Organic Rice Protein Market Size

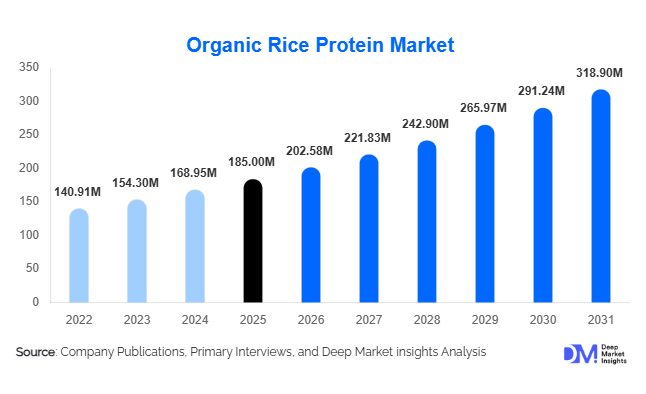

According to Deep Market Insights, the global organic rice protein market size was valued at USD 185 million in 2025 and is projected to grow from USD 202.58 million in 2026 to reach USD 318.90 million by 2031, expanding at a CAGR of 9.5% during the forecast period (2025–2031). The organic rice protein market growth is primarily driven by rising adoption of plant-based diets, increasing demand for clean-label and allergen-free protein ingredients, and expanding applications in sports nutrition, dairy alternatives, and meat substitutes.

Key Market Insights

- Organic rice protein isolate dominates the product landscape, accounting for nearly 48% of the global market in 2025 due to its high protein concentration and suitability for sports nutrition formulations.

- Powder form holds over 85% market share, driven by ease of blending, longer shelf life, and compatibility with dry food and supplement applications.

- North America leads with 38% market share, supported by strong vegan adoption and premium supplement demand in the United States.

- Asia-Pacific is the fastest-growing region, projected to expand at over 11% CAGR, fueled by production expansion in China and India.

- Food & beverages account for 55% of demand, particularly in meat alternatives and dairy-free beverages.

- The top five companies control approximately 52% of the global market share, reflecting moderate consolidation and strong competition in premium certified segments.

What are the latest trends in the organic rice protein market?

Clean-Label and Allergen-Free Positioning

Consumers are increasingly demanding products free from soy, dairy, gluten, and artificial additives. Organic rice protein aligns with this trend due to its hypoallergenic profile and compatibility with vegan and non-GMO claims. Manufacturers are promoting minimal ingredient lists and transparent sourcing practices to appeal to health-conscious buyers. Retail brands are leveraging USDA Organic and EU Organic certifications to command price premiums of 15–25% compared to conventional protein variants. The clean-label movement is particularly strong in North America and Europe, influencing procurement strategies among food processors.

Technological Improvements in Solubility and Texture

Processing advancements such as enzymatic hydrolysis and spray-drying optimization are improving the solubility, taste neutrality, and blending capacity of organic rice protein. These innovations enhance its application in ready-to-drink beverages and high-protein snacks. Manufacturers are also developing protein blends combining rice and pea protein to improve amino acid profiles, expanding their competitiveness against soy-based proteins.

What are the key drivers in the organic rice protein market?

Expansion of the Plant-Based Food Industry

The rapid growth of plant-based meat and dairy alternatives is a primary growth driver. Organic rice protein’s neutral taste and binding properties make it suitable for burgers, sausages, and dairy-free beverages. As global plant-based food sales exceed USD 45 billion and continue to grow at double-digit rates, ingredient demand is rising correspondingly.

Growth in Sports and Functional Nutrition

The global sports nutrition industry is expanding at over 8% annually, boosting demand for high-protein, plant-based formulations. Organic rice protein isolate, with ≥80% protein content, is increasingly adopted in protein powders and performance supplements. Rising gym memberships and wellness trends in urban markets are accelerating consumption.

What are the restraints for the global market?

High Raw Material and Certification Costs

Organic brown rice procurement costs are 20–30% higher than conventional rice due to certification requirements and limited acreage. These higher input costs impact profit margins and retail pricing competitiveness.

Competition from Pea and Soy Protein

Pea protein remains more cost-effective and widely available, posing substitution risks in meat analogues and beverages. Continuous innovation is necessary to maintain differentiation.

What are the key opportunities in the organic rice protein industry?

Emerging Markets Expansion

Asia-Pacific and Middle Eastern markets are witnessing rising disposable incomes and fitness awareness. Export-driven demand from China and India offers supply chain advantages. Establishing localized processing facilities can reduce logistics costs and improve margins.

Pet Food and Clinical Nutrition Applications

Hypoallergenic properties create opportunities in premium pet food and specialized clinical nutrition products. As global pet food markets expand steadily, plant-based formulations are gaining visibility among premium consumers.

Product Type Insights

Organic rice protein isolate leads the global market, accounting for approximately 48% of total revenue in 2025. The dominance of isolates is primarily driven by their high protein concentration (≥80%), superior digestibility, and suitability for premium sports nutrition and functional food formulations. With the global sports nutrition industry expanding at over 8% annually, manufacturers increasingly prefer isolates for protein powders, ready-to-drink beverages, and high-protein snack bars. Additionally, isolates offer improved solubility and neutral taste profiles compared to concentrates, making them highly compatible with dairy alternatives and fortified beverages. Ongoing advancements in enzymatic extraction technologies have further enhanced purity levels and amino acid balance, reinforcing isolate leadership.

