Omega-3 Testing Market Size

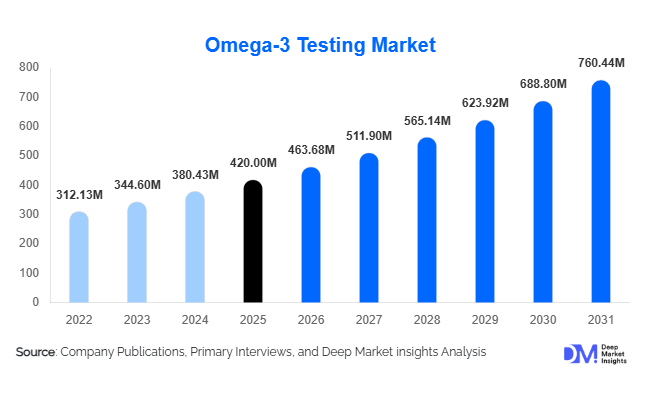

According to Deep Market Insights,the global omega-3 testing market size was valued at USD 420 million in 2026 and is projected to grow from USD 463.68 million in 2026 to reach USD 760.44 million by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The omega-3 testing market growth is primarily driven by rising global consumption of omega-3 supplements, increasing regulatory compliance requirements, and technological advancements in analytical testing methods for dietary supplements, functional foods, pharmaceuticals, and aquaculture products.

Key Market Insights

- Fatty acid profile testing dominates the market, as precise quantification of EPA and DHA is critical for label compliance, consumer safety, and regulatory adherence.

- Gas chromatography remains the leading technology, widely adopted due to its accuracy, reliability, and cost-effectiveness in quantifying omega-3 content.

- North America leads regional demand, supported by strict FDA regulations, high supplement consumption, and a preference for third-party certified testing services.

- Asia-Pacific is the fastest-growing region, driven by expanding nutraceutical manufacturing in India and China, rising middle-class wealth, and export-oriented omega-3 production.

- Third-party contract testing services are increasingly preferred, as independent verification ensures compliance with global pharmacopeial standards and export regulations.

- Technological integration, including AI-enabled chromatography and rapid testing kits, is reshaping laboratory workflows, reducing turnaround times, and improving analytical precision.

What are the latest trends in the omega-3 testing market?

Emergence of Rapid and Automated Testing

Laboratories are increasingly adopting high-throughput testing platforms and automated GC-MS or LC-MS/MS systems. These innovations reduce sample processing times, minimize human error, and allow for large-scale testing of dietary supplements, functional foods, and pharmaceutical formulations. Portable rapid test kits are also gaining traction for on-site testing in manufacturing facilities and aquaculture setups, ensuring real-time quality control. Such technological advances are enabling testing service providers to scale operations and meet the growing global demand for validated omega-3 products.

Focus on Sustainability and Plant-Based Omega-3s

The shift from marine-derived fish oils to plant-based and algal omega-3 formulations is driving the need for specialized testing methodologies. Laboratories are adapting analytical techniques to verify purity, potency, and oxidative stability in these novel matrices. This trend is particularly pronounced in Europe and North America, where consumer preference for sustainable supplements is increasing, creating new market opportunities for testing providers.

What are the key drivers in the omega-3 testing market?

Increasing Global Supplement Consumption

The surge in dietary supplement adoption, particularly omega-3 products for cardiovascular, cognitive, and maternal health, is a major growth driver. Consumers are increasingly conscious of dosage accuracy and product safety, prompting manufacturers to invest heavily in third-party testing for compliance with labeling and quality standards.

Regulatory Compliance and Standardization

Strict regulations from the FDA, EFSA, and Japan’s Pharmaceuticals and Medical Devices Agency have made omega-3 testing mandatory for contaminants, potency, and oxidative stability. Non-compliance can result in recalls, fines, and reputational damage, creating consistent demand for certified analytical testing services.

Expansion of Pharmaceutical and Aquaculture Applications

Prescription-grade omega-3 drugs and aquaculture feed formulations require rigorous quality verification. Growth in these industries has significantly boosted demand for fatty acid profiling, contaminant screening, and stability testing, ensuring that products meet stringent pharmacopeial standards and bioavailability requirements.

What are the restraints for the global market?

High Capital Investment

Advanced analytical equipment such as GC-MS, LC-MS/MS, and automated chromatography systems require significant investment, limiting entry for smaller laboratories. Maintenance and skilled labor costs further increase operational expenses.

Raw Material Variability

Fluctuations in fish oil quality and the introduction of new plant-based omega-3 matrices necessitate continual method adaptation, increasing testing complexity and costs. Variability in raw material composition poses challenges for consistent and accurate testing.

