Organic Foods Market Size

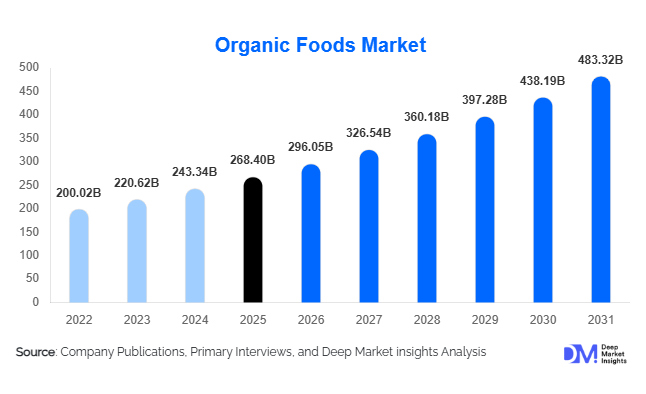

According to Deep Market Insights, the global organic foods market size was valued at USD 268.4 billion in 2025 and is projected to grow from USD 296.05 billion in 2026 to reach USD 483.32 billion by 2031, expanding at a CAGR of 10.3% during the forecast period (2026–2031). The organic foods market growth is driven by rising consumer awareness regarding health and nutrition, increasing preference for chemical-free agricultural products, and growing environmental concerns associated with conventional farming practices. Rapid expansion of organized retail, strong growth in online grocery platforms, and government-backed organic certification programs are further accelerating global adoption.

Key Market Insights

- Health-conscious consumption trends are driving rapid adoption of organic fruits, dairy, packaged foods, and plant-based alternatives globally.

- Europe and North America collectively account for over 65% of global demand, supported by strong certification frameworks and premium consumer spending.

- Asia-Pacific is the fastest-growing region, led by China and India’s expanding middle-class population and domestic organic farming initiatives.

- E-commerce grocery platforms are reshaping distribution channels, improving accessibility of organic products beyond urban centers.

- Private-label organic brands launched by retailers are increasing affordability and widening consumer penetration.

- Sustainability and traceability technologies, including blockchain-enabled supply chains and eco-labeling, are strengthening consumer trust.

What are the latest trends in the organic foods market?

Rise of Plant-Based and Functional Organic Foods

Organic food consumption is increasingly merging with plant-based nutrition and functional wellness trends. Consumers are seeking products that deliver immunity benefits, digestive health support, and clean-label ingredients alongside organic certification. Organic plant proteins, dairy alternatives, probiotic beverages, and fortified cereals are witnessing strong growth across developed economies. Food manufacturers are investing in innovation focused on nutrient density, minimal processing, and allergen-free formulations. This trend is expanding organic food consumption beyond traditional fresh produce into value-added packaged categories, improving margins and strengthening brand differentiation.

Digital Traceability and Transparent Supply Chains

Transparency has become a critical purchasing factor in the organic foods market. Companies are adopting blockchain tracking, QR-code labeling, and farm-to-table traceability systems that allow consumers to verify origin, farming practices, and certifications. Retailers are increasingly highlighting sustainability scores and carbon footprints alongside organic labels. These digital integrations are improving consumer confidence while reducing fraud risks associated with mislabeling. As regulatory scrutiny rises globally, technology-driven traceability is expected to become a standard competitive requirement.

What are the key drivers in the organic foods market?

Growing Health Awareness and Lifestyle Diseases

The increase in obesity, diabetes, and cardiovascular diseases has significantly influenced dietary behavior worldwide. Consumers increasingly perceive organic foods as safer due to the absence of synthetic pesticides, antibiotics, and genetically modified inputs. Healthcare professionals and wellness influencers are promoting clean eating habits, accelerating adoption particularly among urban populations. This health-driven demand continues to expand across dairy, baby food, and ready-to-eat organic products.

Government Support and Organic Certification Programs

Public policies promoting sustainable agriculture are playing a vital role in market expansion. Subsidies for organic farming, certification assistance programs, and export incentives are encouraging farmers to transition away from conventional agriculture. Initiatives such as organic farming missions in India, EU organic action plans, and regenerative agriculture funding in North America are increasing production capacity and improving supply stability.

Expansion of Organized Retail and Online Grocery

Modern retail chains and digital grocery platforms have dramatically improved product accessibility. Supermarkets are dedicating shelf space to organic private labels, while online platforms enable subscription-based delivery models for fresh organic produce. Convenience and wider product availability are converting occasional buyers into repeat consumers, strengthening long-term demand growth.

What are the restraints for the global market?

