Online Dating Services Market Size

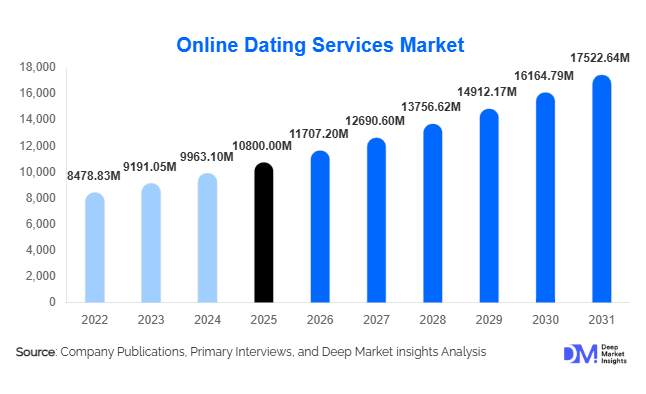

According to Deep Market Insights, the global online dating services market size was valued at USD 10,800 million in 2025 and is projected to grow from USD 11,707.20 million in 2026 to reach USD 17,522.64 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The online dating services market growth is primarily driven by increasing smartphone penetration, shifting social norms toward digital relationships, and the rapid adoption of AI-powered matchmaking technologies that enhance user engagement and personalization.

Key Market Insights

- Mobile-first platforms dominate the market, accounting for over 70% of user engagement due to accessibility and real-time connectivity features.

- Freemium monetization models are leading revenue generation, enabling platforms to scale user bases while converting premium users through value-added features.

- North America dominates the global market, supported by high subscription adoption and mature digital ecosystems.

- Asia-Pacific is the fastest-growing region, driven by rising internet penetration and evolving cultural acceptance of online dating.

- AI-driven personalization and video dating are transforming user experiences, increasing match accuracy and engagement rates.

- Niche dating platforms are expanding rapidly, targeting specific demographics such as religion, lifestyle, and LGBTQ+ communities.

What are the latest trends in the online dating services market?

AI-Powered Matchmaking and Behavioral Analytics

Online dating platforms are increasingly leveraging artificial intelligence and machine learning to enhance matchmaking accuracy. These technologies analyze user preferences, behavior patterns, and interaction history to provide more compatible matches. Predictive analytics is also being used to improve user retention by identifying engagement trends and recommending optimal matches. This trend is particularly important in competitive markets where user experience differentiation is critical for growth.

Rise of Video Dating and Virtual Interaction

Video dating has emerged as a mainstream feature, enabling users to interact in real time before meeting physically. Platforms are integrating live streaming, virtual events, and video-based profiles to enhance authenticity and engagement. This trend gained momentum during the pandemic and continues to grow as users prioritize safety and meaningful interactions. Virtual dating features are also creating new monetization avenues through premium video access and virtual gifting.

What are the key drivers in the online dating services market?

Increasing Smartphone and Internet Penetration

The widespread adoption of smartphones and affordable internet access has significantly expanded the user base for online dating services. Emerging markets, particularly in Asia-Pacific and Latin America, are witnessing rapid growth due to improved connectivity and digital literacy. Mobile applications enable seamless user experiences, making online dating more accessible and convenient.

Changing Social Norms and Relationship Dynamics

Societal attitudes toward relationships and marriage are evolving, with younger generations increasingly open to online dating. Delayed marriages, urban lifestyles, and busy work schedules have further driven the adoption of digital matchmaking platforms. Additionally, the growing acceptance of LGBTQ+ relationships has expanded the addressable market.

Technological Advancements in User Experience

Innovations such as AI matchmaking, geolocation services, and enhanced security features are improving platform reliability and user satisfaction. These technologies reduce fake profiles, increase trust, and provide personalized experiences, which are critical for user retention and monetization.

What are the restraints for the global market?

Data Privacy and Security Concerns

Privacy issues remain a significant challenge, as users are required to share personal and sensitive information. Data breaches and misuse of user data can negatively impact trust and hinder market growth. Regulatory compliance with data protection laws also increases operational complexity for service providers.

Market Saturation in Developed Regions

In mature markets such as North America and Europe, high competition and user saturation are leading to increased customer acquisition costs. This creates pricing pressures and limits growth opportunities for new entrants, making it difficult to achieve profitability.

What are the key opportunities in the online dating services industry?

