Nutraceutical Ingredients Market Size

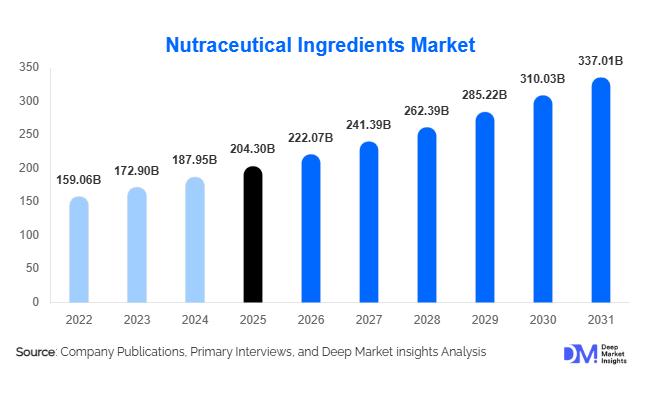

According to Deep Market Insights, the global nutraceutical ingredients market size was valued at USD 204.3 billion in 2025 and is projected to grow from USD 222.07 billion in 2026 to reach USD 337.01 billion by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). The nutraceutical ingredients market growth is primarily driven by rising preventive healthcare awareness, increasing demand for functional foods and beverages, rapid expansion of dietary supplements, and growing consumer preference for plant-based and clean-label bioactive compounds. Aging global populations, higher disposable incomes in emerging economies, and advancements in ingredient extraction and fermentation technologies are further accelerating long-term market expansion.

Key Market Insights

- Dietary supplements represent the largest application segment, accounting for nearly 38% of total ingredient demand in 2025, driven by immunity, gut health, and cardiovascular support products.

- Vitamins remain the leading ingredient category, contributing approximately 28% of global revenue in 2025 due to their broad integration across food, beverage, and supplement formats.

- Plant-based nutraceutical ingredients account for over 40% of the market, reflecting strong clean-label and sustainability trends.

- North America holds the largest regional share, representing about 34% of the global market in 2025, led by the United States.

- Asia-Pacific is the fastest-growing region, expanding at close to 10% CAGR, supported by rising middle-class income and preventive healthcare adoption.

- Top five companies collectively control nearly 33% of the global market, indicating moderate consolidation with strong competition in specialty bioactives.

What are the latest trends in the nutraceutical ingredients market?

Personalized and Precision Nutrition

The nutraceutical ingredients industry is increasingly aligned with personalized nutrition models. Consumers are leveraging microbiome testing, wearable health monitoring devices, and digital health platforms to select customized supplement formulations. Ingredient manufacturers are responding by offering modular blends and clinically validated bioactives that can be tailored to age, lifestyle, and health conditions. This trend is encouraging innovation in microencapsulation, controlled-release formats, and synergistic nutrient combinations, enabling higher efficacy and targeted performance claims.

Plant-Based and Fermentation-Derived Ingredients

Plant-based proteins, botanical extracts, and algae-derived omega-3 fatty acids are gaining strong traction. Fermentation-derived vitamins, amino acids, and probiotics are also expanding due to cost efficiency and scalability. Sustainable sourcing, non-GMO certifications, and traceability systems are becoming key procurement criteria for global food and supplement brands. This shift is reshaping supply chains and driving investment in microbial fermentation facilities worldwide.

What are the key drivers in the nutraceutical ingredients market?

Rising Preventive Healthcare Spending

Consumers globally are shifting toward preventive health strategies to reduce long-term medical costs. Growing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and obesity is encouraging routine consumption of fortified foods and supplements. Governments and healthcare institutions are also supporting nutritional fortification programs, strengthening ingredient demand.

Expansion of Functional Food and Beverage Industry

Functional beverages, protein-enriched snacks, fortified dairy alternatives, and ready-to-drink nutrition formats are witnessing robust growth. Beverage manufacturers are incorporating vitamins, probiotics, fibers, and botanical extracts to differentiate products. This high-volume incorporation significantly boosts bulk ingredient procurement.

Technological Advancements in Extraction and Bioavailability

Innovations in supercritical extraction, encapsulation, and enzyme-assisted processing are enhancing ingredient stability and absorption rates. Improved bioavailability allows brands to use optimized dosages, supporting premium pricing strategies and improving consumer trust in efficacy claims.

What are the restraints for the global market?

Regulatory Complexity and Compliance Costs

Different regulatory frameworks across North America, Europe, and Asia create approval challenges for ingredient manufacturers. Health claim substantiation, labeling requirements, and safety validations increase time-to-market and operational expenses.

