Oat Product Market Size

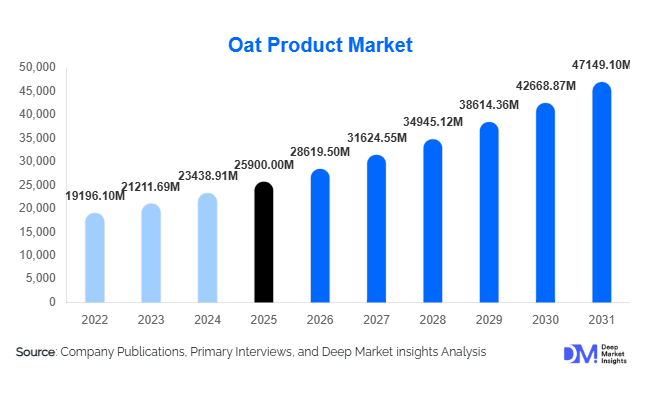

According to Deep Market Insights, the global oat product market size was valued at USD 25,900 million in 2025 and is projected to grow from USD 28,619.50 million in 2026 to reach USD 47,149.10 million by 2031, expanding at a CAGR of 10.5% during the forecast period (2026–2031). The oat product market growth is primarily driven by increasing consumer preference for plant-based nutrition, rising demand for high-fiber functional foods, and the rapid expansion of oat-based dairy alternatives such as oat milk.

Key Market Insights

- Oat-based beverages are transforming the plant-based dairy segment, driven by their creamy texture, sustainability profile, and allergen-friendly positioning.

- Health-conscious consumption patterns are accelerating demand, with oats recognized for their beta-glucan content and heart health benefits.

- North America dominates the global market, supported by strong innovation, high consumer awareness, and premium product adoption.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable income, and increasing dietary diversification.

- Retail expansion and e-commerce growth are enhancing product accessibility across emerging markets.

- Technological advancements in processing are improving taste, texture, and shelf life, boosting consumer acceptance globally.

What are the latest trends in the oat product market?

Rise of Plant-Based Oat Beverages

Oat milk and oat-based beverages have emerged as one of the fastest-growing segments within the global plant-based food industry. Consumers are increasingly shifting away from dairy due to lactose intolerance, environmental concerns, and vegan lifestyles. Oat milk offers a balanced taste profile and superior frothing capability, making it highly popular in coffee applications and foodservice channels. Manufacturers are introducing fortified variants enriched with calcium, vitamins, and protein, further enhancing their appeal. The growing presence of oat milk in cafes, quick-service restaurants, and retail shelves is significantly contributing to overall market expansion.

Expansion of Functional and Clean-Label Products

The demand for clean-label and functional foods is reshaping product innovation in the oat market. Consumers are actively seeking products with minimal processing, natural ingredients, and clear health benefits. Oat-based products enriched with fiber, protein, and probiotics are gaining traction across both developed and emerging markets. Additionally, gluten-free certifications and organic labeling are becoming key purchase drivers. Manufacturers are investing in advanced processing technologies to retain nutritional value while improving taste and texture, aligning with evolving consumer expectations.

What are the key drivers in the oat product market?

Growing Health Awareness and Functional Food Demand

The increasing prevalence of lifestyle diseases such as cardiovascular disorders and diabetes has led consumers to adopt healthier dietary habits. Oats, being rich in beta-glucan, are scientifically associated with cholesterol reduction and improved heart health. This has significantly boosted their inclusion in daily diets, particularly in breakfast cereals, snacks, and dietary supplements. The global shift toward preventive healthcare is expected to sustain long-term demand for oat-based products.

Rapid Adoption of Plant-Based Diets

The global transition toward plant-based diets is a major driver of the oat product market. Consumers are increasingly choosing plant-based alternatives for ethical, environmental, and health reasons. Oats serve as a versatile ingredient in dairy alternatives, bakery products, and ready-to-eat meals. The expansion of vegan and flexitarian populations across North America, Europe, and Asia-Pacific is accelerating market growth, encouraging manufacturers to diversify their product offerings.

What are the restraints for the global market?

Raw Material Price Volatility

The supply of oats is highly dependent on climatic conditions and agricultural yields, leading to fluctuations in raw material prices. This volatility can impact production costs and profit margins, particularly for manufacturers operating in price-sensitive markets. Weather-related disruptions and supply chain challenges further exacerbate pricing instability.

Intense Competition from Alternative Plant-Based Products

The oat product market faces strong competition from other plant-based alternatives such as almond, soy, and coconut-based products. These alternatives have established consumer bases and extensive distribution networks, which can limit market penetration for oat-based offerings in certain regions. Continuous innovation and differentiation are required to maintain competitive advantage.

What are the key opportunities in the oat product industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Brazil present significant growth opportunities for oat products. Rising health awareness, increasing disposable income, and rapid urbanization are driving demand for nutritious and convenient food options. Governments promoting healthier diets and the expansion of modern retail infrastructure are further supporting market penetration. Localization of products and pricing strategies will be critical for capturing these markets.

