Organic Chocolate Flavor Ingredients Market Size

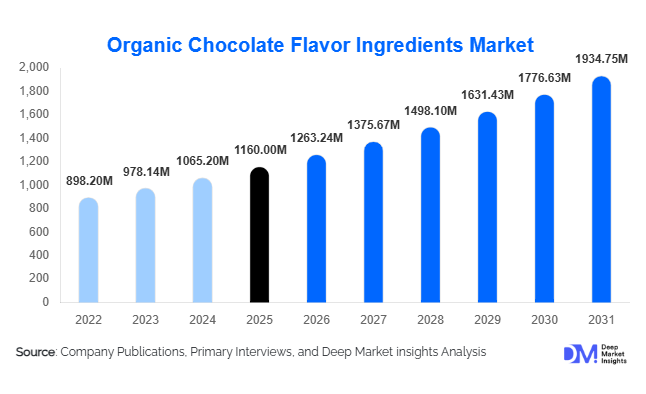

According to Deep Market Insights,the global organic chocolate flavor ingredients market size was valued at USD 1,160 million in 2025 and is projected to grow from USD 1,263.24 million in 2026 to reach USD 1,934.75 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The organic chocolate flavor ingredients market growth is primarily driven by increasing consumer demand for clean-label confectionery and bakery products, rising preference for certified organic cocoa derivatives, and expanding applications in functional foods and premium beverages.

Key Market Insights

- Organic cocoa powder dominates the ingredient landscape, accounting for over 35% of total market revenue due to its wide application across bakery, dairy, and beverage products.

- Direct B2B sourcing remains the primary distribution channel, representing more than 50% of procurement volumes as multinational food manufacturers prioritize supply chain traceability.

- Europe leads global consumption, supported by stringent organic regulations and strong premium chocolate manufacturing traditions.

- Asia-Pacific is the fastest-growing regional market, driven by rising middle-class income and increasing demand for premium and health-oriented chocolate products.

- Food & beverage processing accounts for nearly 58% of total demand, reflecting industrial-scale usage of organic cocoa derivatives.

- Technological advancements in fermentation and flavor encapsulation are improving taste stability and expanding customized flavor applications.

What are the latest trends in the organic chocolate flavor ingredients market?

Clean-Label and Single-Origin Cocoa Expansion

Consumers are increasingly scrutinizing ingredient labels, leading to strong growth in certified organic and single-origin cocoa ingredients. Manufacturers are highlighting traceability, ethical sourcing, and origin transparency on product packaging. Single-origin organic cocoa powder and cocoa liquor are gaining traction among premium chocolate and artisanal bakery brands seeking differentiated flavor profiles. This trend is particularly strong in Europe and North America, where consumers are willing to pay 15–25% premiums for ethically sourced and organic-certified chocolate products. Companies are investing in blockchain-enabled traceability platforms and farm-level partnerships to ensure authenticity and compliance with USDA and EU organic standards.

Integration into Functional and Plant-Based Products

Organic chocolate flavor ingredients are increasingly incorporated into plant-based dairy alternatives, protein bars, and nutraceutical beverages. Cocoa’s natural antioxidant content and flavonoid-rich profile align with consumer demand for indulgence combined with health benefits. Functional beverage manufacturers are using organic cocoa extracts in low-sugar formulations, while vegan product lines rely on organic cocoa butter and powder for clean-label positioning. This trend is expanding beyond confectionery into sports nutrition, wellness snacks, and fortified beverages, diversifying the demand base for organic cocoa derivatives.

What are the key drivers in the organic chocolate flavor ingredients market?

Rising Organic Food Consumption

Global organic food sales have expanded steadily over the past decade, directly benefiting organic flavor ingredient markets. Consumers associate organic chocolate ingredients with higher quality, safety, and sustainability. Retailers are expanding shelf space for organic confectionery, prompting manufacturers to secure certified organic cocoa supplies. The premium pricing advantage further incentivizes ingredient adoption among food processors.

