Oat Beta Glucan Market Size

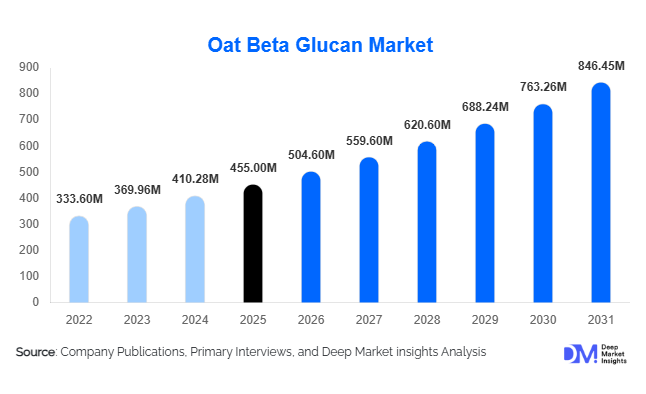

According to Deep Market Insights,the global oat beta glucan market size was valued at USD 455 million in 2025 and is projected to grow from USD 504.60 million in 2026 to reach USD 846.45 million by 2031, expanding at a CAGR of 10.9% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer demand for clinically validated functional ingredients, increasing adoption of heart-health and metabolic wellness products, and expanding applications of soluble dietary fibers across food, nutraceutical, pharmaceutical, and personal care industries. Growing awareness regarding preventive healthcare, combined with regulatory approvals supporting cholesterol-lowering health claims, has accelerated product incorporation into mainstream functional foods and dietary supplements globally.

Key Market Insights

- Functional foods remain the dominant application, accounting for more than half of global demand as manufacturers reformulate products with fiber enrichment and clean-label positioning.

- Powdered oat beta glucan leads product adoption due to superior stability, ease of formulation, and compatibility across food and supplement applications.

- North America dominates global consumption, supported by strong nutraceutical penetration and regulatory-backed health claims.

- Asia-Pacific is the fastest-growing region, driven by expanding middle-class populations and rising preventive healthcare awareness.

- Nutraceutical applications are generating premium margins, supported by consumer willingness to pay for clinically supported wellness ingredients.

- Technological advancements in extraction and purification are improving yield efficiency and enabling high-purity pharmaceutical-grade ingredients.

What are the latest trends in the oat beta glucan market?

Shift Toward Preventive Nutrition and Functional Fortification

Consumers worldwide are increasingly prioritizing preventive health solutions, driving strong adoption of functional ingredients with scientifically validated benefits. Oat beta glucan is gaining traction as manufacturers fortify everyday foods such as cereals, bakery products, dairy alternatives, and beverages to meet dietary fiber intake recommendations. Food brands are repositioning staple products as heart-health solutions, allowing oat beta glucan to transition from niche nutraceutical usage to large-scale food applications. Clean-label trends further reinforce adoption, as consumers prefer recognizable plant-derived ingredients over synthetic additives. Regulatory acceptance of cholesterol-reduction claims has strengthened consumer trust, encouraging multinational food companies to integrate oat beta glucan into reformulated product portfolios.

Advancements in High-Purity Extraction Technologies

Technological innovation is reshaping production economics and expanding application possibilities. Manufacturers are investing in enzymatic extraction and advanced filtration processes that improve beta glucan concentration while maintaining functional performance. High-purity (>70%) variants are increasingly used in pharmaceutical nutrition and medical foods, where consistency and bioactivity are critical. Improved processing efficiency is lowering production costs and enabling wider commercialization in emerging markets. Sustainability-focused processing technologies that reduce water and energy consumption are also becoming industry priorities, aligning with ESG procurement requirements among global food and ingredient companies.

What are the key drivers in the oat beta glucan market?

Rising Prevalence of Cardiovascular and Metabolic Disorders

Increasing incidence of lifestyle-related diseases such as obesity, diabetes, and cardiovascular disorders is driving demand for functional dietary fibers. Oat beta glucan’s scientifically demonstrated ability to lower LDL cholesterol and regulate glycemic response has positioned it as one of the most trusted functional ingredients globally. Healthcare professionals and nutrition organizations increasingly recommend fiber-enriched diets, supporting long-term demand growth across both developed and emerging markets.

Growth of Clean-Label and Plant-Based Food Innovation

The global shift toward plant-based nutrition has accelerated adoption of oat-derived ingredients. Oat beta glucan aligns with vegan, non-GMO, and minimally processed product claims, making it attractive to food manufacturers targeting health-conscious consumers. Plant-based dairy alternatives and functional beverages increasingly incorporate beta glucan to enhance texture while delivering nutritional benefits, further strengthening market expansion.

What are the restraints for the global market?

Raw Material Price Volatility

The market remains sensitive to fluctuations in oat crop yields influenced by climate variability and agricultural supply disruptions. Changes in raw material pricing directly impact production costs and ingredient pricing stability, creating challenges for manufacturers operating under long-term supply contracts.

