Oligomeric Proanthocyanidins (OPC) Supplement Market Size

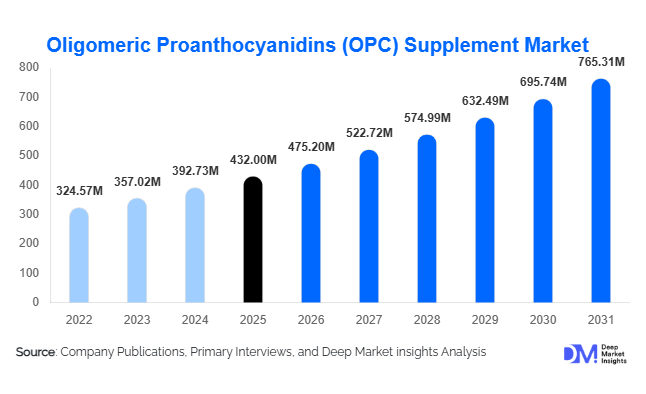

According to Deep Market Insights,the global oligomeric proanthocyanidins (OPC) supplement market size was valued at USD 432 million in 2025 and is projected to grow from USD 475.20 million in 2026 to reach USD 765.31 million by 2031, expanding at a CAGR of 10.0% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer awareness of antioxidant supplementation, increasing adoption of preventive healthcare practices, and growing demand for plant-based nutraceutical ingredients targeting cardiovascular, skin, and immune health. The expanding popularity of natural bioflavonoids and clinically supported botanical extracts is positioning OPC supplements as a premium category within the global dietary supplement industry.

Key Market Insights

- Preventive healthcare adoption is accelerating OPC supplement demand, particularly among aging populations seeking cardiovascular and anti-inflammatory support.

- Grape seed extract remains the dominant source, supported by abundant raw material availability and strong clinical validation.

- Online retail channels are reshaping global distribution, enabling direct-to-consumer brands to expand rapidly across regions.

- North America leads global consumption, supported by high supplement penetration and strong consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and expanding nutraceutical adoption in China, Japan, and India.

- Premiumization and standardized extracts with higher OPC purity levels are driving pricing growth and product differentiation.

What are the latest trends in the OPC supplement market?

Rise of Beauty-from-Within Supplements

One of the most prominent trends shaping the OPC supplement market is the rapid growth of ingestible beauty and nutricosmetics products. OPCs help protect collagen structures from oxidative stress, making them highly attractive for anti-aging, skin elasticity, and UV protection formulations. Supplement manufacturers are increasingly combining OPC extracts with collagen peptides, hyaluronic acid, and vitamins to develop multifunctional wellness solutions. This convergence between dietary supplements and skincare industries is expanding consumer demographics beyond traditional health users into beauty-focused consumers seeking holistic wellness outcomes.

Standardization and Clinical Validation of Botanical Extracts

Manufacturers are investing heavily in standardized OPC extracts with consistent polyphenol concentrations to enhance efficacy and regulatory compliance. Higher-purity extracts above 80% OPC content are gaining traction within premium product categories. Clinical trials demonstrating vascular health benefits and antioxidant efficacy are strengthening practitioner recommendations and enabling OPC supplements to move closer to medical nutrition positioning. This trend is increasing consumer trust and allowing brands to justify premium pricing strategies across developed markets.

What are the key drivers in the OPC supplement market?

Growing Demand for Natural Antioxidants

Consumers worldwide are shifting away from synthetic ingredients toward plant-derived nutraceuticals perceived as safer and more sustainable. OPC supplements, derived primarily from grape seeds and pine bark, align strongly with clean-label and natural health trends. Increasing awareness regarding oxidative stress and chronic disease prevention has significantly boosted antioxidant supplement consumption, driving sustained category expansion.

Expansion of Preventive Healthcare Culture

The global rise in cardiovascular diseases and lifestyle-related disorders is encouraging consumers to adopt preventive supplementation strategies. OPC compounds are associated with improved circulation, vascular elasticity, and anti-inflammatory benefits, making them increasingly popular among individuals aged 40 years and above. Healthcare practitioners are also recommending antioxidant supplementation as part of long-term wellness management, further strengthening market demand.

What are the restraints for the global market?

Variability in Extract Quality and Standardization

OPC concentration varies significantly depending on extraction methods and botanical sourcing, creating inconsistencies in product efficacy. Lack of uniform global standards increases regulatory scrutiny and creates challenges for smaller manufacturers attempting to maintain consistent quality benchmarks.

Limited Consumer Awareness Compared to Mainstream Supplements

Despite strong scientific backing, OPC supplements remain less recognized than vitamins, omega-3 fatty acids, or probiotics. Companies must invest heavily in consumer education and marketing to communicate benefits effectively, which can increase acquisition costs and slow adoption in price-sensitive markets.

What are the key opportunities in the OPC supplement industry?