Sustainability and Ethical Sourcing Commitments

Major chocolate and food brands have pledged sustainable and transparent cocoa sourcing by 2030. Organic certification aligns with these commitments, driving procurement of certified cocoa powder, butter, and liquor. Ethical sourcing not only improves brand image but also mitigates regulatory risks associated with environmental and labor concerns. Increasing partnerships with farmer cooperatives in Latin America and Africa strengthen supply reliability and long-term growth.

What are the restraints for the global market?

High Raw Material Price Volatility

Organic cocoa beans command 20–35% price premiums compared to conventional cocoa due to lower yields and certification costs. Fluctuating weather patterns in West Africa and Latin America further affect supply stability. Price volatility can compress margins for ingredient processors and end-product manufacturers, especially during peak demand cycles.

Limited Organic Cocoa Supply Base

Certified organic cocoa accounts for a relatively small share of total global cocoa production. Expanding certified acreage requires time, farmer training, and regulatory compliance. Supply bottlenecks can restrict rapid capacity expansion and limit scalability for large multinational food manufacturers.

Ingredient Type Insights

Organic cocoa powder leads the global organic chocolate ingredients market, accounting for approximately 36% of total revenue in 2025. The segment’s dominance is primarily driven by its extensive versatility and cost efficiency across multiple food formulations. Organic cocoa powder is widely incorporated into bakery premixes, chocolate beverages, dairy desserts, breakfast cereals, and confectionery fillings, making it the preferred base ingredient for manufacturers seeking consistent flavor intensity and natural coloring properties. Its ease of blending, stable shelf life, and compatibility with clean-label formulations further strengthen its leading position. Organic cocoa butter follows as a key premium ingredient, particularly in high-end chocolate manufacturing and plant-based dairy alternatives, where texture, mouthfeel, and gloss are critical quality parameters. Demand for organic cocoa liquor and specialty extracts continues to expand within artisanal and craft chocolate production, where single-origin and minimally processed ingredients command higher margins. Additionally, certified organic flavor blends are gaining traction among large-scale manufacturers seeking standardized taste profiles, formulation consistency, and regulatory compliance while maintaining organic certification integrity.

Form Insights

Powdered organic chocolate ingredients dominate the market with nearly 48% share in 2025, supported by strong demand from bakery, beverage premix, and dry snack manufacturers. The leading driver for this segment is its extended shelf stability and simplified logistics, which reduce storage costs and minimize spoilage risk. Powdered formats also offer ease of transportation and precise dosing in large-scale production lines, enhancing operational efficiency. Liquid extracts maintain significant adoption in beverage and dairy processing applications due to their rapid solubility and uniform dispersion in ready-to-drink formulations. Paste and block formats remain essential for industrial confectionery applications where controlled melting characteristics and cocoa butter content are crucial for tempering processes. Meanwhile, granules and chips are witnessing rising adoption among bakery and snack manufacturers due to their uniform particle size, portion control advantages, and consistent distribution in cookies, muffins, and snack bars.

Application Insights

Confectionery remains the largest application segment, accounting for around 34% of overall market share in 2025. The leading driver for this segment is sustained global demand for premium and organic-certified chocolate products, including bars, filled pralines, truffles, and coated snacks. Organic cocoa liquor and butter are integral to achieving high cocoa content and smooth texture in premium offerings. Bakery applications represent a significant secondary segment, supported by rising consumer preference for organic cakes, brownies, pastries, and dessert mixes formulated without synthetic additives. Nutraceutical and functional food applications are emerging as the fastest-growing segment, fueled by increasing incorporation of organic cocoa extracts in protein bars, fortified beverages, meal replacements, and antioxidant-rich supplements. Growing consumer awareness of cocoa’s polyphenol content and potential wellness benefits further accelerates adoption in health-focused product lines.

Distribution Channel Insights

Direct B2B sales account for approximately 52% of global revenue, making it the dominant distribution channel. The leading driver behind this segment is manufacturers’ preference for long-term procurement contracts that ensure traceable sourcing, price stability, and consistent quality compliance with organic standards. Large confectionery and beverage companies rely heavily on direct supplier relationships to secure certified organic cocoa derivatives. Ingredient distributors play a vital role in serving mid-sized processors and specialty brands that require flexible order volumes and technical support. Online B2B procurement platforms are gradually expanding access for emerging market manufacturers by improving supplier visibility and simplifying international sourcing processes. Specialty organic ingredient suppliers continue to cater to artisanal and small-batch chocolate producers seeking premium, single-origin, or customized formulations.