What are the key opportunities in the omega-3 testing industry?

Emerging Markets and Export-Driven Demand

Asia-Pacific, particularly China and India, offers substantial growth opportunities due to expanding nutraceutical manufacturing and rising exports to North America and Europe. Investment in testing infrastructure in these regions allows laboratories to capture long-term service contracts from manufacturers seeking global market compliance.

Integration of Advanced Analytical Technologies

Automation, AI, and high-throughput chromatographic systems provide laboratories with the ability to scale operations efficiently. Companies that invest in such technologies can reduce turnaround times, lower per-sample costs, and offer more precise testing for complex omega-3 formulations.

New Product Matrices and Plant-Based Omega-3s

The rise of algal and fermentation-derived omega-3 oils presents opportunities for laboratories to develop specialized testing protocols. These novel products require dedicated oxidative stability, purity, and potency verification, expanding the scope of laboratory services and increasing revenue potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 420 Million |

| Market Size in 2026 | USD 463.68 Million |

| Market Size in 2031 | USD 760.44 Million |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segment Insights

The omega-3 testing services market is characterized by strong demand across multiple service and application categories, with leadership concentrated in technically rigorous and regulatory-driven segments. By test type, fatty acid profile testing accounts for approximately 38% of the global market in 2025, making it the leading segment. This dominance is primarily driven by the critical need to validate and quantify essential omega-3 fatty acids such as EPA and DHA, which form the core value proposition of fish oil, algal oil, and other omega-3 formulations. Regulatory authorities and international buyers require accurate confirmation of labeled EPA and DHA concentrations, while brand owners rely on precise fatty acid profiling to differentiate premium formulations and ensure consistency across production batches.

In terms of technology platform, gas chromatography holds around 42% of the global market share, supported by its high accuracy, reproducibility, and global regulatory acceptance. Gas chromatography remains the industry benchmark for fatty acid methyl ester (FAME) analysis, enabling laboratories to meet stringent pharmacopeial and export standards. Its widespread adoption across contract laboratories and in-house testing facilities, combined with continuous upgrades to GC-MS systems for enhanced sensitivity and automation, reinforces its leading position.

By sample type, dietary supplements represent approximately 35% of total testing demand, reflecting the high production and export volumes of omega-3 capsules, soft gels, syrups, and fortified formats. The growth of private-label brands, e-commerce distribution, and cross-border trade has intensified the need for batch-wise validation, contaminant screening, and oxidation stability testing, further consolidating the leadership of this segment.

Based on service type, third-party contract testing commands about 46% of the market share, emerging as the dominant service model. This leadership is driven by regulatory preference for independent validation, retailer-mandated certifications, and the need for internationally accredited laboratory reports to facilitate exports. Contract laboratories offer cost efficiency, specialized expertise, and access to advanced instrumentation, making them the preferred choice for small and mid-sized nutraceutical manufacturers as well as large multinational brands seeking unbiased quality assurance.

From an end-use industry perspective, nutraceutical manufacturers account for nearly 40% of total demand, supported by rising global supplement consumption, preventive healthcare trends, and expanding product portfolios that include heart health, cognitive support, prenatal nutrition, and sports recovery formulations. The sustained expansion of the global dietary supplement industry continues to anchor testing demand across raw material validation, in-process quality control, and finished product certification.

End-Use Insights

Nutraceutical and dietary supplement manufacturers remain the largest consumers of omega-3 testing services, driven by stringent label compliance requirements, brand reputation management, and increasing consumer scrutiny regarding purity and potency. As regulatory authorities tighten guidelines around heavy metals, oxidation markers, and concentration claims, manufacturers are prioritizing comprehensive analytical testing to mitigate recall risks and protect market credibility.

Pharmaceutical companies represent the fastest-growing end-use segment, supported by the increasing adoption of prescription-grade omega-3 drugs for cardiovascular and metabolic disorders. The development of highly purified EPA formulations and clinical-grade omega-3 products necessitates advanced analytical validation, stability testing, and compliance with pharmacopeial standards, significantly elevating demand for sophisticated laboratory services.

Clinical research organizations are increasingly leveraging omega-3 biomarker testing in cardiovascular, neurological, and maternal health studies. The integration of omega-3 index testing into clinical trials and population health research is expanding the scope of laboratory services beyond traditional product testing into diagnostic and research applications. In parallel, export-driven demand from major manufacturing hubs such as India, China, and Norway remains significant, as compliance with U.S., European, and Asian regulatory frameworks requires rigorous third-party certification. Functional food and beverage companies are also expanding omega-3 fortification across dairy, bakery, and beverage categories, broadening the application landscape for stability, homogeneity, and oxidation testing.