Formulation and Sensory Challenges

Incorporating high fiber concentrations into food products can alter viscosity, taste, and texture profiles. Manufacturers often require additional research and development investment to maintain product sensory quality, which can slow adoption among smaller food producers with limited formulation expertise.

What are the key opportunities in the oat beta glucan industry?

Expansion in Personalized Nutrition Platforms

Personalized nutrition ecosystems supported by digital health monitoring are creating new demand channels for targeted functional ingredients. Oat beta glucan’s measurable impact on cholesterol and blood sugar management makes it well suited for subscription-based wellness programs and customized dietary solutions. Companies integrating ingredient offerings with digital health platforms can develop differentiated premium products supported by data-driven health outcomes.

Emerging Market Penetration and Local Manufacturing

Rapid urbanization and increasing disposable incomes across Asia-Pacific and Latin America present significant growth opportunities. Local production facilities supported by government food innovation initiatives can reduce supply chain costs and improve regional accessibility. Expansion into emerging economies is expected to drive long-term volume growth as awareness of preventive nutrition rises among middle-income consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 455 Million |

| Market Size in 2026 | USD 504.60 Million |

| Market Size in 2031 | USD 846.45 Million |

| CAGR | 10.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The powdered form represents the leading segment in the global oat beta glucan market, accounting for approximately 58% of total demand. The dominance of powdered oat beta glucan is primarily driven by its superior stability, extended shelf life, and operational flexibility across large-scale food and nutraceutical manufacturing processes. Manufacturers favor powdered formats because they enable efficient dry blending, uniform dispersion in cereal and bakery formulations, and reduced logistics costs compared to liquid alternatives. In addition, powders allow precise dosage standardization, which is critical for functional claims and regulatory compliance. Liquid concentrates continue to witness steady adoption in ready-to-drink beverages, dairy alternatives, and functional smoothies where rapid solubility and instant dispersion are essential. Granular formats serve niche industrial applications requiring controlled hydration during processing, particularly in extrusion and specialized food manufacturing. Encapsulated oat beta glucan extracts are emerging as a premium category within nutraceutical formulations, supported by rising demand for controlled-release delivery systems, improved bioavailability, and targeted health outcomes in high-value supplement products.

Purity Level Insights

The 30%–70% purity segment holds the leading share of global consumption, accounting for nearly 46% of the market, driven by its optimal balance between functional efficacy and cost efficiency. This purity range enables large-scale incorporation into fortified foods and beverages without significantly increasing formulation costs, making it highly attractive to food processors and functional ingredient manufacturers. The segment’s growth is further supported by increasing demand for fiber enrichment solutions that meet regulatory health claim thresholds while maintaining product affordability. High-purity variants exceeding 70% beta glucan content are experiencing accelerated growth as clinical nutrition, pharmaceutical-grade supplements, and medical foods require higher bioactivity and standardized functional performance. These products are increasingly utilized in cholesterol management formulations, metabolic health products, and immune-support applications, where scientifically validated efficacy plays a decisive role in purchasing decisions. Lower-purity formats remain relevant in bulk food fortification but are gradually losing share as manufacturers shift toward higher functional concentration products to differentiate offerings.

Application Insights

Functional food and beverage applications constitute the leading segment, representing approximately 52% of global demand, primarily driven by the growing integration of oat beta glucan into everyday dietary products. The segment’s expansion is supported by rising consumer preference for preventive nutrition, clean-label ingredients, and scientifically supported health benefits such as cholesterol reduction and glycemic control. Oat beta glucan is increasingly incorporated into breakfast cereals, bakery goods, nutritional beverages, snack bars, and plant-based dairy alternatives, allowing manufacturers to enhance nutritional profiles while maintaining product taste and texture. Dietary supplements represent the fastest-growing application area, fueled by increasing global awareness of immune health, cardiovascular wellness, and metabolic disease prevention. Pharmaceutical nutrition applications are gaining momentum as healthcare systems emphasize medical nutrition therapy for aging populations and chronic disease management. Meanwhile, cosmetic and personal care applications are emerging as innovative growth areas, leveraging oat beta glucan’s anti-inflammatory, moisturizing, and skin barrier repair properties for advanced dermatological and anti-aging formulations.

Distribution Channel Insights

B2B ingredient supply remains the dominant distribution channel, accounting for nearly 68% of total market revenues, largely driven by bulk procurement practices among multinational food processors, nutraceutical companies, and pharmaceutical nutrition manufacturers. Long-term supply agreements ensure consistent ingredient quality, cost optimization, and supply chain reliability, which are critical for large-scale production environments. The expansion of contract formulation and private-label manufacturing services is further strengthening B2B demand, as emerging health brands increasingly outsource research, development, and production activities to specialized ingredient partners. Retail and e-commerce channels are gradually expanding their presence as smaller manufacturers, independent supplement formulators, and health-focused consumers gain access to functional ingredients in smaller quantities. Digital platforms are enabling ingredient transparency, direct sourcing, and global accessibility, contributing to the gradual diversification of distribution strategies across the industry.