Growth in Nutraceutical and Functional Applications

Oats are increasingly being used in nutraceuticals and functional food products due to their high fiber and antioxidant content. The extraction of beta-glucan for use in dietary supplements and functional beverages is gaining traction. This presents opportunities for premium product development and higher profit margins. Companies investing in R&D to develop innovative oat-based formulations can tap into this high-growth segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 25900.00 Million |

| Market Size in 2026 | USD 28619.50 Million |

| Market Size in 2031 | USD 47149.10 Million |

| CAGR | 10.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Oat-based beverages have emerged as the dominant product category in the global oat market, accounting for approximately 32% of the global market share in 2025. This leadership position is strongly supported by the accelerating shift toward plant-based diets and the growing intolerance and sensitivity to lactose among global consumers. Oat milk, in particular, has become a preferred dairy alternative due to its creamy texture, neutral taste profile, and strong compatibility with coffee, smoothies, and ready-to-drink formulations. The rapid expansion of coffee chains and specialty cafés integrating oat milk into their standard offerings has further reinforced demand across both developed and emerging economies. Additionally, sustainability considerations are playing a critical role, as oat cultivation requires significantly less water compared to almond and dairy production, making it a more environmentally attractive choice for conscious consumers.Oatmeal products, including instant oats, rolled oats, and steel-cut variants, continue to maintain a substantial share within the product landscape due to their long-standing presence in traditional breakfast consumption habits. The convenience factor associated with instant oats has significantly increased their penetration among urban working populations, particularly in fast-paced economies. Furthermore, growing awareness regarding heart health, cholesterol management, and weight control has reinforced oatmeal consumption as a staple dietary choice recommended by nutritionists globally.Meanwhile, oat-based snacks and bakery products represent a rapidly expanding sub-segment, driven primarily by younger consumers seeking convenient yet nutritious snacking alternatives. Product innovation in this category, including oat cookies, energy bars, granola clusters, and fortified baked goods, is reshaping consumer perception of oats from a basic breakfast ingredient to a versatile functional food component. The increasing incorporation of protein enrichment, fiber fortification, and clean-label positioning in these products is further enhancing their appeal in the health-focused snacking market.

Processing Type Insights

Conventional oat products dominate the market with approximately 68% share, largely driven by their affordability, mass production capabilities, and extensive global availability. Conventional processing methods allow manufacturers to achieve economies of scale, making oat-based products accessible across a wide consumer base. The strong presence of established supply chains and large-scale agricultural production in North America and Europe continues to support this segment’s dominance. Additionally, conventional oats are widely integrated into both retail and industrial food manufacturing, ensuring consistent demand across multiple end-use applications.However, the organic oat segment is witnessing significantly faster growth, propelled by rising consumer awareness regarding food safety, pesticide exposure, and overall dietary quality. Organic oats are increasingly associated with clean-label positioning, non-GMO certification, and chemical-free cultivation practices, which resonate strongly with health-conscious and environmentally aware consumers. The premium pricing structure of organic oat products has also contributed to higher value generation despite lower volume penetration. Furthermore, regulatory support for organic farming practices in several regions, along with expanding certification frameworks, is expected to further accelerate growth in this segment over the forecast period.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape, accounting for nearly 45% of the global market share. This dominance is primarily attributed to strong product visibility, extensive shelf space allocation, and the convenience of one-stop shopping experiences. Consumers often prefer physical retail environments when purchasing staple food items such as oats, as it allows them to compare brands, packaging sizes, and pricing structures directly. Retailers also actively promote oat-based products through in-store promotions and health-focused marketing campaigns, further driving sales volume.At the same time, online retail channels are emerging as the fastest-growing distribution segment, supported by rapid digital transformation and increasing penetration of e-commerce platforms. The convenience of home delivery, subscription-based models, and attractive discounts has significantly shifted consumer purchasing behavior, especially in urban areas. The COVID-19 pandemic accelerated this transition, and the trend has continued due to sustained consumer preference for digital grocery shopping. Additionally, direct-to-consumer brands specializing in health foods are leveraging online platforms to expand their reach without relying heavily on traditional retail infrastructure.

Application Insights

The food and beverages application segment dominates the global oat market with more than 70% share, reflecting the widespread integration of oats into daily dietary consumption. Oats are extensively used in breakfast cereals, dairy alternatives, bakery products, snacks, and functional beverages. The increasing demand for nutrient-dense, high-fiber foods has significantly contributed to the expansion of oat-based food applications. Moreover, product innovation within the food and beverage industry, particularly in plant-based formulations, has further enhanced the versatility of oats as a core ingredient.Beyond food and beverages, oats are increasingly being utilized in personal care and nutraceutical applications. In personal care, oat extracts are widely recognized for their soothing, anti-inflammatory, and moisturizing properties, making them a popular ingredient in skincare formulations such as lotions, creams, and cleansers. In the nutraceutical segment, oats are being incorporated into dietary supplements and functional health products due to their beta-glucan content, which is associated with cholesterol reduction and improved cardiovascular health. The diversification of application areas is expected to significantly strengthen long-term market growth by expanding oats beyond traditional food categories.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 52% of the global market. This dominance is largely driven by the increasing incorporation of oats into daily breakfast routines, rising health consciousness, and growing awareness of preventive nutrition. Consumers are actively shifting toward high-fiber, low-fat dietary options, positioning oats as a staple food in many households. The ease of preparation, affordability, and long shelf life of oat products further enhance their suitability for household consumption.The commercial food processing industry represents the fastest-growing end-use segment, fueled by the expanding integration of oats into packaged foods, ready-to-eat meals, and functional ingredients. Food manufacturers are increasingly leveraging oats to enhance the nutritional profile of their products while meeting consumer demand for healthier alternatives. The rise of convenience foods, combined with innovation in product formulation, is expected to further drive industrial consumption of oats. Additionally, the foodservice sector, including cafés, bakeries, and quick-service restaurants, is increasingly incorporating oat-based ingredients to cater to evolving dietary preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Oat Product Market Segmentations

