Omega-3 Fatty Acids EPA and DHA Market Size

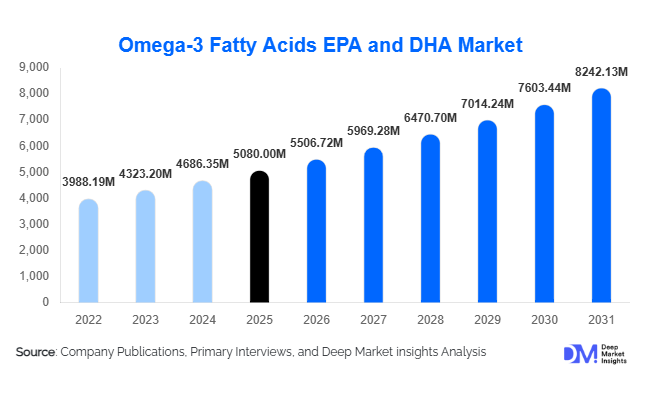

According to Deep Market Insights,the global omega-3 fatty acids EPA and DHA market size was valued at USD 5,080 million in 2025 and is projected to grow from USD 5,506.72 million in 2026 to reach USD 8,242.13 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer awareness regarding cardiovascular and cognitive health, expanding demand for preventive healthcare solutions, increasing prescription use of high-purity EPA formulations, and the growing incorporation of DHA in infant nutrition and functional food products. The industry is also benefiting from sustainability-driven shifts toward algal-based omega-3 production and technological advancements in purification and encapsulation processes.

Key Market Insights

- Dietary supplements remain the dominant application segment, accounting for nearly 46% of the global market value in 2025, driven by strong consumer demand for preventive health products.

- Marine-sourced omega-3 leads the market, contributing approximately 72% of total revenue in 2025, supported by established supply chains and cost efficiencies.

- Nutraceutical grade products hold the largest share, representing around 58% of the market, reflecting the rapid growth of OTC supplement consumption.

- North America dominates the global market with nearly 34% share in 2025, led by strong demand in the United States.

- Asia-Pacific is the fastest-growing region, expanding at over 9.5% CAGR due to rising middle-class populations and expanding nutraceutical penetration.

- Pharmaceutical-grade EPA products command premium pricing, often 30–40% higher than standard nutraceutical formulations.

What are the latest trends in the omega-3 fatty acids EPA and DHA market?

Shift Toward Algal and Sustainable Omega-3 Sources

Sustainability concerns surrounding overfishing and marine ecosystem pressure are accelerating the adoption of algal-based omega-3 production. Microalgae-derived DHA and EPA are increasingly used in infant formula, vegan supplements, and pharmaceutical applications due to their purity and traceability. Companies are investing in fermentation-based technologies and closed-loop cultivation systems to enhance scalability and reduce environmental impact. ESG-driven investment flows and consumer preference for plant-based nutrition are further supporting this transition. As a result, algal omega-3 is emerging as one of the fastest-growing sub-segments within the market.

High-Purity Pharmaceutical Omega-3 Expansion

Prescription-grade EPA products used in cardiovascular risk management are gaining strong traction globally. Clinical validation studies over recent years have strengthened physician confidence in prescribing high-concentration omega-3 formulations for hypertriglyceridemia and related conditions. Pharmaceutical-grade products, although representing a smaller share than nutraceuticals, contribute disproportionately to revenue due to higher margins. Expansion into emerging healthcare systems and broader regulatory approvals are expected to further boost pharmaceutical uptake.

What are the key drivers in the omega-3 fatty acids EPA and DHA market?

Rising Prevalence of Cardiovascular and Metabolic Disorders

The increasing global burden of cardiovascular disease is a major growth catalyst. Omega-3 EPA and DHA are clinically associated with triglyceride reduction and anti-inflammatory benefits. Growing physician endorsement and patient awareness have significantly boosted both prescription and OTC consumption. Aging populations in North America, Europe, and Japan further amplify demand for heart health supplements.

Rapid Growth of the Global Nutraceutical Industry

The expanding dietary supplement market, growing at approximately 7–8% annually worldwide, has directly supported omega-3 consumption. Consumers increasingly favor preventive health solutions, subscription-based supplement models, and premium branded formulations. Digital marketing and influencer-driven health awareness campaigns have further accelerated retail sales, particularly through e-commerce platforms.

Mandatory DHA Inclusion in Infant Nutrition

Regulatory frameworks in multiple regions now require DHA fortification in infant formula. This mandate has created stable and recurring demand from global baby nutrition manufacturers. Rising maternal health awareness and premiumization of infant formula products are sustaining steady growth in this segment.

What are the restraints for the global market?

Raw Material Volatility and Supply Risk

Fish oil supply is highly dependent on marine harvest volumes, particularly anchovy and sardine fisheries. Climatic events such as El Niño can significantly disrupt supply chains, causing price volatility and margin pressures for manufacturers. This unpredictability remains a structural challenge for marine-based omega-3 producers.

