Global Oats Market Size

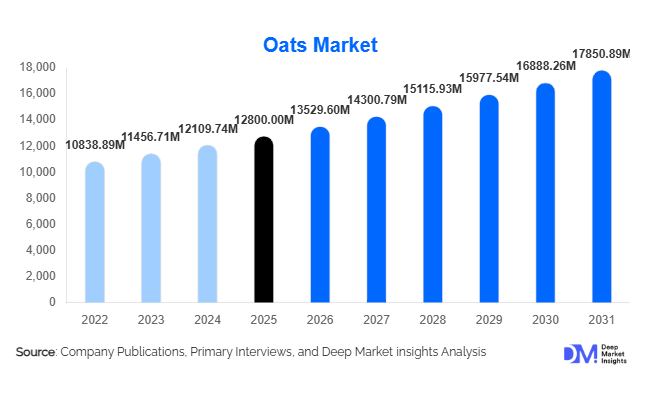

According to Deep Market Insights, the global oats market size was valued at USD 12,800 million in 2026 and is projected to grow from USD 13,529.60 million in 2027 to reach USD 16,850.89 million by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The oats market growth is primarily driven by increasing consumer preference for whole grain nutrition, rising demand for plant-based dairy alternatives such as oat milk, and growing adoption of functional foods rich in dietary fiber and beta-glucan.

Key Market Insights

- Oats are transitioning from a breakfast staple to a functional ingredient, widely used in bakery, dairy alternatives, and nutraceutical applications.

- Oat milk expansion is reshaping global demand dynamics, particularly in North America and Europe, where plant-based diets are accelerating.

- Europe dominates global consumption, supported by strong whole grain dietary habits and high organic product penetration.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and Western dietary influence.

- E-commerce channels are significantly expanding product accessibility, especially for premium and organic oat-based products.

- Functional food innovation is increasing, with oats being integrated into supplements, protein bars, and health-focused formulations.

Global oats market latest trends

Rise of Oat-Based Dairy Alternatives

The increasing adoption of plant-based lifestyles has significantly boosted demand for oat milk and oat-based yogurts. Consumers are shifting away from lactose-based dairy due to health, ethical, and environmental concerns. This has led manufacturers to invest in fortified oat beverages enriched with calcium, vitamins, and protein. The trend is particularly strong in urban centers across the United States, Germany, and China, where vegan and flexitarian diets are expanding rapidly. Oat milk has also gained traction in coffee chains and foodservice outlets, further strengthening its mainstream acceptance.

Functional and Clean-Label Product Innovation

Manufacturers are increasingly focusing on clean-label, non-GMO, and high-fiber oat products. Oats are being positioned as a core ingredient in heart health and digestive wellness formulations. Advanced processing technologies such as enzymatic treatment and micronization are improving texture, shelf life, and nutritional bioavailability. This trend is driving premiumization across oat-based product categories, particularly in health-focused retail segments and nutraceutical applications.

global oats market drivers

Rising Health Consciousness and Whole Grain Demand

Growing awareness of cardiovascular health and cholesterol management is significantly driving oat consumption. The presence of beta-glucan, a soluble fiber linked to heart health benefits, has strengthened oats’ positioning in preventive nutrition. Consumers are increasingly replacing refined grains with whole grain alternatives, boosting demand across breakfast cereals, bakery products, and snacks. This shift is especially strong in developed economies where diet-related lifestyle diseases are prevalent.

Expansion of Plant-Based Food Industry

The rapid growth of plant-based diets is a major driver for oats, particularly as a base ingredient for dairy alternatives. Oat milk has emerged as one of the fastest-growing non-dairy beverages globally. Food manufacturers are increasingly incorporating oats into vegan products such as yogurts, ice creams, and protein shakes. This expansion is also supported by foodservice chains integrating oat-based options into mainstream menus.

