Organic Coconut Water Market Size

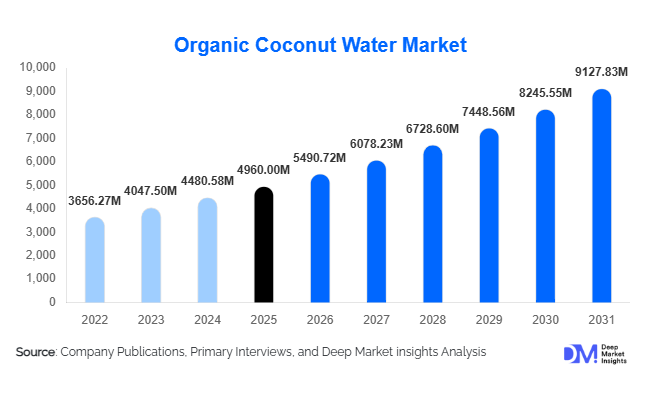

According to Deep Market Insights, the global organic coconut water market size was valued at USD 4,960 million in 2025 and is projected to grow from USD 5,490.72 million in 2026 to reach USD 9,127.83 million by 2031, expanding at a CAGR of 10.7% during the forecast period (2026–2031). The organic coconut water market growth is primarily driven by increasing consumer preference for clean-label beverages, rising demand for natural hydration alternatives, and the global shift toward plant-based functional drinks.

Key Market Insights

- Rising demand for clean-label and organic beverages is accelerating adoption across developed and emerging markets.

- Pure organic coconut water dominates product demand, driven by minimal processing and natural electrolyte content.

- North America leads global consumption, supported by strong health and wellness trends.

- Asia-Pacific is the fastest-growing region, driven by production advantages and rising domestic demand.

- Flavored and functional variants are gaining traction among younger consumers seeking taste and added benefits.

- E-commerce and direct-to-consumer channels are reshaping distribution and improving brand reach.

What are the latest trends in the organic coconut water market?

Shift Toward Functional and Fortified Beverages

Organic coconut water is increasingly being positioned as a functional beverage with added health benefits. Manufacturers are introducing variants enriched with vitamins, minerals, probiotics, and adaptogens to cater to wellness-focused consumers. These innovations are helping brands differentiate in a competitive market while capturing premium pricing. Functional positioning is particularly strong among fitness enthusiasts and urban consumers seeking natural energy and hydration solutions.

Sustainable Packaging and Ethical Sourcing

Sustainability is becoming a core focus in the organic coconut water market. Companies are adopting eco-friendly packaging solutions such as recyclable tetra packs, biodegradable materials, and reduced plastic usage. Ethical sourcing practices, including fair-trade coconut farming and carbon-neutral supply chains, are also gaining importance. These initiatives not only improve brand perception but also align with evolving regulatory and consumer expectations around environmental responsibility.

What are the key drivers in the organic coconut water market?

Growing Health and Wellness Awareness

The increasing global focus on health and wellness is a major driver of market growth. Consumers are actively shifting away from sugary and artificially flavored beverages toward natural alternatives. Organic coconut water, rich in electrolytes and low in calories, is widely perceived as a healthier hydration option, driving its adoption across diverse demographic groups.

Expansion of Retail and Digital Channels

The growth of organized retail and e-commerce platforms is significantly boosting product accessibility. Supermarkets and hypermarkets provide high visibility, while online platforms enable consumers to explore a wider range of products and brands. Subscription-based models and direct-to-consumer strategies are further enhancing customer engagement and repeat purchases.

What are the restraints for the global market?

High Production and Certification Costs

Organic coconut water production involves higher costs due to stringent organic farming practices and certification requirements. These costs are often passed on to consumers, making the product relatively expensive compared to conventional beverages. This limits adoption in price-sensitive markets and poses a challenge for mass-market penetration.

Supply Chain and Raw Material Volatility

The market is highly dependent on coconut production, which is susceptible to climate variability, natural disasters, and seasonal fluctuations. Supply disruptions can lead to price volatility and impact profitability for manufacturers, making supply chain management a critical challenge.

What are the key opportunities in the organic coconut water industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, the Middle East, and Africa present significant growth opportunities. Rising disposable incomes, urbanization, and increasing awareness of organic products are driving demand in these regions. Local production capabilities further enhance market potential by reducing costs and improving supply chain efficiency.

