Organic Spices Market Size

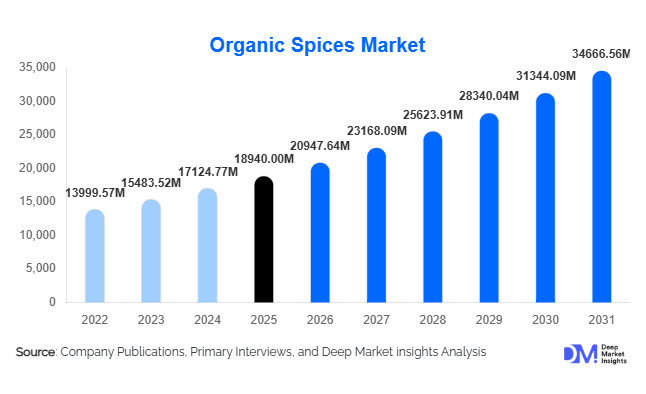

According to Deep Market Insights, the global organic spices market size was valued at USD 18,940 million in 2025 and is projected to grow from USD 20,947.64 million in 2026 to reach USD 34,666.56 million by 2031, expanding at a CAGR of 10.6% during the forecast period (2026–2031). Market expansion is driven by increasing consumer preference for chemical-free food ingredients, rising awareness regarding pesticide residues in conventional spices, and strong demand from premium food processing and health-oriented retail segments. The organic spices industry is transitioning from niche specialty retail toward mainstream food manufacturing, supported by certification frameworks, improved global supply chains, and expanding private-label organic product portfolios.

The market reflects a structural shift toward clean-label consumption, particularly across developed economies and urbanizing regions in Asia-Pacific. Organic spices such as turmeric, pepper, cumin, ginger, and chili are increasingly integrated into packaged foods, nutraceutical formulations, and functional beverages. Growth is further supported by expanding export-oriented agriculture in producing countries including India, Vietnam, Sri Lanka, and Indonesia, where government-backed organic farming initiatives are improving traceability and farmer participation. E-commerce platforms and specialty organic retail channels have widened accessibility, allowing smaller brands to compete globally. Additionally, rising demand from vegan, plant-based, and immunity-focused diets has elevated organic spices from culinary ingredients to wellness products, strengthening long-term market fundamentals.

Key Market Insights

- Organic turmeric and pepper dominate global demand due to strong application in functional foods and nutraceuticals.

- Asia-Pacific leads production and exports, while North America and Europe remain premium consumption markets.

- Retail packaged organic spices are expanding rapidly through supermarkets and online grocery platforms.

- Food processing companies are integrating organic-certified inputs to meet clean-label requirements.

- Private-label organic spice brands are increasing competition and price accessibility.

- Traceability technologies and blockchain adoption are improving supply chain transparency.

What are the latest trends in the organic spices market?

Shift Toward Functional and Immunity-Boosting Ingredients

Organic spices are increasingly positioned as health-supporting ingredients rather than purely flavoring agents. Consumers associate spices such as turmeric, ginger, cinnamon, and cloves with anti-inflammatory and antioxidant properties, driving their incorporation into wellness beverages, dietary supplements, and fortified foods. Food manufacturers are marketing spice-based blends for immunity enhancement, digestion support, and metabolic health. This trend gained momentum following heightened global health awareness, encouraging sustained demand for certified organic variants perceived as safer and more nutritionally intact.

Digital Traceability and Ethical Sourcing

Transparency has become a defining trend within the organic spices industry. Buyers increasingly demand proof of origin, ethical farming practices, and pesticide-free cultivation. Companies are investing in blockchain-enabled tracking systems, QR-code packaging, and farm-level certification monitoring. Ethical sourcing initiatives that ensure farmer welfare and fair pricing are strengthening brand differentiation, particularly among premium European and North American consumers. These developments are improving trust while reducing fraud risks within organic labeling systems.

What are the key drivers in the organic spices market?

Growing Clean-Label Food Consumption

The rapid expansion of clean-label food products is a major growth driver. Consumers increasingly scrutinize ingredient lists, favoring recognizable and naturally produced inputs. Organic spices align with this preference by eliminating synthetic pesticides, fertilizers, and additives. Major packaged food manufacturers are reformulating products to meet organic certification standards, significantly increasing industrial demand.

Expansion of Organic Farming Ecosystems

Government-backed agricultural programs promoting sustainable cultivation have accelerated organic spice production. Countries such as India and Sri Lanka are expanding certified organic acreage through subsidies, training programs, and export incentives. Improved farmer cooperatives and certification accessibility are reducing entry barriers, strengthening global supply availability.