Premium Pricing and Cost Sensitivity

Organic foods remain priced 20–60% higher than conventional alternatives due to lower yields, certification costs, and supply chain complexities. Price sensitivity in emerging markets restricts widespread adoption, particularly among middle-income consumers.

Supply Chain and Certification Challenges

Limited availability of certified farmland, inconsistent regulatory standards across countries, and risks of fraudulent labeling create operational challenges. Maintaining consistent quality and supply volumes remains a key barrier for large-scale market expansion.

What are the key opportunities in the organic foods industry?

Expansion into Emerging Markets

Asia-Pacific, Latin America, and Middle Eastern markets present strong untapped potential. Rising disposable incomes and urbanization are enabling consumers to shift toward premium food categories. Governments are investing heavily in domestic organic agriculture to reduce import dependency. Retail expansion into tier-2 and tier-3 cities further strengthens growth prospects.

Integration of Technology in Organic Farming

Precision agriculture, AI-driven soil monitoring, and biological crop protection solutions are improving productivity while maintaining organic standards. Technology adoption reduces yield gaps between conventional and organic farming, improving profitability for producers and stabilizing pricing for consumers.

Growth of Organic Processed and Convenience Foods

Busy lifestyles are driving demand for organic ready meals, snacks, and frozen foods. Manufacturers expanding into convenient organic formats can capture higher margins while attracting younger consumers seeking healthy yet time-efficient food solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 268.40 Billion |

| Market Size in 2026 | USD 296.05 Billion |

| Market Size in 2031 | USD 483.32 Billion |

| CAGR | 10.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Organic fruits and vegetables continue to dominate the global organic foods market, accounting for approximately 34% of total market revenue in 2025. The leadership of this segment is primarily supported by its role as a staple category within daily diets, high purchase frequency, and expanding availability across both organized retail and online grocery platforms. Increasing consumer preference for pesticide-free produce, combined with growing awareness regarding food safety and nutritional quality, has strengthened demand across developed and emerging economies. Retailers are further expanding fresh organic assortments and private-label offerings, improving affordability and accessibility, which reinforces the segment’s leading position.Organic dairy products represent nearly 18% of the market, driven by rising consumer concerns surrounding antibiotic usage, hormone treatments, and animal welfare practices in conventional dairy farming. Demand for organic milk, yogurt, and cheese is expanding steadily as health-conscious consumers prioritize clean-label and minimally processed nutrition. Growth is also supported by increasing adoption of organic dairy among families with children and premiumization trends across developed markets.Organic packaged foods account for approximately 16% of global revenue, supported by continuous innovation in ready-to-eat meals, snacks, cereals, and functional food products. Manufacturers are increasingly combining organic certification with attributes such as gluten-free, vegan, and non-GMO positioning, appealing to convenience-oriented urban consumers seeking healthier alternatives without sacrificing convenience.Organic beverages contribute close to 11% of the market, led by expanding consumption of organic juices, plant-based drinks, and functional beverages. Rising demand for natural hydration solutions, clean ingredient labeling, and sugar reduction trends are encouraging beverage companies to introduce organic variants across multiple product categories.Organic meat, poultry, and seafood collectively hold around 13% share, supported by growing consumer awareness regarding ethical sourcing, animal welfare standards, and traceability in protein supply chains. Although price premiums remain relatively high, rising disposable incomes and transparency initiatives are encouraging gradual adoption, particularly in North America and Europe.Organic baby food represents approximately 8% of the market and is emerging as one of the fastest-growing categories. Increasing parental awareness about early childhood nutrition, concerns regarding chemical residues, and preference for preservative-free formulations are accelerating demand. Expansion of premium infant nutrition brands and wider retail distribution is further strengthening growth momentum in this segment.