Retail Expansion and E-Commerce Growth

The growth of modern retail and online grocery platforms has significantly improved accessibility to oat-based products. E-commerce has enabled smaller and premium brands to reach wider audiences, while supermarkets continue to dominate mass distribution. Digital marketing and subscription-based nutrition models are further accelerating repeat consumption, particularly in urban markets.

global market restraints

Raw Material Price Volatility

Oat production is highly dependent on climatic conditions, making supply chains vulnerable to yield fluctuations. Weather variability in key producing regions such as Canada and Northern Europe can lead to price instability, affecting both manufacturers and end consumers. This volatility creates challenges in maintaining consistent profit margins for processed oat products.

Substitution from Alternative Grains

The oats market faces strong competition from alternative grains such as quinoa, barley, rice, and chia seeds. These substitutes are often marketed with similar or enhanced nutritional benefits, limiting oat penetration in certain health-conscious consumer segments. This competitive pressure restricts pricing power and slows expansion in niche health food categories.

global oats industry key opportunities

Expansion of Plant-Based Beverage Ecosystem

The oat milk segment presents one of the largest growth opportunities globally. Increasing vegan adoption and lactose intolerance awareness are driving demand across retail and foodservice channels. Premium fortified oat beverages with added nutrients are expected to generate strong revenue growth, particularly in North America, Europe, and urban Asia-Pacific markets.

Functional Food and Nutraceutical Integration

Oats are increasingly being used in dietary supplements, protein bars, and medical nutrition products due to their fiber content and cholesterol-lowering properties. This opens opportunities for high-margin product innovation in the health and wellness industry. The integration of oats into clinical nutrition and sports nutrition products is expected to expand significantly.

Government Nutrition Programs and Institutional Demand

Public health initiatives promoting whole grain consumption in schools, hospitals, and welfare programs are boosting institutional demand for oats. Governments in Europe and North America are actively encouraging fiber-rich diets, creating stable bulk procurement opportunities for manufacturers and suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12800.00 Million |

| Market Size in 2026 | USD 13529.60 Million |

| Market Size in 2031 | USD 17850.89 Million |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Rolled oats dominate the global oats market, accounting for approximately 34% of total market share in 2025, primarily due to their versatility, affordability, and ease of preparation across household and industrial food applications. The leading segment driver for rolled oats is their strong suitability for large-scale food processing and their widespread incorporation into breakfast cereals, granola bars, and ready-to-eat meals, making them a staple ingredient across both developed and emerging markets. Instant oats are witnessing rapid adoption, particularly in urban regions, driven by convenience-oriented lifestyles, increasing working populations, and growing demand for quick breakfast solutions that require minimal preparation time. Oat flour is expanding steadily as a key ingredient in bakery and gluten-free product formulations, supported by the rising prevalence of gluten intolerance awareness and the shift toward healthier baked goods. Steel-cut oats continue to serve a niche but premium segment of health-conscious consumers who prefer minimally processed foods with higher texture retention and slower digestion benefits. Oat bran is increasingly utilized in functional foods and dietary supplements, with its growth driven by strong demand for high-fiber ingredients linked to digestive health improvement and cholesterol management.

Application Insights

Breakfast cereals remain the largest application segment in the global oats market, supported by long-standing consumption habits in Western economies and the continued integration of oats into everyday morning diets. The leading growth driver for this segment is the sustained consumer preference for convenient, nutritious, and fiber-rich breakfast options that align with preventive health trends. Dairy alternatives, particularly oat milk, represent the fastest-growing application area, driven by rising lactose intolerance awareness, vegan dietary adoption, and strong expansion of plant-based beverage portfolios by global food and beverage manufacturers. Bakery and confectionery applications are also expanding steadily as manufacturers reformulate products to include healthier, whole-grain ingredients in response to growing consumer demand for low-fat and high-fiber baked goods. Nutraceutical and dietary supplement applications are gaining momentum due to the clinically recognized benefits of oats in cholesterol reduction and digestive health support, further strengthening their role in functional nutrition products. Animal feed applications remain relatively stable, supported by consistent demand in livestock nutrition, though their market share is comparatively smaller than human consumption segments.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the global distribution landscape for oats, accounting for the largest market share due to their extensive product variety, strong brand visibility, and consumer preference for one-stop shopping experiences. The leading driver for this channel is its ability to provide immediate product accessibility along with promotional pricing and bundled offerings that encourage higher volume purchases. Online retail is emerging as the fastest-growing distribution channel, fueled by increasing digital penetration, evolving consumer shopping behavior, subscription-based delivery models, and the convenience of home delivery, particularly in urban areas. Specialty health stores play a crucial role in distributing premium, organic, and functional oat-based products, driven by rising consumer willingness to pay for clean-label and health-focused food items. Foodservice channels are also expanding steadily, particularly through the growing adoption of oat milk in cafés, quick-service restaurants, and specialty beverage outlets, where plant-based alternatives are becoming a standard menu offering.