Expansion into Emerging Markets

Emerging economies such as India, Southeast Asia, and parts of Africa present significant growth opportunities due to rising internet penetration and changing cultural attitudes toward online relationships. Localization strategies, including language support and culturally relevant features, can help platforms capture new user segments and drive revenue growth.

Integration of Immersive Technologies

The adoption of virtual reality (VR), augmented reality (AR), and live streaming features is creating new opportunities for user engagement. These technologies enable immersive dating experiences, such as virtual dates and interactive environments, enhancing user satisfaction and increasing monetization potential.

Development of Niche and Specialized Platforms

Niche dating platforms targeting specific demographics, such as religious groups, professionals, or lifestyle communities, are gaining popularity. These platforms offer tailored experiences and higher match success rates, attracting users willing to pay for premium services. This trend allows companies to diversify their offerings and reduce competition in saturated segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 10800 Million |

| Market Size in 2026 | USD 11707.20 Million |

| Market Size in 2031 | USD 17522.64 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Service Type Insights

Social dating platforms continue to dominate the global online dating services market, accounting for approximately 38% of total market share in 2025. This leadership is primarily driven by their strong appeal among younger demographics, particularly Gen Z and millennials, who prefer intuitive, swipe-based interfaces and gamified user experiences. The ease of onboarding, low entry barriers, and high engagement frequency have made these platforms the primary driver of user volume globally. Additionally, continuous feature innovation—such as short-form video profiles, AI-based recommendations, and real-time chat functionalities—has significantly enhanced user stickiness and monetization potential.

Matchmaking services are witnessing steady growth, especially among users seeking serious and long-term relationships. These platforms leverage advanced algorithms and psychological profiling to improve compatibility outcomes, making them particularly popular in developed markets and among older demographics. Meanwhile, niche dating platforms are expanding rapidly by catering to specific communities based on religion, ethnicity, profession, or lifestyle preferences. This targeted approach not only improves match success rates but also allows platforms to command premium pricing. Video dating and live interaction platforms represent a high-growth sub-segment, driven by increasing demand for authenticity, safety, and real-time engagement. The shift toward virtual interactions has accelerated post-pandemic, with users increasingly preferring video-first experiences before in-person meetings, thereby reshaping the future of digital dating ecosystems.

Revenue Model Insights

The freemium model remains the dominant revenue strategy, contributing approximately 42% of the global market revenue in 2025. Its success lies in enabling platforms to acquire a large user base through free access while monetizing premium features such as profile boosts, unlimited swipes, and enhanced visibility. This model is particularly effective in emerging markets where price sensitivity is high, but user engagement is strong. Subscription-based models continue to perform strongly in mature markets such as North America and Europe, where users are more willing to pay for enhanced experiences, ad-free interfaces, and advanced matchmaking features. These models provide predictable and recurring revenue streams, improving financial stability for service providers.

Advertising-based platforms and in-app purchases also play a crucial role in revenue diversification. In-app monetization strategies, including virtual gifts, super likes, and exclusive content access, are gaining traction, particularly among younger users. The integration of microtransactions and tiered pricing strategies is further optimizing revenue per user and increasing overall platform profitability.

Platform Type Insights

Mobile applications dominate the online dating services market, accounting for nearly 72% of the total market share in 2025. This dominance is driven by the widespread adoption of smartphones, improved mobile internet infrastructure, and the convenience of accessing dating platforms on-the-go. Features such as geolocation-based matching, push notifications, and seamless integration with social media platforms have significantly enhanced user engagement on mobile apps. Web-based platforms, while still relevant, are gradually losing market share as user preferences shift toward mobile-first experiences. However, they continue to serve niche segments, particularly older demographics and users in regions with limited mobile optimization. Despite this decline, web platforms remain important for detailed profile management and long-form interactions, complementing mobile usage in a multi-platform ecosystem.

Age Group Insights

The 25–34 years age group leads the market with approximately 36% share in 2025, driven by a combination of high digital literacy, active social lifestyles, and greater spending capacity. This demographic is highly engaged across both casual and long-term dating platforms, making it the primary revenue-generating segment. Their willingness to pay for premium features and enhanced visibility further strengthens their contribution to overall market value. The 18–24 age group plays a critical role in driving user volume and engagement, particularly on social dating platforms. This segment is highly responsive to new features, trends, and gamified experiences, making it a key target for innovation. Meanwhile, users aged 35 and above are increasingly adopting online dating services, particularly for serious relationships and marriage-oriented platforms. This trend is expanding the market’s demographic reach and contributing to sustained growth.