Application Insights

Household consumption dominates organic food applications, contributing nearly 72% of total global demand. The segment’s leadership is driven by rising health consciousness, increasing incidence of lifestyle-related diseases, and growing consumer interest in home-prepared meals made from natural ingredients. The expansion of retail accessibility, subscription grocery services, and greater product variety has enabled organic food adoption to transition from niche consumption toward mainstream household purchasing behavior.Foodservice applications account for approximately 18% of market demand, supported by restaurants, cafés, and premium dining establishments incorporating organic ingredients to differentiate menus and attract health-focused consumers. The growth of farm-to-table concepts, sustainable sourcing initiatives, and premium dining experiences is encouraging foodservice operators to integrate organic offerings as part of brand positioning strategies.Institutional demand contributes nearly 10% of the market, expanding steadily due to nutrition-focused procurement policies across schools, hospitals, and corporate cafeterias. Governments and organizations are increasingly prioritizing healthier meal programs, which is supporting long-term adoption of certified organic food products within institutional supply chains.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 46% of global organic food sales. The leading position of this segment is driven by extensive product visibility, wide assortment availability, competitive pricing through private-label organic ranges, and consumer preference for one-stop shopping experiences. Large retail chains are investing in dedicated organic sections and sustainability branding, which further strengthens consumer trust and purchase frequency.Online retail represents nearly 22% of the market and is the fastest-expanding distribution channel. Growth is supported by increasing digital adoption, convenience-driven purchasing behavior, and subscription-based grocery delivery models that enable regular organic product consumption. Improved cold-chain logistics and direct-to-consumer strategies are also enhancing product freshness and accessibility.Specialty organic stores hold around 20% market share, benefiting from strong consumer trust, product authenticity, and knowledgeable in-store guidance. These outlets often emphasize local sourcing and premium product positioning, attracting loyal health-conscious customer bases.Convenience stores and direct farm sales together account for approximately 12% of distribution. Growth in this segment is supported by rising interest in locally sourced food, farmers’ markets, and community-supported agriculture models that promote transparency between producers and consumers.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Foods Market Segmentations

By Product Type

- Organic Fruits & Vegetables

- Organic Dairy Products

- Organic Packaged Foods

- Organic Beverages

- Organic Meat, Poultry & Seafood

- Organic Baby Food

By Application

- Household Consumption

- Foodservice & Restaurants

- Institutional Applications

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce

- Specialty Organic Stores

- Convenience Stores

- Direct Farm-to-Consumer Sales

Regional Insights

North America

North America held approximately 38% of the global organic foods market in 2025, led primarily by the United States as the largest single-country contributor. Regional growth is supported by high consumer awareness regarding health and sustainability, well-established organic certification frameworks, and strong penetration of organic products across mainstream retail channels. Rising demand for clean-label foods, expansion of private-label organic offerings, and increasing adoption of organic diets among younger consumers continue to drive market expansion. Canada is strengthening regional supply integration through expansion of certified organic farmland and cross-border trade, enhancing product availability and supply chain stability across the region.

Europe

Europe accounted for nearly 31% of global market share, with Germany, France, Italy, and the United Kingdom serving as key demand centers. Regional growth is strongly influenced by supportive European Union agricultural policies promoting sustainable farming practices, reduced chemical usage, and environmental stewardship. High consumer preference for ethically produced and environmentally responsible food products, combined with government incentives for organic farming conversion, continues to expand production capacity. Mature retail infrastructure and strong adoption of organic private labels further reinforce market growth across Western and Northern Europe.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, expanding middle-class populations, and rising disposable incomes across China, India, Japan, and Australia. Increasing food safety concerns and growing awareness of chemical-free agriculture are accelerating consumer adoption of organic products. China’s expanding premium consumer base is driving imports of organic packaged foods, while India is strengthening domestic supply through national organic farming missions, certification programs, and export-focused agricultural initiatives. Growth of e-commerce grocery platforms and modern retail formats is further improving accessibility throughout the region.

Latin America

Latin America is emerging as both a major production hub and a developing consumption market, led by Brazil, Mexico, and Argentina. Regional growth is supported by favorable climatic conditions for organic agriculture and strong export demand for organic coffee, fruits, cocoa, and sugar products. Increasing participation of small-scale farmers in certified organic farming and rising international trade partnerships are strengthening regional supply chains. Domestic consumption is gradually expanding as urban populations grow and awareness of health and sustainability improves.

Middle East & Africa

The Middle East & Africa region is experiencing steady growth, led by the United Arab Emirates and Saudi Arabia, where high dependence on food imports and expanding premium retail infrastructure are supporting demand for organic products. Rising expatriate populations, higher disposable incomes, and increasing focus on health-oriented lifestyles are encouraging adoption of premium organic food categories. In Africa, South Africa represents the largest organic consumption hub, supported by improving retail networks, expanding local production, and growing consumer awareness regarding sustainable agriculture and nutritional quality.

Key Players in the Organic Foods Market

- Danone S.A.

- Nestlé S.A.

- General Mills Inc.

- Hain Celestial Group

- Whole Foods Market

- United Natural Foods Inc.

- Amy’s Kitchen

- Organic Valley

- Arla Foods

- Nature’s Path Foods

- Sprouts Farmers Market

- Eden Foods

- SunOpta Inc.

- Clif Bar & Company

- Fonterra Co-operative Group