End-Use Industry Insights

Food and beverage processing dominates overall demand, contributing nearly 58% of the total market. Valued at over USD 720 million in 2026, this segment continues to expand alongside global confectionery exports and rising demand for clean-label formulations. The leading growth driver is the increasing reformulation of mainstream chocolate and bakery products to meet organic certification standards and evolving consumer preferences for transparency in sourcing. Health and wellness product manufacturers represent the fastest-growing end-use industry, expanding at approximately 11% CAGR. The rapid rise of plant-based beverages, functional snacks, and high-protein confectionery alternatives is significantly influencing organic cocoa ingredient utilization. Cosmetic and personal care applications are also gradually incorporating organic cocoa butter due to its emollient properties and alignment with natural ingredient positioning trends.

| By Ingredient Type | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global market share in 2025, led by the United States and Canada. The United States remains the dominant contributor due to high per capita organic food consumption, strong certification infrastructure, and advanced supply chain traceability systems. Growth in the region is driven by rising demand for premium chocolate, clean-label bakery products, and functional snacks. Expansion of private-label organic confectionery offerings by major retailers further supports procurement of certified organic cocoa derivatives. In addition, increasing consumer awareness regarding sustainable sourcing and ethical trade practices strengthens demand for certified organic and Fairtrade cocoa ingredients across the region.

Europe

Europe leads with nearly 34% of global market share in 2025, supported by strong demand in Germany, France, the United Kingdom, Italy, Belgium, and Switzerland. The region’s growth is primarily driven by stringent organic certification regulations, well-established artisanal chocolate traditions, and strong consumer preference for ethically sourced ingredients. European manufacturers emphasize single-origin organic cocoa and transparent supply chains to reinforce premium brand positioning. Growing demand for vegan and plant-based chocolate products further accelerates utilization of organic cocoa butter and powder. Additionally, sustainability initiatives and carbon-neutral production targets adopted by leading confectionery companies continue to stimulate demand for certified organic cocoa inputs.

Asia-Pacific

Asia-Pacific holds around 22% market share and represents the fastest-growing region, expanding at over 10% CAGR. Rapid urbanization, rising disposable incomes, and growing exposure to premium Western-style confectionery products are key growth drivers. China and India are witnessing increasing consumption of premium and imported chocolate products, while Japan and Australia maintain steady demand for high-quality confectionery ingredients. The region also benefits from expanding local manufacturing capacity for bakery and snack products, encouraging greater incorporation of organic cocoa powder and extracts. Increasing health awareness and adoption of functional foods further contribute to strong regional expansion.

Latin America

Latin America accounts for approximately 7% of the global market share, with Brazil and Mexico leading consumption. Regional growth is supported by expanding middle-class populations and rising domestic chocolate production. The presence of organic cocoa cultivation in countries such as Peru and the Dominican Republic enhances vertical integration opportunities and export competitiveness. Growing investments in sustainable farming practices and organic certification programs are strengthening the region’s position as both a producer and consumer of organic cocoa ingredients.

Middle East & Africa

The Middle East and Africa region contributes nearly 5% of the global market. The United Arab Emirates and South Africa serve as key consumption hubs due to rising premium confectionery demand and expanding retail infrastructure. Increasing tourism-driven chocolate sales and growth in specialty dessert outlets further support regional demand. Meanwhile, several West African nations remain critical suppliers of organic-certified cocoa beans, providing upstream supply advantages. Continued investments in organic farming certification and export-oriented processing facilities are expected to gradually enhance regional value addition over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Organic Chocolate Flavor Ingredients Market

- Barry Callebaut

- Cargill Incorporated

- Olam Group

- Blommer Chocolate Company

- ECOM Agroindustrial

- Puratos Group

- Guittard Chocolate Company

- Valrhona

- TCHO Chocolate

- Ghirardelli Chocolate Company

- Tradin Organic

- The Hershey Company

- Mars Incorporated

- Nestlé S.A.

- Mondelez International