Innovation in Product Variants

The introduction of flavored, sparkling, and fortified organic coconut water is expanding the consumer base. These innovations cater to evolving taste preferences and provide additional health benefits, enabling brands to tap into new market segments and enhance profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4960.00 Million |

| Market Size in 2026 | USD 5490.72 Million |

| Market Size in 2031 | USD 9127.83 Million |

| CAGR | 10.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global organic coconut water market is primarily segmented into pure organic coconut water, flavored organic coconut water, fortified organic coconut water, and sparkling organic coconut water, each catering to distinct consumer needs shaped by evolving health consciousness, taste preferences, and functional beverage demand. Among these, pure organic coconut water continues to dominate the global market, accounting for approximately 42% of the total market share in 2025. This dominance is strongly supported by rising consumer inclination toward clean-label beverages, minimal processing, and naturally hydrating drinks that retain electrolytes without artificial additives or sweeteners. The leading growth driver for this segment is the accelerating shift toward natural hydration solutions, especially among urban consumers who are increasingly replacing sugary soft drinks with plant-based, nutrient-rich alternatives. Additionally, the strong perception of coconut water as a “natural isotonic drink” enhances its adoption among fitness-conscious individuals and wellness-oriented populations across developed and emerging economies.Flavored organic coconut water is experiencing significant expansion, driven by innovation in taste profiles and the increasing demand for variety among younger consumers. This segment benefits from the key growth driver of experiential consumption, where consumers seek beverages that not only provide hydration but also deliver enjoyable sensory experiences. Flavors such as mango, pineapple, passion fruit, and mixed berry are gaining traction, particularly in urban retail environments and quick-service beverage outlets. Meanwhile, fortified organic coconut water enriched with vitamins, minerals, antioxidants, and functional ingredients is emerging as a high-value segment. Its primary growth driver is the rising demand for functional beverages that support immunity, energy, and recovery, especially in post-pandemic health-conscious populations.Sparkling organic coconut water, although still a niche category, is gradually establishing itself as a premium alternative to carbonated soft drinks. Its growth is primarily driven by the global trend of alcohol-free and low-sugar lifestyle beverages, particularly among millennials seeking healthier substitutes for soda and alcoholic drinks. The combination of carbonation with natural coconut water positions this segment uniquely within the premium wellness beverage category, and it is expected to gain stronger traction in urban retail and hospitality channels.

Application Insights

In terms of application, direct consumption remains the dominant segment, accounting for approximately 55% of total global demand. This leadership is largely driven by the convenience factor, increasing on-the-go consumption habits, and strong consumer trust in organic coconut water as a ready-to-drink natural hydration solution. The primary growth driver for this segment is the expansion of health-driven beverage substitution behavior, where consumers actively replace carbonated drinks, packaged juices, and energy drinks with healthier alternatives. The widespread availability of packaged organic coconut water across supermarkets, convenience stores, and online platforms further reinforces its dominance in direct consumption.The sports and fitness nutrition application segment represents the fastest-growing category, propelled by rising global participation in fitness activities, gym memberships, yoga practices, endurance sports, and athletic training programs. The key driver supporting this segment is the increasing recognition of coconut water as a natural electrolyte replenisher, offering potassium, magnesium, and sodium balance without synthetic additives. Athletes and fitness enthusiasts are increasingly shifting toward organic hydration sources that support recovery, reduce muscle fatigue, and enhance performance, thereby accelerating demand in this segment.Additionally, the functional beverage industry is witnessing robust integration of organic coconut water into health-focused formulations. Beverage manufacturers are increasingly incorporating coconut water into smoothies, wellness drinks, detox beverages, and nutraceutical products. This segment is driven by the rapid expansion of preventive healthcare trends, where consumers prioritize immunity support, digestive wellness, and natural energy enhancement. The use of organic coconut water as a base ingredient in innovative beverage formulations is expected to further expand its industrial and commercial applications over the forecast period.

Distribution Channel Insights

The distribution landscape of the organic coconut water market is highly diversified, with supermarkets and hypermarkets holding the largest share, accounting for nearly 40% of total global sales. This dominance is primarily attributed to strong consumer trust, extensive product visibility, and the ability of large retail chains to offer multiple brands and variants under one roof. The leading growth driver for this channel is the rising penetration of organized retail infrastructure in both developed and emerging markets, along with increasing consumer preference for physically inspecting premium organic beverages before purchase.Online retail is emerging as the most dynamic and rapidly expanding distribution channel. Its growth is fueled by the increasing adoption of e-commerce platforms, digital grocery delivery services, and subscription-based beverage models. The primary driver for this segment is convenience-driven purchasing behavior, especially among younger, digitally connected consumers who prefer doorstep delivery and access to a wider product assortment. In addition, promotional pricing, product bundling, and direct-to-consumer brand strategies are significantly enhancing online sales penetration.Specialty health stores and organic retail outlets are also gaining importance, particularly in urban regions where consumers actively seek premium wellness products. The key driver for this channel is the trust associated with curated health-focused retail environments, where consumers perceive higher product authenticity and quality assurance. Direct-to-consumer channels operated by organic beverage brands are also expanding, enabling companies to strengthen brand loyalty, control pricing strategies, and improve customer engagement through personalized marketing.

