Nutraceutical Excipients Market Size

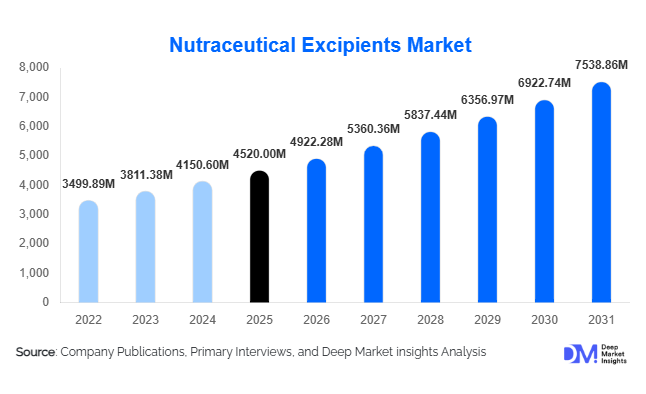

According to Deep Market Insights,the global nutraceutical excipients market size was valued at USD 4,520 million in 2025 and is projected to grow from USD 4,922.28 million in 2026 to reach USD 7,538.86 million by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The nutraceutical excipients market growth is primarily driven by the rapid expansion of the global dietary supplements industry, increasing consumer preference for preventive healthcare, and rising demand for innovative dosage formats such as gummies, chewables, softgels, and functional powders. As nutraceutical manufacturers focus on improving product stability, taste masking, bioavailability, and shelf life, the importance of high-performance excipients has significantly increased across formulation pipelines.

Key Market Insights

- Fillers and diluents represent the largest functionality segment, accounting for nearly 28% of the 2025 market, supported by high-volume tablet and capsule production.

- Tablets dominate formulation types with approximately 32% market share in 2025, owing to cost efficiency and global consumer acceptance.

- Dietary supplements account for nearly 48% of total demand, driven by expanding vitamin, mineral, and herbal supplement consumption.

- North America leads the global market with around 34% share in 2025, supported by strong supplement penetration and regulatory standardization.

- Asia-Pacific is the fastest-growing region, projected to expand at over 10% CAGR due to rising middle-class health awareness in China and India.

- Clean-label and plant-based excipients are gaining traction, particularly in Europe and North America, as brands shift toward natural ingredient positioning.

What are the latest trends in the nutraceutical excipients market?

Shift Toward Clean-Label and Plant-Based Excipients

Manufacturers are increasingly developing plant-derived binders, natural disintegrants, and non-GMO stabilizers to align with clean-label positioning. Consumer scrutiny over ingredient transparency is influencing supplement brands to replace synthetic excipients with botanical or cellulose-based alternatives. This shift is especially prominent in Europe and North America, where regulatory emphasis on traceability and allergen-free formulations is stronger. Plant-based excipients derived from starch, cellulose, and natural gums are witnessing double-digit growth, reshaping procurement strategies across contract manufacturers.

Growth of Advanced Dosage Formats

The expansion of gummies, chewables, orally disintegrating tablets, and effervescent powders is significantly influencing excipient innovation. These formats require advanced flavoring systems, moisture-resistant coatings, and multifunctional binding agents. Gummies in particular are driving demand for specialized sweeteners, gelling agents, and stabilizers, especially in pediatric and adult wellness segments. As consumer experience becomes a competitive differentiator, excipient suppliers are investing in co-processed and multifunctional systems to enhance manufacturability and sensory performance.

What are the key drivers in the nutraceutical excipients market?

Rapid Expansion of the Global Dietary Supplements Industry

The global dietary supplements industry, valued at over USD 180 billion in 2025, continues to expand at more than 8% annually. This directly increases demand for excipients across tablets, capsules, softgels, and powders. Rising awareness around immunity, bone health, digestive wellness, and sports nutrition is fueling production volumes, thereby increasing excipient consumption per formulation batch.

Technological Advancements in Multifunctional Excipients

Co-processed excipients combining binding, lubrication, and disintegration properties are gaining popularity. These systems reduce manufacturing complexity, enhance compressibility, and improve cost efficiency for large-scale supplement producers. Advanced spray-drying, granulation, and blending technologies are also supporting higher-quality excipient production.