By Product Type

- Oatmeal

- Oat-Based Beverages

- Oat Bakery Products

- Oat Snacks

- Oat Ingredients

By Application

- Food & Beverages

- Animal Feed

- Personal Care & Cosmetics

- Nutraceuticals & Dietary Supplements

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Health Stores

- Foodservice

Regional Insights

North America

North America holds approximately 35% of the global market share in 2025, making it the largest regional market for oat products. The United States is the primary contributor to regional growth, driven by high consumer awareness regarding health and nutrition, as well as the widespread adoption of plant-based diets. The strong presence of established brands, advanced food processing infrastructure, and well-developed retail networks are key factors supporting market expansion.One of the primary growth drivers in North America is the rapid rise in demand for dairy alternatives, particularly oat milk, which has gained significant popularity due to its taste and environmental benefits. Additionally, increasing incidences of lactose intolerance and growing vegan populations are further boosting demand. Continuous product innovation, including fortified and flavored oat beverages, is enhancing consumer engagement. The region also benefits from strong marketing strategies and high investment in research and development by major companies, which is driving product diversification and premiumization.

Europe

Europe accounts for around 30% of the global market share, with countries such as the United Kingdom, Germany, and Sweden leading demand. The region’s strong emphasis on sustainability and environmental responsibility is a major driver of oat product adoption. Consumers in Europe are increasingly shifting toward plant-based diets, supported by government initiatives promoting sustainable food consumption.The presence of innovative companies such as :contentReference[oaicite:11]{index=11} has significantly contributed to the growth of the oat beverage segment in Europe. Additionally, stringent regulations regarding food quality and labeling are encouraging the production of high-quality oat products. The growing demand for organic and clean-label foods is further accelerating market growth. Europe’s well-established retail infrastructure and increasing penetration of private-label oat products are also contributing to the expansion of the market.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a CAGR exceeding 12%, driven by rapid urbanization, rising disposable incomes, and increasing awareness of healthy dietary habits. Countries such as China and India are key markets, where changing lifestyles and growing middle-class populations are fueling demand for convenient and nutritious food products.The expansion of modern retail formats, including supermarkets, hypermarkets, and e-commerce platforms, is significantly enhancing product accessibility across the region. Additionally, the increasing influence of Western dietary patterns and the rising popularity of plant-based diets are driving the adoption of oat-based products. Government initiatives promoting healthy eating and nutritional awareness are further supporting market growth. Local manufacturers are also entering the market with affordable product offerings, intensifying competition and expanding consumer reach.

Latin America

Latin America is witnessing steady growth, particularly in countries such as Brazil and Mexico. The increasing awareness of health and wellness, coupled with the rising prevalence of lifestyle-related diseases, is encouraging consumers to incorporate oats into their diets. The growing availability of oat products through expanding retail networks is further supporting market growth.Additionally, the region is benefiting from the increasing influence of global food trends, including the demand for plant-based and functional foods. The entry of international brands and the expansion of local manufacturers are enhancing product availability and diversity. Economic development and improving consumer purchasing power are also contributing to the gradual expansion of the oat products market in this region.

Middle East & Africa

The Middle East and Africa region is gradually emerging as a promising market for oat products, with demand primarily concentrated in urban areas. Increasing awareness of healthy eating habits and the growing influence of Western diets are key drivers of market growth. The rising prevalence of chronic diseases such as obesity and diabetes is encouraging consumers to adopt healthier food options, including oats.The expansion of retail infrastructure, including supermarkets and online platforms, is improving product accessibility across the region. Additionally, government initiatives aimed at promoting food security and nutrition are supporting market development. While the market is still in its early stages compared to other regions, increasing investments by international companies and the growing popularity of health-focused products are expected to drive future growth.

Key Players in the Oat Product Market

- Nestlé S.A.

- PepsiCo, Inc.

- General Mills, Inc.

- Kellogg Company

- Danone S.A.

- Oatly Group AB

- The Quaker Oats Company

- Bob’s Red Mill Natural Foods

- Grain Millers, Inc.

- Blue Diamond Growers

- Califia Farms

- Hain Celestial Group

- Nature’s Path Foods

- Marico Limited

- ITC Limited