Rising Demand from Premium Retail and E-commerce

The growth of online grocery platforms and specialty organic retailers has expanded consumer access to certified spices. Direct-to-consumer brands are leveraging digital marketing to promote origin stories and sustainability credentials, driving higher-value sales and expanding margins across premium product categories.

What are the restraints for the global market?

High Certification and Compliance Costs

Organic certification requires rigorous auditing, documentation, and transition periods for farms shifting from conventional cultivation. These costs increase product prices and create barriers for small-scale farmers, limiting supply scalability in certain regions.

Price Sensitivity in Emerging Markets

Organic spices typically command 20–40% price premiums compared to conventional alternatives. In price-sensitive markets, consumers often prioritize affordability, slowing adoption despite rising awareness of organic benefits.

What are the key opportunities in the organic spices industry?

Expansion into Functional Foods and Nutraceuticals

The integration of organic spices into supplements, herbal extracts, and functional beverages represents a major opportunity. Turmeric curcumin extracts, ginger concentrates, and spice blends targeting immunity and digestion are attracting investment from health-focused brands. Partnerships between spice processors and nutraceutical companies are expected to accelerate innovation and revenue diversification.

Emerging Demand from Asia-Pacific Urban Markets

Rapid urbanization and rising disposable incomes across India, China, and Southeast Asia are creating new consumer bases for organic packaged foods. Domestic consumption of organic spices, previously export-driven, is expanding rapidly as middle-class consumers prioritize health and food safety.

Technology Integration in Supply Chains

Digital procurement platforms, precision agriculture tools, and AI-based crop monitoring are improving yield predictability and reducing contamination risks. Companies investing in traceability technologies can command premium pricing while strengthening long-term buyer relationships.

Product Type Insights

The global organic spices market is witnessing substantial expansion as consumers increasingly prioritize clean-label ingredients, traceable sourcing, and chemical-free agricultural practices. Among product categories, organic turmeric continues to dominate the market landscape, accounting for approximately 18.7% of the global market share in 2025. The leadership of organic turmeric is primarily driven by its strong association with health and wellness trends, particularly its widespread use in nutraceutical formulations, dietary supplements, immunity-boosting beverages, and functional food products. The growing scientific recognition of turmeric’s bioactive compound curcumin has significantly strengthened demand across pharmaceutical, herbal medicine, and preventive healthcare sectors. Additionally, increased adoption of traditional medicinal systems such as Ayurveda and herbal therapy in both developed and emerging economies has amplified global consumption patterns.Organic black pepper represents the second-largest product segment, supported by its universal culinary application across virtually all cuisines worldwide. Its consistent demand stems from both household cooking and large-scale food processing industries, where pepper functions as a foundational seasoning ingredient. Export demand remains particularly strong due to the spice’s versatility and year-round usage in packaged foods, sauces, ready meals, and snack seasonings. Furthermore, rising consumer awareness regarding pesticide residues in conventional spices is encouraging buyers to shift toward certified organic variants, strengthening long-term demand stability.Organic ginger and cinnamon segments are experiencing accelerated growth rates compared to traditional spice categories. Beverage manufacturers are increasingly incorporating organic ginger into functional drinks, herbal teas, and wellness shots targeting digestion and immunity support. Similarly, organic cinnamon is gaining traction within bakery, confectionery, and plant-based beverage industries, where manufacturers aim to enhance flavor profiles while maintaining organic certification standards. The rising popularity of natural sweetening alternatives and sugar-reduction initiatives in processed foods further supports cinnamon’s adoption.The leading driver across product types remains the convergence of wellness-oriented consumption, rising demand for functional ingredients, and expanding regulatory scrutiny around pesticide use. As consumers increasingly link diet quality with long-term health outcomes, organic spices are transitioning from niche specialty products into mainstream pantry essentials across developed and developing markets alike.