What are the restraints for the global market?

Raw Material Price Volatility

Fluctuations in cellulose, starch derivatives, gelatin, and natural gum prices significantly affect production costs. Agricultural dependency and global supply chain disruptions increase cost unpredictability, impacting profit margins and pricing strategies.

Regulatory Variability Across Regions

Nutraceutical classification differs globally, with some countries regulating supplements under food laws and others imposing quasi-pharmaceutical standards. This regulatory inconsistency increases compliance complexity and documentation burdens for excipient suppliers operating internationally.

What are the key opportunities in the nutraceutical excipients industry?

Expansion in Emerging Manufacturing Hubs

Countries such as India, China, and Brazil are investing heavily in domestic nutraceutical production. Industrial initiatives promoting local manufacturing are creating opportunities for excipient companies to establish regional production facilities and reduce import dependency. Export-oriented supplement manufacturing is further driving demand for globally compliant excipients.

Specialized Delivery Systems for Sports and Geriatric Nutrition

The rapid growth of sports nutrition and aging populations worldwide is creating demand for tailored excipient systems that enhance bioavailability and taste masking. High-protein supplements, joint-health formulations, and cognitive wellness products require innovative stabilizers and solubilizers, offering high-margin opportunities for excipient innovators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4520 Million |

| Market Size in 2026 | USD 4922.28 Million |

| Market Size in 2031 | USD 7538.86 Million |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

By functionality, fillers and diluents dominate the nutraceutical excipients market, contributing approximately 28% of the global share in 2025. The leading segment driver for fillers and diluents is their indispensable role in ensuring uniform dosage weight, stability, and compressibility across almost every tablet and capsule formulation. As global supplement production volumes continue to expand, manufacturers rely heavily on these excipients to maintain formulation consistency, cost efficiency, and scalable production. Binders and disintegrants hold the next significant share, supported primarily by rising tablet manufacturing and the need to achieve optimal mechanical strength while ensuring rapid dissolution and bioavailability.

Lubricants and coating agents are gaining increasing importance as controlled-release, enteric-coated, and moisture-sensitive nutraceutical products become more prevalent. The expansion of probiotic, omega-3, and herbal formulations that require enhanced stability and shelf life is accelerating demand for advanced coating systems and anti-adherent technologies. Flavoring and sweetening agents are emerging as high-growth categories, driven by the rapid expansion of gummy, chewable, and effervescent supplement formats. The leading driver for this segment is consumer preference for palatable, convenient dosage forms that improve compliance, particularly among pediatric and geriatric populations.

Application Insights

Dietary supplements remain the largest application segment, accounting for nearly 48% of overall demand in 2025. The leading driver for this segment is the sustained global shift toward preventive healthcare and self-medication, supported by increasing consumer awareness of immunity, cardiovascular health, and overall wellness. The rapid proliferation of vitamins, minerals, herbal extracts, probiotics, and omega-3 products continues to generate substantial excipient demand across multiple dosage forms.

Functional foods and beverages represent expanding application areas, particularly due to fortification trends in dairy alternatives, energy drinks, protein bars, and ready-to-drink nutrition products. The integration of nutraceutical ingredients into mainstream food matrices requires specialized stabilizers, emulsifiers, and texturizing excipients, supporting segment growth. Sports nutrition is among the fastest-growing applications, driven by increasing gym memberships, performance-focused lifestyles, and rising demand for protein powders, amino acid blends, and hydration products. Pediatric and geriatric nutraceutical formulations are also expanding steadily, generating demand for taste-masking systems, sugar-free sweeteners, and easy-to-consume formats such as liquids, dispersible tablets, and gummies.

Formulation Insights

Tablets lead the formulation segment with approximately 32% market share in 2025. The leading driver for tablet dominance is their cost-effectiveness, manufacturing efficiency, longer shelf life, and suitability for high-volume production. Tablets also allow for precise dosing and compatibility with a broad range of excipients, making them the preferred choice for multivitamins and mineral supplements. Capsules and softgels maintain substantial shares, supported by consumer preference for easy swallowing, faster disintegration, and enhanced bioavailability for oil-based or sensitive active ingredients.