Organic rice protein concentrates hold a significant secondary share, particularly in cost-sensitive bakery, snack fortification, and cereal applications. Their moderate protein content (60–80%) makes them suitable for texture enhancement and nutritional fortification at lower price points. Hydrolysates are gaining traction in infant nutrition, geriatric diets, and clinical formulations due to improved absorption and hypoallergenic properties. Meanwhile, texturized organic rice protein is expanding within plant-based meat manufacturing, supported by growing demand for vegan protein sources in burger patties, sausages, and ready-to-cook meals. The increasing penetration of plant-based meat products globally is expected to accelerate demand for texturized variants over the forecast period.

Application Insights

Food & beverages dominate the market with nearly 55% share in 2025, primarily driven by rising demand for plant-based meat and dairy alternatives. The global shift toward flexitarian diets and lactose-free consumption patterns is boosting ingredient substitution in mainstream food processing. Organic rice protein’s neutral taste, allergen-free positioning, and compatibility with clean-label claims make it particularly attractive for dairy-free beverages, protein-fortified cereals, and plant-based meat products.

Dietary supplements account for approximately 30% of total demand, supported by strong growth in sports and performance nutrition. Increasing gym participation, wellness awareness, and the expansion of vegan protein powders have accelerated demand for organic-certified protein ingredients. Meanwhile, animal nutrition and cosmetics collectively represent about 15% of the market, with steady growth in premium pet food formulations and plant-based cosmetic ingredients. Hypoallergenic properties make organic rice protein suitable for sensitive-skin formulations and specialty pet diets.

Distribution Channel Insights

Direct industrial sales dominate the distribution landscape, contributing nearly 70% of total volume in 2025. Bulk procurement by food and beverage manufacturers ensures stable long-term supply contracts and predictable revenue streams for producers. Large-scale ingredient buyers prioritize vertically integrated suppliers capable of providing certified organic, traceable, and non-GMO compliant products.

Ingredient distributors remain critical in regional supply chains, particularly in Europe and Asia-Pacific, where fragmented manufacturing bases rely on established distribution networks. Online retail channels are expanding in the branded supplement segment, especially in North America and Europe, as direct-to-consumer protein powder sales gain momentum through e-commerce platforms and subscription-based wellness models.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America accounts for approximately 38% of the global organic rice protein market in 2025, with the United States representing over 85% of regional consumption. Regional growth is driven by high vegan and flexitarian adoption rates, strong demand for sports nutrition supplements, and widespread clean-label awareness. The presence of established organic certification frameworks, such as USDA Organic, enhances consumer confidence and supports premium pricing. Additionally, the region benefits from a well-developed e-commerce infrastructure, enablingthe rapid growth of plant-based supplement brands. Continuous product innovation in protein blends and ready-to-drink beverages further strengthens demand across the U.S. and Canada.

Europe

Europe holds around 29% market share, led by Germany, France, and the United Kingdom. Growth in this region is primarily driven by stringent labeling regulations, high consumer awareness of sustainable sourcing, and strong adoption of organic-certified food ingredients. The European Green Deal and sustainability initiatives encourage plant-based protein substitution in food manufacturing. Additionally, the region’s mature dairy alternative market and expanding vegan population contribute significantly to ingredient demand. Import reliance on Asian suppliers for organic rice protein is also shaping trade flows within the region.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of the global share and is the fastest-growing region with over 11% CAGR. China and India serve as major production hubs due to abundant rice cultivation and lower processing costs, making the region a key exporter to North America and Europe. Rising disposable incomes, expanding nutraceutical industries, and increasing fitness awareness are driving domestic consumption. Government support for organic agriculture and export-oriented manufacturing further strengthens regional competitiveness.

Latin America

Latin America represents about 6% of the global market, with Brazil and Mexico leading regional demand. Growth drivers include rising sports nutrition awareness, urbanization, and increasing penetration of plant-based diets. While the region remains import-dependent for certified organic protein ingredients, local supplement brands are expanding portfolios to include vegan and allergen-free products, gradually boosting regional consumption.

Middle East & Africa

The Middle East & Africa region holds approximately 5% market share and demonstrates steady growth. The UAE and South Africa are key markets, driven by premium fitness trends, high disposable income segments, and expanding retail infrastructure for health products. In the Middle East, growing demand for halal-certified and clean-label protein ingredients supports organic rice protein adoption. Although overall consumption remains modest compared to developed regions, rising awareness of plant-based nutrition is expected to drive gradual expansion during the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Organic Rice Protein Market

- Axiom Foods

- RiceBran Technologies

- Golden Grain Group

- Shafi Gluco Chem

- Bioway (Xi’an) Organic Ingredients

- Top Health Ingredients

- AIDP

- The Green Labs LLC

- ETChem

- Wuxi Jinnong Biotechnology

- Nutribiotic

- Growing Naturals

- Pure Food Company

- Z-COMPANY

- Beneo