Purpose Insights

Platforms focused on long-term relationships hold a leading position, accounting for approximately 34% of the global market in 2025. This dominance is driven by a growing preference among users for meaningful and stable connections, particularly in urban and developed markets. Advanced matchmaking algorithms, compatibility scoring, and personalized recommendations are key drivers supporting this segment’s growth.

Casual dating remains highly popular, especially among younger users seeking flexible and non-committal interactions. These platforms benefit from high engagement rates and frequent usage, contributing significantly to overall market activity. Meanwhile, marriage-oriented platforms are experiencing strong growth in regions such as Asia-Pacific and the Middle East, where cultural preferences for structured matchmaking and family involvement remain prevalent. This segment is particularly lucrative due to higher subscription rates and longer user lifecycles.

Explore more data points, trends and opportunities Download Free Sample Report

Online Dating Services Market Segmentations

By Service Type

- Matchmaking Services

- Social Dating Platforms

- Niche Dating Platforms

- Video Dating & Live Interaction Platforms

- Marriage & Matrimonial Platforms

By Revenue Model

- Subscription-Based Services

- Freemium Model

- Advertising-Based Platforms

- In-App Purchases

By Platform Type

- Mobile Applications

- Web/Desktop Platforms

By Age Group

- 18–24 Years

- 25–34 Years

- 35–44 Years

- 45+ Years

By Purpose

- Casual Dating

- Long-Term Relationships

- Marriage-Oriented Platforms

- Friendship/Networking

Regional Insights

North America

North America remains the largest market, accounting for approximately 35% of global revenue in 2025, with the United States as the primary contributor. The region’s dominance is driven by high smartphone penetration, strong digital payment infrastructure, and widespread acceptance of online dating across all age groups. Premium subscription adoption is particularly high, supported by higher disposable incomes and willingness to pay for enhanced user experiences. Additionally, continuous innovation by leading market players and the integration of advanced technologies such as AI and video dating are further strengthening regional growth. Canada also contributes significantly, benefiting from similar technological and cultural trends.

Europe

Europe holds around 25% of the global market share, led by countries such as the United Kingdom, Germany, and France. The region’s growth is driven by high internet penetration, strong regulatory frameworks for data protection, and increasing user trust in digital platforms. The General Data Protection Regulation (GDPR) has enhanced transparency and security, encouraging more users to adopt online dating services. Additionally, the growing popularity of niche and serious relationship platforms among European users is contributing to market expansion. Younger demographics are also driving demand for innovative features and socially conscious platforms.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with countries such as India, China, and Japan leading demand. Rapid urbanization, increasing smartphone penetration, and changing cultural attitudes toward relationships are key growth drivers. India is experiencing particularly strong growth, supported by a large युवा population, rising internet accessibility, and increasing acceptance of digital matchmaking, especially in urban areas. In China, local platforms are leveraging AI and social media integration to enhance user engagement. Japan and Southeast Asian countries are also witnessing rising adoption due to busy lifestyles and delayed marriages, making digital dating a convenient alternative.

Latin America

Latin America is experiencing steady growth, with Brazil and Mexico as key markets. The region’s expansion is driven by increasing urbanization, growing smartphone usage, and strong integration of social media with dating platforms. Cultural openness to social interactions and a युवा demographic profile further support market growth. Additionally, the rising popularity of freemium models aligns well with the region’s price-sensitive user base, enabling platforms to scale rapidly while gradually increasing monetization through premium features.

Middle East & Africa

The Middle East and Africa region is emerging as a promising market, with countries such as the UAE, Saudi Arabia, and South Africa showing increasing adoption of online dating services. Growth in this region is driven by rising internet penetration, a young population, and gradual cultural shifts toward digital interactions. In the Middle East, premium and discreet dating platforms are gaining traction due to cultural sensitivities, while in Africa, mobile-first solutions are expanding rapidly due to widespread smartphone adoption. Government investments in digital infrastructure and increasing exposure to global social trends are further accelerating market growth across the region.

Key Players in the Online Dating Services Market

- Match Group Inc.

- Bumble Inc.

- Spark Networks SE

- Grindr Inc.

- eHarmony Inc.

- Zoosk Inc.

- The Meet Group Inc.

- Coffee Meets Bagel Inc.

- Tantan

- Shaadi.com

- TrulyMadly

- Happn

- Momo Inc.

- OkCupid

- Plenty of Fish