Regulatory and Quality Compliance Costs

Stringent quality standards for pharmaceutical-grade and high-purity nutraceutical products increase operational costs. Compliance with global regulatory bodies requires advanced purification technology, traceability systems, and clinical validation, raising entry barriers for smaller participants.

What are the key opportunities in the omega-3 fatty acids EPA and DHA industry?

Expansion in Emerging Economies

Rising disposable incomes and preventive healthcare awareness in India, Southeast Asia, Brazil, and the Middle East present strong growth opportunities. E-commerce penetration and government-led nutrition programs are expanding consumer access to omega-3 supplements, creating scalable growth potential for both local and global manufacturers.

Technological Innovation and Microencapsulation

Advancements in molecular distillation, supercritical CO₂ extraction, and microencapsulation are improving product stability, taste masking, and bioavailability. These innovations enable broader application in functional foods and beverages, unlocking new revenue streams beyond traditional capsules and softgels.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5080 Million |

| Market Size in 2026 | USD 5506.72 Million |

| Market Size in 2031 | USD 8242.13 Million |

| CAGR | 8.40% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Marine sources continue to dominate the global omega-3 fatty acids EPA and DHA market, accounting for approximately 72% of total revenue in 2025. The leadership of marine-derived omega-3 is supported by established fishing and refining infrastructure across key production hubs such as Peru, Norway, and Chile, ensuring consistent supply of fish oil concentrates for dietary supplement and pharmaceutical applications. The well-developed global supply chain, advanced concentration technologies, and long-standing regulatory approvals further strengthen marine oil’s commercial position. Additionally, widespread consumer familiarity with fish oil supplements continues to reinforce demand across mature markets.

Algal oil, however, represents the fastest-growing source segment, driven by increasing vegan and vegetarian consumer preferences, sustainability concerns, and its application in infant nutrition. Unlike marine sources, algal oil offers a controlled production environment with minimal exposure to ocean contaminants, enabling premium positioning and consistent quality. The rising demand for plant-based supplements, clean-label formulations, and fortified infant formulas is accelerating adoption of algal DHA, particularly in North America and Asia-Pacific. Sustainability certifications and environmental considerations are further enhancing its long-term growth trajectory.

Form Insights

The triglyceride (TG) form leads the market with nearly 48% share in 2025, primarily due to its superior bioavailability and higher consumer trust compared to ethyl ester variants. Consumers increasingly associate triglyceride-based omega-3 with better absorption efficiency and reduced gastrointestinal side effects, which supports its dominance in premium supplement categories. The growing demand for high-concentration and clinically validated formulations continues to drive investment in re-esterified triglyceride technologies.

Re-esterified triglyceride (rTG) formulations are gaining traction within premium nutraceutical segments as manufacturers focus on enhanced potency and purity levels. Meanwhile, phospholipid forms, commonly derived from krill oil, cater to niche, high-value segments targeting cognitive health and cardiovascular support. The increasing consumer preference for differentiated and science-backed formulations is expected to sustain growth across advanced delivery formats.

Grade Insights

Nutraceutical-grade omega-3 accounts for approximately 58% of total market share in 2025, reflecting robust over-the-counter supplement demand and expanding preventive healthcare trends globally. The leading driver for this segment is rising consumer awareness regarding heart health, brain function, joint support, and overall wellness maintenance. Growth in e-commerce penetration and subscription-based supplement models further reinforces the dominance of nutraceutical-grade products.

Pharmaceutical-grade omega-3 contributes around 27% of total revenue but commands significantly higher pricing due to stringent regulatory standards, clinical trial validation, and prescription-based usage. The expansion of cardiovascular prescription therapies and growing physician endorsement of omega-3 formulations are key growth catalysts. Increasing regulatory clarity and pipeline development of high-purity EPA products are expected to strengthen pharmaceutical-grade adoption in the coming years.

Application Insights

Dietary supplements represent nearly 46% of total market value in 2025 and remain the leading application segment. The primary growth driver is the expanding consumer focus on preventive healthcare and long-term wellness management. Strong retail penetration, influencer-driven health awareness, and recurring subscription purchases have accelerated supplement consumption across developed and emerging markets.

Pharmaceutical applications account for approximately 24% of market share, supported by prescription omega-3 therapies targeting hypertriglyceridemia and cardiovascular risk management. The increasing burden of lifestyle-related diseases and aging populations continue to support clinical demand. Infant formula and baby nutrition contribute around 12% of total market value, benefiting from regulatory mandates requiring DHA fortification in several countries and rising consumption of premium and specialty infant formulas. Clinical research linking DHA to early cognitive development further strengthens this segment’s growth outlook.

Distribution Channel Insights

Direct B2B sales to supplement and pharmaceutical manufacturers represent a substantial portion of overall revenue, supported by long-term supply agreements and bulk procurement contracts. Ingredient suppliers maintain strategic partnerships with global nutraceutical brands to ensure stable production volumes and quality consistency.