Clinical Nutrition and Practitioner Channels

Increasing scientific validation presents opportunities to position OPC supplements within clinical nutrition markets. Companies investing in clinical trials and standardized formulations can expand into physician-recommended channels, improving credibility and enabling premium product positioning. Healthcare integration is expected to significantly enhance long-term adoption rates.

Personalized Nutrition Platforms

The rise of digital health ecosystems and subscription-based supplement models creates opportunities for personalized OPC supplementation programs. AI-driven wellness platforms are integrating antioxidant supplements into customized cardiovascular and longevity plans, increasing consumer retention and recurring revenue potential for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 432 Million |

| Market Size in 2026 | USD 475.20 Million |

| Market Size in 2031 | USD 765.31 Million |

| CAGR | 10% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Grape seed extract OPC dominates the global OPC supplement market, accounting for approximately 42% of total revenue in 2025. The segment’s leadership is primarily driven by the abundant availability of raw material derived from wine industry by-products, which ensures cost efficiency and consistent supply chains. Additionally, extensive clinical research supporting grape seed extract’s role in cardiovascular protection, antioxidant activity, and vascular health enhancement has strengthened consumer trust and manufacturer adoption. Its versatility across dietary supplements, functional foods, and nutricosmetic applications further reinforces market dominance. Pine bark extract represents the second-largest source segment and maintains strong positioning within premium formulations due to its high bioactive flavonoid concentration and association with branded, clinically validated ingredients. Increasing consumer preference for scientifically backed botanical extracts continues to support steady growth of both sources, while innovation in extraction technologies is improving bioavailability and product differentiation.

Purity Level Insights

Products standardized between 60–80% OPC concentration hold nearly 48% market share, making this the leading purity category due to its optimal balance between efficacy, affordability, and scalability for mass-market supplements. Manufacturers widely adopt this concentration range as it provides measurable health benefits while maintaining competitive pricing, thereby appealing to mainstream preventive healthcare consumers. These formulations are extensively used across cardiovascular, immune, and general wellness supplements. Meanwhile, high-purity extracts exceeding 80% OPC concentration are witnessing accelerated growth, particularly within premium and clinically positioned product lines. Rising consumer demand for potent, research-supported supplements and physician-recommended formulations is encouraging brands to invest in advanced purification processes. As consumer awareness of ingredient standardization increases, purity transparency and clinical validation are expected to remain key growth drivers across the segment.

Product Form Insights

Capsules lead the OPC supplement market with approximately 46% share, primarily driven by consumer preference for convenient consumption, accurate dosage control, and enhanced shelf stability. Capsules also enable efficient encapsulation of standardized botanical extracts without compromising potency, making them the preferred format among both manufacturers and healthcare-conscious consumers. Their compatibility with preventive health routines and daily supplementation habits further strengthens adoption. Softgels and tablets continue to maintain steady demand due to familiarity and ease of large-scale production, particularly in pharmacy retail channels. At the same time, powdered OPC supplements are gaining traction among fitness-oriented and lifestyle consumers seeking customizable dosing options and integration into functional beverages, smoothies, and sports nutrition products. Growing personalization trends in nutrition are expected to expand innovation across product forms.

Application Insights

Cardiovascular health applications represent the largest segment, accounting for nearly 34% of global demand, supported by increasing global prevalence of heart-related conditions and rising awareness regarding circulation support and oxidative stress management. OPC’s scientifically recognized benefits in improving vascular elasticity and supporting blood flow have positioned it as a core ingredient in heart health supplements, particularly among aging populations. Preventive healthcare adoption and physician-backed recommendations continue to drive consistent demand within this segment. Skin health and anti-aging applications are emerging as the fastest-growing category, fueled by expanding nutricosmetics trends and growing consumer interest in beauty-from-within solutions. The antioxidant and collagen-supporting properties of OPC are increasingly incorporated into skincare supplements targeting pigmentation control, skin elasticity, and photoprotection, contributing to rapid expansion across both developed and emerging markets.

Distribution Channel Insights

Online retail channels account for approximately 38% of global OPC supplement sales, making them the leading distribution platform as digital commerce reshapes consumer purchasing behavior. Growth is largely driven by increased access to product information, consumer reviews, personalized recommendations, and subscription-based purchasing models that enhance brand loyalty. Direct-to-consumer supplement brands leverage educational marketing strategies, influencer engagement, and targeted wellness campaigns to build trust and expand reach. Despite rapid e-commerce growth, pharmacies and health stores remain critical distribution channels for clinically positioned and practitioner-recommended products, particularly among older consumers who prioritize professional guidance and product credibility. Omni-channel retail strategies integrating online convenience with offline trust are becoming increasingly important for sustained market expansion.