Gummies and chewables are the fastest-growing formulation category, expanding at double-digit rates through 2031. The primary growth driver for this segment is the rising demand for convenient, flavorful, and visually appealing supplements that improve consumer adherence. This trend significantly increases the need for gelling agents, stabilizers, sweeteners, and moisture-control excipients to maintain texture, taste, and product stability throughout shelf life.

Explore more data points, trends and opportunities Download Free Sample Report

Nutraceutical Excipients Market Segmentations

By Functionality

- Fillers & Diluents

- Binders

- Disintegrants

- Coating Agents

- Lubricants & Glidants

- Flavoring & Sweetening Agents

- Preservatives & Stabilizers

- Emulsifiers & Solubilizers

By Formulation Type

- Tablets

- Capsules

- Softgels

- Gummies & Chewables

- Powders & Sachets

- Liquid Formulations

By Source

- Synthetic Excipients

- Natural & Plant-Based Excipients

- Animal-Derived Excipients

By End-Use Application

- Dietary Supplements

- Functional Foods

- Functional Beverages

- Sports Nutrition

- Pediatric Nutraceuticals

- Geriatric Nutraceuticals

Regional Insights

North America

North America accounts for nearly 34% of the global nutraceutical excipients market in 2025, with the United States representing the majority share and Canada contributing steady growth. Regional growth is primarily driven by high dietary supplement penetration rates, strong consumer spending on preventive healthcare, and well-established contract manufacturing organizations. Advanced regulatory oversight, sophisticated supply chains, and continuous product innovation further strengthen demand. The expansion of clean-label, plant-based, and allergen-free supplement formulations is also accelerating the adoption of specialized excipients across the region.

Europe

Europe holds approximately 27% market share in 2025, led by Germany, France, Italy, and the United Kingdom. Regional growth is supported by stringent quality standards, harmonized regulatory frameworks, and increasing demand for clean-label and plant-derived excipients. Consumers in the region demonstrate strong preference for transparency, sustainability, and traceability, prompting manufacturers to adopt natural binders, non-GMO fillers, and organic-certified ingredients. Additionally, the region’s aging population and rising focus on preventive nutrition are contributing to steady expansion in nutraceutical production volumes.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at a CAGR exceeding 10% through 2031. China and India serve as major growth engines due to rising disposable incomes, expanding middle-class populations, increasing domestic supplement manufacturing, and supportive government industrial policies. Rapid urbanization and heightened health awareness following global public health events have significantly boosted supplement consumption. Japan and South Korea represent mature, innovation-driven markets characterized by advanced formulation technologies and strong demand for functional foods and premium nutraceutical products. The region’s expanding contract manufacturing base further accelerates excipient demand.

Latin America

Brazil and Mexico are leading demand centers within Latin America. Regional growth is driven by increasing awareness of preventive healthcare, expanding retail and e-commerce supplement penetration, and growing adoption of sports nutrition products. Rising urbanization and improving healthcare access are encouraging consumers to invest in vitamins and immunity-boosting products, thereby strengthening demand for cost-effective and multifunctional excipients suitable for large-scale production.

Middle East & Africa

The United Arab Emirates and South Africa are key markets within the Middle East & Africa region. Growth is supported by rapid urbanization, expanding middle-income populations, and increasing premium supplement consumption. The rising presence of international nutraceutical brands, combined with improving regulatory structures and distribution networks, is fostering gradual but consistent market expansion. Demand for halal-certified and clean-label formulations is also influencing excipient selection and procurement strategies across the region.

Key Players in the Nutraceutical Excipients Market

- BASF SE

- Evonik Industries AG

- Roquette Frères

- Ashland Global Holdings Inc.

- DuPont de Nemours, Inc.

- Croda International Plc

- Colorcon Inc.

- Associated British Foods Plc

- Kerry Group Plc

- Innophos Holdings Inc.

- SPI Pharma Inc.

- Wacker Chemie AG

- DFE Pharma

- JRS Pharma

- Cargill Incorporated