On the consumer-facing side, retail pharmacies and online platforms dominate sales distribution. Online retail is the fastest-growing channel, driven by increasing digital health awareness, price transparency, and convenience-based purchasing behavior. Subscription models, auto-replenishment services, and targeted digital marketing campaigns are reshaping consumer engagement patterns, particularly in North America and Asia-Pacific.

End-Use Industry Insights

The dietary supplement industry remains the largest end-use sector, with omega-3 consumption valued at over USD 2,400 million in 2025. Growth in this sector is driven by expanding product portfolios across capsules, gummies, functional beverages, and fortified foods. The pharmaceutical sector is growing at nearly 9–10% CAGR, supported by rising prescription adoption and increasing cardiovascular disease prevalence globally. Continuous clinical research and regulatory approvals are expected to further solidify pharmaceutical demand.

Infant nutrition demonstrates stable and premium-oriented demand, valued at approximately USD 650 million in omega-3 consumption in 2025. Increasing parental awareness regarding early brain development and regulatory fortification standards support sustained growth. Export-driven demand from China, Norway, and Peru strengthens global trade flows, while aquaculture feed applications are expanding to enhance the nutritional value of farmed fish and improve omega-3 content in seafood supply chains.

Explore more data points, trends and opportunities Download Free Sample Report

Omega-3 Fatty Acids EPA and DHA Market Segmentations

By Source

- Marine Source

- Algal Source

- Other Sources

By Form

- Triglyceride (TG) Form

- Ethyl Ester (EE) Form

- Re-esterified Triglyceride (rTG) Form

- Phospholipid Form

By Grade

- Nutraceutical Grade

- Pharmaceutical Grade

- Food & Beverage Grade

By Application

- Dietary Supplements

- Pharmaceuticals

- Infant Formula & Baby Nutrition

- Functional Foods & Beverages

- Animal Feed & Aquaculture

- Clinical Nutrition

By Distribution Channel

- Direct B2B Sales

- Retail Pharmacies

- Online Retail

- Specialty Nutrition Stores

- Institutional Supply

Regional Insights

North America

North America accounts for nearly 34% of the global omega-3 EPA and DHA market in 2025, with the United States contributing approximately 28% alone. The region’s leadership is supported by high dietary supplement penetration, strong prescription omega-3 adoption, and a well-established retail and e-commerce infrastructure. Rising cardiovascular disease prevalence, growing consumer preference for preventive healthcare, and advanced clinical research activities are key regional growth drivers. Canada demonstrates steady demand driven by public health awareness initiatives and increasing focus on aging population health management.

Europe

Europe holds approximately 29% of global market share, with Germany, the United Kingdom, France, Italy, and Spain representing major consumption centers. Strict European Union quality regulations and traceability standards support premium pricing and consumer trust. The region benefits from strong sustainability initiatives and clean-label product positioning. Norway plays a dual role as both a major consumption and production hub, leveraging advanced marine harvesting and refining technologies. Rising awareness regarding heart health and government-backed nutritional recommendations further drive demand across Western Europe.

Asia-Pacific

Asia-Pacific accounts for around 26% of global revenue and is the fastest-growing region, expanding at over 9.5% CAGR. China, Japan, India, South Korea, and Australia represent major markets. Rapid urbanization, rising disposable income, and expanding middle-class populations are significant growth drivers. Strong demand for infant formula fortified with DHA, increasing adoption of nutraceutical products, and expanding e-commerce platforms accelerate market expansion. Government initiatives promoting maternal and child health, along with growing awareness of lifestyle disease prevention, further strengthen regional growth prospects.

Latin America

Latin America contributes approximately 6% of the global market, led by Brazil and Mexico. Increasing supplement penetration, improving healthcare access, and rising urbanization support steady growth. Growing middle-class populations and expanding retail distribution networks enhance product accessibility. Additionally, the region benefits from proximity to key marine raw material sources, supporting regional trade and processing activities.

Middle East & Africa

The Middle East & Africa region holds nearly 5% of global market share, with the United Arab Emirates and South Africa driving demand. Rising health awareness, expanding premium supplement adoption, and increasing lifestyle-related disease prevalence support market growth. The development of organized retail channels and cross-border e-commerce platforms is improving product availability. Government healthcare diversification strategies and growing expatriate populations further contribute to rising omega-3 consumption across the region.

Key Players in the Omega-3 Fatty Acids EPA and DHA Market

- DSM-Firmenich

- BASF SE

- Croda International Plc

- Epax Norway AS

- GC Rieber Oils

- Pelagia AS

- Corbion NV

- KD Pharma Group

- Polaris

- Golden Omega SA

- Aker BioMarine ASA

- Omega Protein Corporation

- Cargill Inc.

- Lonza Group

- Nordic Naturals