Raw Material Price Volatility

Botanical extracts, fish oil, specialty minerals, and agricultural commodities are subject to seasonal and geopolitical fluctuations. Supply chain disruptions can compress margins, particularly for small and mid-sized ingredient producers operating in competitive pricing environments.

What are the key opportunities in the nutraceutical ingredients industry?

Emerging Market Manufacturing Expansion

Countries such as India, China, Brazil, and Indonesia are investing heavily in domestic nutraceutical production under initiatives like Make in India and Made in China 2025. Local manufacturing reduces import dependency and enhances export competitiveness, creating long-term growth opportunities.

Clinical and Medical Nutrition Integration

The integration of nutraceutical ingredients into clinical nutrition and hospital-based dietary protocols presents high-value opportunities. Ingredients targeting immune support, recovery nutrition, and metabolic management are increasingly used in therapeutic nutrition formulations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 204.3 Billion |

| Market Size in 2026 | USD 222.07 Billion |

| Market Size in 2031 | USD 337.01 Billion |

| CAGR | 8.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Ingredient Type Insights

Vitamins continue to dominate the global nutraceutical ingredients market, accounting for approximately 28% of total market share in 2025. The leadership of vitamins is primarily driven by their extensive incorporation across dietary supplements, fortified foods, functional beverages, and clinical nutrition formulations. Growing consumer emphasis on immunity enhancement, bone health, and overall wellness—particularly post-pandemic—has significantly strengthened demand for vitamin D, vitamin C, and B-complex ingredients. In addition, regulatory approvals for fortification programs in developing economies and expanding preventive healthcare awareness have reinforced vitamins as the leading ingredient segment.

Probiotics and plant-based proteins are emerging as some of the fastest-growing ingredient categories. Probiotics are witnessing strong adoption due to rising awareness regarding gut microbiome health, digestive balance, and immunity support, alongside increasing clinical validation of strain-specific benefits. Meanwhile, plant-based proteins are expanding rapidly as veganism, flexitarian diets, and sustainability considerations reshape global consumption patterns. Omega fatty acids and botanical extracts also represent high-growth segments, supported by increasing cardiovascular health concerns, cognitive wellness focus, and consumer preference for natural and traditional plant-derived solutions. Technological advancements in extraction, encapsulation, and bioavailability enhancement further strengthen growth prospects across these ingredient categories.

Application Insights

Dietary supplements represent the largest application segment, contributing nearly 38% of total market demand in 2025. The segment’s leadership is primarily driven by increasing self-directed health management, aging populations, rising disposable income, and growing availability of personalized nutrition solutions. Expanding e-commerce distribution channels and direct-to-consumer brands have further improved accessibility, enabling broader product penetration across developed and emerging markets.

Functional foods and beverages collectively account for over 30% of the global market, supported by continuous innovation in fortified snacks, dairy alternatives, energy drinks, and ready-to-drink nutrition products. Consumers increasingly prefer convenient, on-the-go nutrition formats that seamlessly integrate health benefits into daily diets. Sports and performance nutrition is expanding rapidly, particularly in emerging economies where urbanization, gym culture, and youth fitness trends are accelerating demand. Infant nutrition and clinical nutrition segments continue to demonstrate steady institutional demand, supported by hospital procurement, pediatric fortification programs, and medical nutrition therapy applications.

Form Insights

Powdered ingredients account for approximately 46% of the global market, making them the leading form segment. Their dominance is driven by ease of formulation blending, longer shelf life, cost-effective bulk manufacturing, and compatibility with large-scale food and beverage production. Powders are particularly preferred in protein supplements, meal replacements, and industrial premix applications, enhancing their widespread adoption.

Capsules and softgels maintain strong market presence within the supplement delivery segment due to precise dosing, enhanced stability of sensitive ingredients, and established consumer trust in pharmaceutical-style formats. Gummies are experiencing rapid growth, supported by consumer preference for palatable, convenient, and easy-to-consume dosage forms. The increasing availability of sugar-free, plant-based, and functional gummy formulations is further broadening their consumer base, particularly among millennials and pediatric populations.

Source Insights

Plant-based ingredients hold around 41% of total market revenue in 2025, reflecting a structural shift toward natural, sustainable, and clean-label products. Consumer concerns regarding synthetic additives, coupled with environmental awareness and ethical sourcing considerations, are driving demand for botanical extracts, plant proteins, and algae-derived omega fatty acids. The growing influence of vegan and vegetarian lifestyles across North America, Europe, and Asia-Pacific continues to strengthen plant-based ingredient adoption.