Form Insights

Based on form, powdered organic spices dominate the global market, accounting for nearly 62% of total market share in 2025. The dominance of powdered spices is primarily attributed to their convenience, extended shelf stability, uniform flavor distribution, and compatibility with industrial-scale food manufacturing processes. Powdered formats are particularly favored by packaged food producers because they integrate seamlessly into automated production systems, ensuring consistent taste profiles across large production batches. Additionally, consumers increasingly prefer powdered spices due to ease of storage, reduced preparation time, and compatibility with modern cooking practices.The growth of meal kits, ready-to-cook products, and instant food solutions has further reinforced demand for powdered organic spices. As urban lifestyles become busier, consumers gravitate toward formats that simplify cooking without compromising quality or authenticity. Powdered spices also align well with e-commerce distribution due to lightweight packaging and longer shelf life, reducing logistical complexities for online retailers.Whole organic spices continue to maintain strong relevance, particularly within traditional culinary cultures and premium gastronomy segments. Professional chefs and culinary enthusiasts often prefer whole spices for their superior aroma retention and freshness, grinding them immediately before use to achieve enhanced flavor intensity. Premium restaurants and specialty foodservice providers increasingly highlight whole organic spices as part of authenticity-driven dining experiences, contributing to steady demand.Crushed and granulated spice formats are expanding within foodservice and industrial seasoning operations where controlled flavor dispersion and texture consistency are essential. Snack manufacturers, quick-service restaurant chains, and seasoning processors rely on these formats to achieve standardized flavor coating and efficient blending during production. The leading growth driver across forms is the increasing industrial adoption of organic ingredients combined with consumer demand for convenience-oriented culinary solutions that maintain natural integrity.

Distribution Channel Insights

Distribution dynamics within the organic spices market reflect evolving consumer purchasing behaviors and retail transformation worldwide. Supermarkets and hypermarkets collectively account for approximately 41% of global market revenue, maintaining their leadership due to consumer trust, product variety, and availability of certified organic product ranges under one roof. Large retail chains increasingly dedicate shelf space to organic and natural food categories, supported by private-label organic spice offerings that improve price accessibility while maintaining certification standards.Retail expansion strategies emphasizing transparency, certification labeling, and traceability information are strengthening consumer confidence in organic spice purchases. In-store promotions, sampling initiatives, and health-focused marketing campaigns further encourage trial and repeat purchases. The organized retail environment also enables effective comparison between conventional and organic alternatives, accelerating conversion rates toward organic products.Online retail represents the fastest-growing distribution channel, driven by digital grocery adoption, subscription-based purchasing models, and direct-to-consumer organic brands. E-commerce platforms allow consumers to access niche organic spice varieties that may not be available in physical stores, expanding product discovery opportunities. The convenience of doorstep delivery, coupled with increasing smartphone penetration and digital payment adoption, has significantly accelerated online sales growth. Brands are increasingly investing in digital storytelling, farm-to-table transparency, and sustainability messaging to build consumer loyalty through online platforms.Specialty organic stores continue to play an influential role in premium urban markets where consumers actively seek curated, ethically sourced, and high-quality products. These stores often provide educational engagement around organic farming practices and product origins, reinforcing consumer trust and willingness to pay premium prices. The leading driver across distribution channels is the global shift toward omnichannel retail strategies, allowing consumers to seamlessly purchase organic spices through both physical and digital environments.

End-Use Industry Insights

The household retail segment remains the largest end-use category, accounting for approximately 46% of global demand. Growth within this segment is driven by increasing home cooking activities, heightened health awareness, and the growing perception of spices as functional wellness ingredients rather than simple flavor enhancers. Consumers are increasingly incorporating organic spices into daily diets as part of preventive health practices, supporting sustained demand growth.The food processing industry represents the fastest-growing end-use segment as packaged food manufacturers integrate organic ingredients to meet certification requirements and respond to clean-label trends. Organic ready meals, snacks, sauces, baby foods, and plant-based products increasingly rely on certified organic spices to maintain product integrity and regulatory compliance. Large food companies are reformulating existing product lines using organic inputs to capture premium market segments and improve brand positioning.Nutraceutical and herbal medicine applications are expanding at double-digit growth rates globally. Organic spices such as turmeric, ginger, cinnamon, and black pepper are widely used in capsules, extracts, herbal supplements, and functional powders targeting immunity, digestion, and metabolic health. The integration of traditional herbal knowledge with modern scientific validation is accelerating adoption across pharmaceutical and wellness industries.Foodservice establishments, including restaurants, cafés, and catering services, are also increasing their use of organic spices to align with sustainability commitments and consumer expectations for natural ingredients. The leading driver across end-use industries is the transformation of spices from culinary commodities into health-oriented functional ingredients supporting broader wellness ecosystems.