Consumer Type Insights

Preventive healthcare consumers dominate the OPC supplement market with nearly 41% share, driven by growing awareness of long-term wellness management and increasing adoption of proactive health strategies. Rising healthcare costs and a global shift toward self-directed health maintenance encourage consumers to incorporate antioxidant supplements into daily routines. Aging populations represent a significant demand base due to heightened concerns regarding cardiovascular health, mobility, and cognitive longevity. Simultaneously, beauty-focused consumers are emerging as a rapidly expanding segment as anti-aging supplementation gains popularity within younger demographics influenced by wellness and aesthetic trends. The convergence of health optimization and beauty enhancement is reshaping consumer purchasing motivations, supporting diversified product innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Oligomeric Proanthocyanidins (OPC) Supplement Market Segmentations

By Source

- Grape Seed Extract OPC

- Pine Bark Extract OPC

- Cranberry Extract OPC

- Apple Extract OPC

- Cocoa & Other Botanical Sources

By Purity Level

- Below 40% OPC Content

- 40–60% OPC Content

- 60–80% OPC Content

- Above 80% OPC Content

By Product Form

- Capsules

- Tablets

- Softgels

- Powder Supplements

- Liquid Extracts

By Application

- Cardiovascular Health

- Skin Health & Anti-Aging

- Immune Support

- Anti-Inflammatory & Joint Health

- General Antioxidant Wellness

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Pharmacies & Drug Stores

- Health & Nutrition Specialty Stores

- Supermarkets & Hypermarkets

- Practitioner & Clinical Channels

By Consumer Type

- Preventive Healthcare Consumers

- Aging Population (40+ Years)

- Beauty & Nutricosmetic Consumers

- Sports & Active Lifestyle Users

Regional Insights

North America

North America accounts for approximately 34% of the global OPC supplement market, supported by high dietary supplement penetration and strong consumer awareness of antioxidant-based wellness products. The United States leads regional demand due to well-established nutraceutical distribution networks, advanced research infrastructure, and widespread preventive healthcare adoption. Increasing prevalence of lifestyle-related cardiovascular conditions continues to drive demand for circulation-support supplements, while premiumization trends encourage consumers to choose clinically validated botanical extracts. The region also benefits from strong e-commerce infrastructure, high disposable income, and growing demand for clean-label and plant-based supplements, all of which collectively sustain steady market expansion.

Europe

Europe holds nearly 28% market share, led by Germany, France, Italy, and the United Kingdom, where consumers strongly favor scientifically validated botanical ingredients. Regional growth is driven by strict regulatory frameworks emphasizing ingredient quality, traceability, and labeling transparency, which enhance consumer confidence in standardized OPC products. Increasing aging demographics and preventive cardiovascular care initiatives further stimulate demand. Additionally, Europe’s mature herbal supplement tradition and expanding nutricosmetic sector contribute to higher adoption of antioxidant-rich formulations. Premium product positioning and sustainability-focused sourcing practices also play a significant role in strengthening regional market growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 12% CAGR, fueled by rising health awareness, expanding middle-class populations, and rapid growth of the nutraceutical industry. China and Japan dominate demand due to strong cultural acceptance of functional supplements and rapidly aging populations seeking preventive health solutions. Increasing urbanization and digital retail penetration are accelerating product accessibility across the region. India is emerging as a high-potential market supported by expanding domestic manufacturing capabilities, cost-efficient production, and growing consumer awareness of herbal and plant-based supplements. Rising interest in beauty supplements and functional nutrition further strengthens long-term regional growth prospects.

Latin America

Latin America represents around 6% of global demand, with Brazil and Mexico leading adoption through expanding pharmacy networks and wellness retail channels. Regional growth is supported by improving middle-class purchasing power, increasing awareness of preventive healthcare, and gradual expansion of nutraceutical distribution infrastructure. Consumers are increasingly adopting antioxidant supplements to address lifestyle-related health concerns, while growing digital commerce platforms are improving product availability across urban markets. Local manufacturers are also contributing to market expansion by introducing affordable formulations tailored to regional price sensitivity.

Middle East & Africa

The Middle East & Africa account for nearly 4% market share, led by the UAE and South Africa, where rising urbanization and premium wellness trends are driving supplement adoption. Increasing consumer awareness regarding lifestyle diseases, combined with expanding pharmacy chains and specialty health stores, is supporting gradual market development. Growth is further encouraged by rising disposable income among urban populations and increasing demand for beauty and anti-aging supplements. Government initiatives promoting healthier lifestyles and expanding access to preventive healthcare solutions are expected to contribute to steady long-term market growth across the region.

Key Players in the OPC Supplement Market

- Givaudan (Naturex)

- Indena S.p.A.

- Nexira

- Euromed S.A.

- NOW Foods

- Swanson Health Products

- Life Extension

- Douglas Laboratories

- Herbalife Ltd.

- Blackmores Limited

- Amway Corporation

- Thorne HealthTech

- NutraMarks Inc.

- Nature’s Way Products LLC

- Solgar Inc.