Microbial and fermentation-based sources are gaining prominence for amino acids, enzymes, probiotics, and specialty bioactives. Advances in biotechnology and precision fermentation are enabling scalable, cost-efficient, and highly consistent production processes. These methods also support improved bioavailability and purity standards, making them increasingly attractive for pharmaceutical-grade and clinical nutrition applications.

Explore more data points, trends and opportunities Download Free Sample Report

Nutraceutical Ingredients Market Segmentations

By Ingredient Type

- Vitamins

- Minerals

- Amino Acids

- Proteins & Peptides

- Omega Fatty Acids

- Probiotics & Prebiotics

- Carotenoids

- Botanical Extracts & Phytochemicals

- Fibers & Specialty Carbohydrates

- Enzymes

By Source

- Plant-Based

- Animal-Based

- Microbial/Fermentation-Based

- Synthetic

By Form

- Powder

- Liquid

- Capsules & Softgels

- Granules

- Gummies

Application

- Dietary Supplements

- Functional Food

- Functional Beverages

- Infant Nutrition

- Clinical Nutrition

- Sports & Performance Nutrition

- Animal Nutrition

By Distribution Channel

- Direct to Manufacturers

- Contract Manufacturing Organizations (CMOs)

- Online B2B Platforms

Regional Insights

North America

North America accounts for approximately 34% of the global nutraceutical ingredients market in 2025, making it the largest regional market. The United States alone represents nearly 28% of global demand, supported by high dietary supplement penetration, strong consumer spending on wellness products, and a well-established regulatory framework that encourages product innovation while maintaining safety standards. Growth drivers in the region include rising adoption of personalized nutrition, increasing preventive healthcare expenditure, expansion of sports nutrition consumption, and strong presence of leading nutraceutical manufacturers. Canada contributes significantly through clean-label product innovation, plant-based formulation development, and growing consumer preference for sustainable sourcing practices.

Europe

Europe holds approximately 27% of the global market share, led by Germany, France, Italy, and the United Kingdom. Germany represents the largest consumer base within the region due to its strong herbal supplement traditions, advanced research capabilities, and stringent quality standards. Regional growth is driven by increasing demand for clinically validated formulations, regulatory emphasis on product safety and traceability, and rising awareness regarding preventive healthcare among aging populations. Sustainability initiatives, organic certification programs, and consumer demand for ethically sourced botanical extracts further contribute to market expansion across Western and Northern Europe.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at nearly 10% CAGR, supported by rapid urbanization, growing middle-class income, and rising healthcare awareness. China and India serve as major growth engines due to expanding domestic manufacturing capabilities, favorable government initiatives promoting nutraceutical production, and increasing consumer inclination toward preventive health solutions. Additionally, traditional medicine systems in the region provide a strong foundation for botanical ingredient integration. Japan and South Korea represent mature yet innovation-driven markets, characterized by high product sophistication, functional beverage innovation, and strong demand for anti-aging and beauty-from-within nutraceutical formulations.

Latin America

Latin America accounts for roughly 7% of global demand, with Brazil and Mexico leading regional consumption. Growth in the region is supported by expanding sports nutrition markets, increasing demand for fortified foods, and improving retail infrastructure. Rising obesity rates and lifestyle-related health concerns are encouraging greater adoption of functional ingredients, particularly proteins, vitamins, and omega fatty acids. Economic stabilization efforts and increasing foreign investment in food processing and supplement manufacturing further enhance regional market potential.

Middle East & Africa

The Middle East & Africa region is experiencing steady expansion, led by the United Arab Emirates, Saudi Arabia, and South Africa. Growth drivers include rising urbanization, expanding healthcare infrastructure, increasing awareness of preventive health practices, and higher disposable income levels in Gulf Cooperation Council countries. The region is witnessing growth in ingredient imports as well as local blending and packaging operations, supported by government diversification initiatives aimed at strengthening domestic food and pharmaceutical manufacturing capabilities. Increasing demand for halal-certified nutraceutical ingredients also contributes to regional market development.

Key Players in the Nutraceutical Ingredients Market

- DSM-Firmenich

- BASF SE

- Cargill Incorporated

- Archer Daniels Midland Company

- Kerry Group

- Ingredion Incorporated

- Givaudan

- Evonik Industries AG

- Lonza Group

- Chr. Hansen Holding

- Glanbia plc

- International Flavors & Fragrances Inc.

- Roquette Frères

- Ajinomoto Co., Inc.

- DuPont de Nemours, Inc.