solutions designed for artisanal bakeries and premium foodservice operators. Innovation allows manufacturers to command higher margins and differentiate products.

Product Type Insights

The organic wheat flour market demonstrates strong product diversification; however, whole organic wheat flour continues to dominate the global landscape, accounting for approximately 42% of the global market share in 2025. The leadership of this segment is primarily driven by increasing consumer awareness regarding nutritional density, digestive health benefits, and the demand for minimally processed food products. Whole organic wheat flour retains bran and germ components, making it rich in fiber, vitamins, and antioxidants, which aligns closely with rising clean-label and functional food consumption trends worldwide. Growing incidences of lifestyle-related health concerns, including obesity and digestive disorders, have further encouraged consumers to transition toward whole-grain organic alternatives, strengthening long-term segment growth.All-purpose organic wheat flour represents the second-largest segment due to its versatility across household cooking and commercial bakery applications. Its adaptability for bread, cakes, sauces, and processed foods makes it highly preferred among both home consumers and food manufacturers seeking organic reformulations without altering product texture or taste profiles. Increasing penetration of organic private-label brands across supermarkets and retail chains has also expanded accessibility, supporting sustained adoption. Meanwhile, specialty organic wheat flour varieties, including stone-ground, sprouted, and heritage grain flours, are witnessing accelerated growth as artisanal baking, premium culinary experimentation, and craft food movements gain global popularity. Consumers increasingly associate specialty flour variants with authenticity, superior flavor, and traditional milling techniques, encouraging premiumization within the organic flour category.

Application Insights

Bakery products remain the largest application segment, contributing nearly 46% of global demand in 2025, supported by the rapid expansion of organic bread, pastries, cookies, and baked snacks across both developed and emerging markets. The dominance of this segment is driven by the growing consumer preference for healthier indulgence options, prompting commercial bakeries to replace conventional ingredients with certified organic alternatives. Retail bakeries and packaged baked goods manufacturers increasingly leverage organic labeling to achieve premium positioning and brand differentiation, particularly in North America and Europe.Household consumption continues to demonstrate steady expansion as home cooking and baking habits established during recent years remain persistent. Consumers are increasingly experimenting with organic ingredients for everyday meals, encouraged by social media food trends and increased availability of smaller packaging formats. In addition, pasta and noodle manufacturing is emerging as one of the fastest-growing application areas. The expansion of clean-label packaged foods and organic convenience meals has encouraged manufacturers to integrate organic wheat flour into dried pasta, instant noodles, and ready-to-cook meal kits. Rising global demand for preservative-free and traceable ingredients further strengthens the adoption of organic wheat flour across processed food categories.

Distribution Channel Insights

Supermarkets and hypermarkets lead the distribution landscape with approximately 38% market share, primarily due to strong product visibility, wide assortment availability, and expanding organic private-label offerings. Large retail chains continue to invest in dedicated organic sections, improving consumer education and enhancing purchase confidence through certification labeling and transparent sourcing information. Promotional campaigns and competitive pricing strategies have further enabled mainstream adoption beyond niche health-food consumers.Online retail is emerging as the fastest-growing distribution channel, supported by the rapid digitalization of grocery purchasing behavior and increasing consumer preference for convenience-driven shopping experiences. Subscription-based organic food delivery models, direct-to-consumer brand strategies, and e-commerce marketplace expansion have significantly improved product accessibility, particularly in urban areas. Enhanced logistics infrastructure and digital payment adoption in emerging economies are accelerating online organic food purchases, allowing smaller organic producers to reach broader customer bases without traditional retail limitations.

End-Use Industry Insights

The food processing industry accounts for nearly 52% of organic wheat flour demand, making it the leading end-use sector globally. The segment’s dominance is fueled by the rapid expansion of organic packaged foods, including breakfast products, snacks, frozen meals, and ready-to-eat bakery items. Food manufacturers are increasingly reformulating product portfolios to align with clean-label standards, non-GMO requirements, and sustainability commitments, all of which favor organic ingredient adoption. Rising consumer trust in certified organic processed foods continues to reinforce industrial-scale demand.Foodservice establishments are also witnessing rising adoption, particularly among artisanal bakeries, specialty cafés, and premium restaurants seeking to differentiate menus through organic and sustainably sourced ingredients. Culinary professionals increasingly emphasize ingredient transparency and nutritional quality to appeal to health-conscious diners. Additionally, export-oriented demand is expanding as European and North American markets import organic wheat flour and raw materials from emerging agricultural economies where organic farming acreage is growing rapidly. International trade agreements and certification harmonization are further facilitating cross-border supply chains.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America held approximately 34% of the global market share in 2025, led primarily by the United States, where mature organic certification frameworks and strong consumer awareness create a highly developed market environment. Growth in the region is driven by increasing demand for clean-label packaged foods, strong penetration of organic private-label brands, and rising health-focused dietary preferences among millennials and Gen Z consumers. Advanced retail infrastructure, widespread availability of organic bakery products, and innovation in plant-based and functional foods continue to accelerate flour consumption. Canada complements regional growth through expanding organic farming acreage and increasing adoption among commercial bakeries responding to premium consumer demand.

Europe

Europe accounted for nearly 29% market share, supported by stringent food safety standards, sustainability-driven agricultural policies, and environmentally conscious consumer behavior. Countries such as Germany, France, Italy, and the United Kingdom lead consumption due to strong demand for traditional bread products made with organic ingredients. Regional growth is further driven by government incentives promoting organic farming practices, reduced pesticide usage regulations, and high consumer trust in certification systems. The popularity of artisanal baking culture and locally sourced ingredients continues to strengthen demand for organic wheat flour across both retail and foodservice sectors.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, led by India, China, Japan, and Australia. Rapid urbanization, expanding middle-class populations, and rising disposable incomes are encouraging consumers to shift toward healthier staple food alternatives. India is emerging as both a major producer and consumer due to expanding organic farmland, favorable climatic conditions, and government initiatives promoting sustainable agriculture and natural farming practices. Increasing e-commerce grocery adoption and rising awareness of food safety following concerns around chemical residues are accelerating organic food purchases throughout the region. Additionally, growing demand for premium bakery and Western-style food products is expanding organic flour applications.

Latin America

Latin America is witnessing steady expansion, with Brazil and Argentina serving as key contributors due to strong agricultural capabilities and increasing organic grain exports. Regional growth is supported by favorable farming conditions, rising participation in global organic supply chains, and increasing domestic awareness of healthy diets. Investments in organic certification and export-oriented production models enable producers to supply high-demand markets in North America and Europe. Urbanization and modernization of retail infrastructure are also encouraging local consumption of organic packaged foods.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but consistent growth, particularly in the UAE, Saudi Arabia, and South Africa. Rising disposable income levels, expanding expatriate populations, and growing exposure to global health trends are increasing demand for premium organic food products. Dependence on imported organic ingredients supports international trade flows, while rapid expansion of modern retail formats and specialty organic stores improves product accessibility. Urban consumers are increasingly prioritizing food quality, safety, and nutritional value, driving adoption of organic staple foods such as wheat flour across both retail and foodservice sectors.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Organic Wheat Flour Market

- Ardent Mills

- King Arthur Baking Company

- Bob’s Red Mill Natural Foods

- General Mills Inc.

- Hain Celestial Group

- Hodgson Mill

- Bay State Milling Company

- Arrowhead Mills

- Doves Farm Foods Ltd.

- Anita’s Organic Mill

- Shipton Mill Ltd.

- Nature Bio Foods Ltd.

- Organic India Pvt. Ltd.

- Grain Millers Inc.

- To Your Health Sprouted Flour Co.