Explore more data points, trends and opportunities Download Free Sample Report

Oats Market Segmentations

By Product Type

- Whole Oats

- Steel-Cut Oats

- Rolled Oats

- Instant/Quick Oats

- Oat Flour

- Oat Bran

By Nature

- Conventional Oats

- Organic Oats

By Processing Level

- Minimally Processed Oats

- Moderately Processed Oats

- Highly Processed Oats

By Application

- Breakfast Cereals

- Bakery & Confectionery

- Dairy Alternatives

- Nutraceuticals & Dietary Supplements

- Infant Nutrition

- Animal Feed

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail / E-commerce

- Specialty Health Stores

- Convenience Stores

- Foodservice & Institutional Supply

Regional Insights

Europe

Europe holds the largest share of the global oats market at approximately 38% in 2025, driven by deeply rooted dietary habits such as porridge consumption and strong demand for breakfast cereals across countries including Germany, the United Kingdom, Finland, and Sweden. The primary growth driver in the region is the high consumer preference for organic, natural, and minimally processed food products, supported by stringent food quality regulations and strong health awareness. Additionally, the well-established retail infrastructure and widespread acceptance of plant-based diets further reinforce Europe’s dominant position in the global market.

North America

North America accounts for approximately 32% of the global oats market, with the United States serving as the largest consumption hub. Market growth in the region is primarily driven by the rapid expansion of oat milk and other plant-based dairy alternatives, alongside increasing consumer adoption of health-conscious and fiber-rich diets. Strong retail penetration and continuous product innovation by food manufacturers also contribute significantly to regional expansion. Canada plays a dual role as both a major consumer and one of the world’s leading oat producers, further strengthening North America’s supply chain advantage.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, led by China, India, Japan, and Australia. The key growth drivers in this region include rapid urbanization, rising disposable incomes, and increasing exposure to Western dietary habits, which are collectively accelerating the adoption of oat-based foods and beverages. Expanding health awareness among younger populations and growing demand for convenient packaged breakfast solutions are also contributing to strong market momentum. Furthermore, the entry of international brands and expansion of e-commerce platforms are improving product availability across both urban and semi-urban areas.

Latin America

Latin America is experiencing moderate but steady growth in the oats market, with Brazil and Mexico emerging as the primary demand centers. The main growth driver in the region is the gradual shift toward healthier eating habits, supported by increasing awareness of the nutritional benefits of whole grains and dietary fiber. Rising penetration of breakfast cereals and expanding modern retail networks are also enhancing product accessibility, thereby supporting sustained market development across urban populations.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth in the oats market, largely driven by import-dependent supply structures and increasing health consciousness among consumers. The leading growth driver in this region is the rising demand for premium, functional, and fortified food products, particularly in high-income Gulf countries such as the UAE and Saudi Arabia. Strong retail expansion, coupled with growing interest in Western dietary patterns and plant-based nutrition, is further supporting market penetration, especially in urban centers.

Key Players in the Global Oats Market

- General Mills

- Kellogg Company

- Quaker Oats Company

- Cargill

- Archer Daniels Midland Company

- Grain Millers Inc.

- Richardson International

- Blue Lake Milling

- Bob’s Red Mill

- Ardent Mills

- Morning Foods

- Bauck GmbH

- Avena Foods

- Bagrry’s India

- Ralston Foods