| By Product Type | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global organic spices market, accounting for approximately 39% of global demand in 2025. The region’s dominance is supported by favorable agro-climatic conditions, long-standing spice cultivation traditions, and expanding organic farming initiatives. India remains the primary production and export hub due to its diverse climatic zones suitable for turmeric, pepper, ginger, and chili cultivation. Government-led organic certification programs, farmer training initiatives, and export incentives are encouraging producers to transition from conventional farming methods to organic practices.Rising domestic consumption across Asia-Pacific further strengthens regional growth. Increasing middle-class populations, urbanization, and growing awareness regarding food safety are encouraging consumers to shift toward pesticide-free food products. China is witnessing expanding demand driven by concerns over food contamination and increasing adoption of premium imported organic products. Japan and Australia function as high-value import markets characterized by strict quality standards and strong consumer willingness to pay premium prices for certified organic goods.The leading regional growth drivers include expanding export opportunities, supportive agricultural policies, increasing health consciousness, and rapid growth of functional food and herbal medicine industries rooted in traditional dietary practices.

North America

North America accounts for nearly 26% of the global organic spices market, led primarily by the United States, where organic food penetration continues to expand across mainstream retail channels. Consumers in the region demonstrate strong purchasing power and growing preference for clean-label products free from synthetic additives and pesticides. Retailers are significantly expanding organic private-label portfolios, improving affordability and accessibility.The region benefits from highly developed supply chains, advanced packaging technologies, and strong certification frameworks that enhance consumer confidence. The rapid growth of plant-based diets, international cuisine adoption, and functional wellness trends further drives organic spice consumption. Canada is experiencing increasing integration of organic spices within packaged food manufacturing and specialty retail segments, supported by sustainability-focused consumer behavior.Key regional growth drivers include premiumization trends, rising health awareness, expansion of organic packaged foods, and strong retail infrastructure enabling widespread distribution.

Europe

Europe represents a mature yet rapidly evolving consumption hub for organic spices, with strong demand across Germany, the United Kingdom, France, and the Netherlands. Strict regulatory frameworks promoting organic agriculture, environmental sustainability, and traceability standards significantly influence market expansion. European consumers exhibit high awareness regarding ethical sourcing, biodiversity preservation, and carbon footprint reduction, making organic certification a critical purchasing factor.The region’s well-established organic food culture supports consistent demand across retail and foodservice industries. Manufacturers increasingly incorporate organic spices into premium ready meals, gourmet sauces, and health-oriented food products. Additionally, sustainability initiatives under regional agricultural policies encourage imports of certified organic spices from developing economies, strengthening international trade flows.The leading growth drivers in Europe include stringent regulatory support, environmentally conscious consumption patterns, expanding vegan and organic food sectors, and strong institutional backing for sustainable agriculture.

Middle East & Africa

The Middle East and Africa region presents a dual-market structure combining high-value consumption hubs with emerging production centers. The Middle East is rapidly evolving into a premium import market driven by luxury hospitality industries and expanding gourmet food cultures in countries such as the United Arab Emirates and Saudi Arabia. Hotels, fine-dining establishments, and premium retailers increasingly source organic spices to meet international culinary standards and health-conscious consumer expectations.Africa contributes primarily through agricultural production, with countries such as Madagascar and Tanzania expanding organic spice cultivation supported by international development programs and export partnerships. Organic vanilla, pepper, and specialty spices from the region are gaining global recognition for quality and sustainability credentials.Regional growth drivers include tourism-driven foodservice demand, export-oriented agricultural investments, improving certification infrastructure, and rising global demand for ethically sourced spices.

Latin America

Latin America is experiencing steady growth in the organic spices market, led by Brazil and Mexico, where expanding middle-class populations and rising awareness of organic food benefits are strengthening domestic consumption. Improvements in modern retail infrastructure and increasing penetration of supermarkets and online grocery platforms are enhancing product accessibility across urban centers.The region is also emerging as a production base for certain organic spices due to favorable climatic conditions and growing participation in sustainable agriculture initiatives. Export opportunities to North America and Europe are encouraging farmers to adopt organic cultivation methods supported by certification programs and international trade partnerships.The primary drivers of regional growth include expanding retail modernization, increasing consumer health awareness, export diversification strategies, and government support for sustainable agricultural development.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Organic Spices Market

- McCormick & Company, Inc.

- Olam Group Limited

- Frontier Co-op

- Organic Spices Inc.

- Everest Spices

- MDH Spices

- Simply Organic (Frontier Co-op brand)

- SunOpta Inc.

- Dabur India Ltd.

- Kotányi GmbH

- Rapid Organic Pvt. Ltd.

- Naturevibe Botanicals

- Spicely Organics

- Curio Spice Company

- Pacific Spice Company