Consumer Demographics Insights

Millennials and Gen Z consumers represent the largest demographic segment in the organic coconut water market, contributing approximately 48% of total global demand. This dominance is primarily driven by lifestyle shifts toward health consciousness, sustainability awareness, and preference for plant-based diets. These consumers are highly influenced by digital media, influencer marketing, and wellness trends circulating on social platforms. The leading growth driver for this segment is the increasing prioritization of preventive health and clean-label consumption patterns, where transparency, organic certification, and environmental responsibility play a critical role in purchase decisions.Health-conscious adults and fitness enthusiasts form another significant consumer base, driven by structured wellness routines, dietary discipline, and active lifestyle habits. The key driver for this segment is the integration of functional beverages into daily nutrition plans, particularly for hydration, recovery, and energy balance. Organic coconut water is increasingly viewed as a natural replacement for synthetic sports drinks, further strengthening its penetration among this demographic.Additionally, demand among aging populations is gradually increasing, supported by the product’s low-calorie nature, easy digestibility, and natural electrolyte content. The primary driver for this segment is the growing focus on age-related wellness management, including cardiovascular health, hydration maintenance, and diabetes-friendly dietary choices.

Explore more data points, trends and opportunities Download Free Sample Report

Organic Coconut Water Market Segmentations

By Product Type

- Pure Organic Coconut Water

- Organic Coconut Water From Concentrate

- Flavored Organic Coconut Water

- Fortified Organic Coconut Water

- Sparkling Organic Coconut Water

By Packaging Type

- Tetra Packs

- Glass Bottles

- Aluminum Cans

- Bulk Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Health Stores

- HoReCa

By End-Use Application

- Direct Consumption

- Sports & Fitness Nutrition

- Functional Beverages Industry

- Food Processing

- Hospitality & Catering

Regional Insights

North America

North America accounts for approximately 32% of the global organic coconut water market, with the United States leading consumption due to its highly developed health and wellness industry. The region’s growth is primarily driven by strong consumer awareness regarding clean-label products, rising demand for plant-based beverages, and widespread adoption of functional drinks among fitness enthusiasts. The expansion of organic product certification standards and premium beverage culture further strengthens market penetration. Another key driver is the robust retail and e-commerce infrastructure, which ensures wide product accessibility across urban and suburban populations. Canada also contributes significantly, with increasing organic food adoption and rising demand for sustainable beverage alternatives reinforcing steady market growth.

Europe

Europe holds around 24% of the global market share, with key contributions from Germany, the United Kingdom, and France. The region’s growth is strongly influenced by strict organic certification regulations and high consumer awareness regarding environmental sustainability. The leading driver in Europe is the strong cultural shift toward eco-friendly consumption patterns, where consumers actively prefer ethically sourced and environmentally responsible products. Additionally, increasing veganism, vegetarian diets, and reduced sugar consumption trends are accelerating demand for organic coconut water. The presence of well-established health food retail chains and premium supermarket segments further supports consistent market expansion.

Asia-Pacific

Asia-Pacific represents approximately 28% of the global market and is the fastest-growing regional market. The region’s growth is primarily driven by abundant raw material availability in countries such as India, Indonesia, Thailand, and the Philippines, which are major coconut-producing nations. Rising urbanization, increasing disposable incomes, and shifting dietary preferences are significantly boosting demand for packaged organic beverages. Government initiatives promoting organic farming practices and sustainable agriculture are further accelerating production capabilities. Additionally, the rapid expansion of e-commerce platforms and modern retail formats is improving product accessibility, making Asia-Pacific a critical growth engine for the global market.

Latin America

Latin America accounts for approximately 10% of the global market, with Brazil emerging as the leading contributor due to its strong agricultural base and favorable climatic conditions for coconut cultivation. The primary driver for regional growth is the increasing domestic consumption of natural beverages, supported by rising health awareness and urban lifestyle changes. Additionally, expanding export opportunities to North America and Europe are encouraging local producers to scale organic coconut water production. The region is also witnessing gradual growth in premium beverage consumption, particularly in metropolitan areas.

Middle East & Africa

The Middle East & Africa region holds around 6% of the global market share, with the United Arab Emirates emerging as a key consumption hub due to high demand for premium imported beverages. The growth in this region is driven by rising expatriate populations, increasing disposable incomes, and strong demand for healthy hydration alternatives in hot climatic conditions. South Africa is also witnessing steady growth, supported by increasing awareness of health and wellness trends. The expansion of luxury retail formats and hospitality-driven beverage demand further contributes to regional market development, positioning the region as an emerging niche market for organic coconut water.

Key Players in the Organic Coconut Water Market

- Vita Coco Company

- PepsiCo

- Coca-Cola Company

- Harmless Harvest

- Amy & Brian Naturals

- Taste Nirvana

- C2O Pure Coconut Water

- Goya Foods

- UFC Coconut Water

- Thai Agri Foods

- Celebes Coconut Corporation

- Edward & Sons Trading

- Green Coco Europe

- FOCO

- Coco Libre