End-Use Industry Insights

The nutraceutical industry represents the leading value-generating end-use segment, accounting for approximately 34% of total demand in 2025. Growth in this segment is primarily driven by premium product positioning, strong consumer trust in functional supplements, and increasing clinical validation of oat beta glucan’s health benefits. Nutraceutical manufacturers benefit from higher margins associated with targeted health claims related to cardiovascular health, immune modulation, and metabolic wellness. The food processing industry remains the largest volume consumer, supported by widespread fortification initiatives and growing demand for healthier everyday food products. Pharmaceutical nutrition applications are expanding rapidly as aging demographics and rising chronic disease prevalence encourage adoption of medically supported dietary interventions. Additionally, cosmetics and personal care companies are increasingly incorporating oat beta glucan into skincare formulations, capitalizing on consumer demand for natural, soothing, and scientifically backed bioactive ingredients.

Explore more data points, trends and opportunities Download Free Sample Report

Oat Beta Glucan Market Segmentations

By Product Form

- Powder

- Liquid Concentrates

- Granules

- Encapsulated Extracts

By Purity Level

- Below 30% Beta Glucan

- 30%–70% Beta Glucan

- Above 70% Beta Glucan

By Application

- Functional Food & Beverages

- Dietary Supplements

- Pharmaceuticals & Medical Nutrition

- Personal Care & Cosmetics

By Distribution Channel

- B2B Ingredient Supply

- Contract Manufacturing & Formulation Services

- Retail & E-commerce Ingredient Sales

By End-Use Industry

- Food Processing Industry

- Nutraceutical Industry

- Pharmaceutical Industry

- Cosmetics & Personal Care Industry

Regional Insights

North America

North America accounted for approximately 34% of the global oat beta glucan market in 2025, led by strong demand across the United States and Canada. Regional growth is driven by high consumer awareness of dietary fiber benefits, widespread adoption of functional supplements, and established regulatory frameworks supporting heart-health claims associated with beta glucan consumption. The presence of advanced food innovation ecosystems, strong collaboration between ingredient suppliers and research institutions, and well-developed oat cultivation infrastructure ensures consistent raw material availability. Additionally, rising healthcare costs are encouraging preventive nutrition adoption, while increasing demand for clean-label and plant-based foods continues to accelerate incorporation of oat-derived functional ingredients across mainstream product categories.

Europe

Europe held nearly 29% of the global market share, supported by strong consumption across Germany, the United Kingdom, France, and Nordic countries. Regional growth is driven by long-standing dietary preferences for fiber-rich foods, robust regulatory endorsement of health claims, and advanced oat processing technologies concentrated in Scandinavian nations. Sustainability-focused food innovation, circular agriculture practices, and consumer preference for natural ingredients are further strengthening market expansion. The region’s strong plant-based food movement, combined with increasing demand for cholesterol-lowering functional ingredients, continues to support widespread adoption of oat beta glucan across bakery, dairy alternatives, and clinical nutrition applications.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR exceeding 13%, fueled by rapid urbanization, rising disposable incomes, and increasing preventive healthcare awareness. China leads regional demand through aggressive innovation in functional beverages and fortified convenience foods, while Japan’s aging population significantly drives adoption in medical nutrition and senior wellness products. India is emerging as a high-potential growth market due to expanding nutraceutical manufacturing capabilities, growing middle-class health consciousness, and increasing government emphasis on preventive healthcare. The expansion of modern retail infrastructure and digital commerce platforms further enhances accessibility of functional nutrition products across the region.

Latin America

Latin America represents a developing yet promising market led by Brazil and Mexico, where demand for fortified foods and wellness supplements is steadily increasing. Regional growth is supported by rising awareness of obesity and cardiovascular health concerns, encouraging consumers to shift toward functional dietary solutions. Improvements in retail penetration, expansion of international nutraceutical brands, and growing investment in local food processing industries are facilitating wider adoption of oat beta glucan ingredients. Increasing urbanization and evolving dietary patterns are also contributing to gradual but sustained market expansion.

Middle East & Africa

The Middle East & Africa region remains an emerging market, with growth concentrated in the United Arab Emirates and South Africa. Market expansion is driven by rising disposable incomes, increasing demand for premium imported health products, and growing awareness of preventive nutrition among urban populations. Expansion of modern retail chains, healthcare-driven wellness initiatives, and increasing penetration of dietary supplements are supporting adoption of functional ingredients. Additionally, the region’s growing expatriate population and evolving consumer lifestyles are encouraging demand for scientifically supported nutrition solutions, positioning oat beta glucan as a valuable ingredient within premium functional food and supplement categories.

Key Players in the Oat Beta Glucan Market

- Tate & Lyle PLC

- Kerry Group plc

- DSM-Firmenich

- Cargill Incorporated

- Swedish Oat Fiber AB

- Lantmännen Biorefineries

- Givaudan (Naturex Division)

- Garuda International Inc.

- Ceapro Inc.

- Avena Foods Limited

- Fazer Group

- IFF Health

- Biovelop International AB

- Suzhou NutraMax

- Ingredion Incorporated