Explore more data points, trends and opportunities Download Free Sample Report

Omega-3 Testing Market Segmentations

By Test Type

- Fatty Acid Profile Testing (EPA/DHA Quantification)

- Omega-6 to Omega-3 Ratio Testing

- Oxidative Stability & Peroxide Value Testing

- Contaminant Testing (Heavy Metals, PCBs, Dioxins)

- Purity & Potency Validation Testing

By Technology Platform

- Gas Chromatography (GC-FID, GC-MS)

- Liquid Chromatography (HPLC, UHPLC)

- Mass Spectrometry (LC-MS/MS)

- Spectroscopy (NIR, FTIR)

- Rapid Test Kits & Point-of-Care Devices

By Sample Type

- Dietary Supplements & Capsules

- Functional Foods & Beverages

- Pharmaceutical Formulations

- Animal Feed & Aquaculture Feed

- Biological Samples (Blood, Plasma, RBC Membranes)

By Service Type

- Third-Party Contract Testing Services

- In-House Laboratory Testing

- Regulatory Compliance Testing

- Research & Development Analytical Testing

By End-Use Industry

- Nutraceutical & Dietary Supplement Manufacturers

- Pharmaceutical Companies

- Functional Food & Beverage Companies

- Clinical Research Organizations (CROs)

- Aquaculture & Animal Nutrition Companies

Regional Insights

North America

North America accounts for approximately 34% of the global omega-3 testing services market in 2025, with the United States leading regional demand. Growth in this region is primarily driven by high per capita dietary supplement consumption, strict regulatory oversight by the U.S. Food and Drug Administration, and strong retailer requirements for third-party certification. The mature nutraceutical ecosystem, presence of large contract testing laboratories, and rising demand for pharmaceutical-grade omega-3 formulations further strengthen regional market leadership. In Canada, expanding nutraceutical manufacturing clusters and compliance with Natural Health Product regulations are accelerating demand for accredited testing services, particularly for export-oriented brands targeting the U.S. and European markets.

Europe

Europe represents around 29% of the global market, led by Germany, France, the United Kingdom, and Norway. Regional growth is strongly influenced by rigorous regulatory frameworks under the European Food Safety Authority and heightened consumer preference for sustainable and traceable omega-3 sources. Norway’s position as a major fish oil exporter necessitates extensive purity, potency, and contaminant testing to comply with international trade standards. In addition, European manufacturers are increasingly adopting rapid testing methods, automation, and digital laboratory management systems to enhance throughput and maintain compliance with evolving quality benchmarks. Sustainability certifications and marine sourcing transparency further reinforce the need for comprehensive analytical validation.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of over 11%. China and India are rapidly scaling omega-3 supplement production, supported by government-backed manufacturing initiatives and expanding domestic consumption. The rise of export-oriented nutraceutical companies in these countries significantly increases demand for third-party contract testing to meet North American and European regulatory requirements. Japan and Australia maintain steady demand, driven by established pharmaceutical and functional food sectors that prioritize high-quality laboratory validation. Growing health awareness, urbanization, and rising disposable incomes across Southeast Asia are also contributing to the region’s accelerated testing demand.

Latin America

Latin America is witnessing gradual yet steady growth, particularly in Brazil, Mexico, and Argentina. Regional expansion is driven by increasing consumer awareness of preventive healthcare, a growing middle-class population, and rising imports of premium dietary supplements. Regulatory modernization efforts and improving quality standards are encouraging manufacturers and distributors to adopt structured testing protocols. Export ambitions among local nutraceutical producers are also pushing demand for internationally accredited laboratory certifications, strengthening the region’s testing infrastructure.

Middle East & Africa

The Middle East & Africa region presents a mixed growth landscape. Parts of Africa, which host important fish oil production and marine resource centers, play a strategic role in raw material supply chains, thereby requiring testing for purity, oxidation, and contaminant levels prior to export. In the Middle East, countries such as the United Arab Emirates, Saudi Arabia, and Qatar are emerging as high-value consumer markets driven by affluent populations and increasing demand for premium imported supplements. Government-led diversification initiatives and investments in laboratory infrastructure are enhancing regional testing capabilities, supporting both domestic quality assurance and export-oriented validation services.

Key Players in the Omega-3 Testing Market

- Eurofins Scientific

- SGS SA

- Intertek Group plc

- Bureau Veritas

- TÜV SÜD

- ALS Limited

- Mérieux NutriSciences

- AsureQuality

- NSF International

- UL Solutions

- Covance Inc.

- Thermo Fisher Scientific

- Waters Corporation

- Agilent Technologies

- Shimadzu Corporation