Non-GMO Soybean Market Size

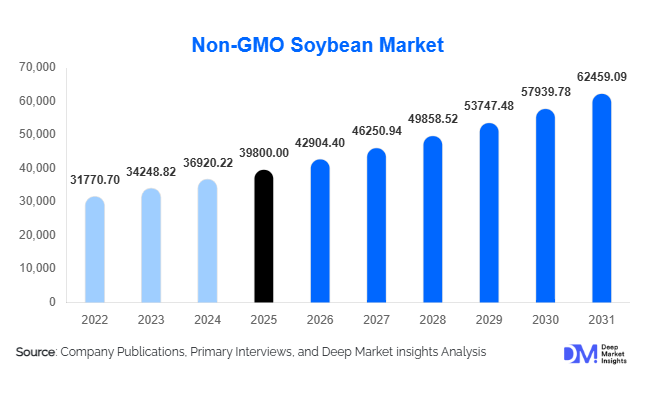

According to Deep Market Insights, the global non-GMO soybean market size was valued at USD 39,800 million in 2025 and is projected to grow from USD 42,904.40 million in 2026 to reach USD 61,459.09 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). The non-GMO soybean market growth is primarily driven by rising consumer demand for clean-label food products, increasing adoption of plant-based diets, and stringent regulatory frameworks supporting non-GMO labeling across key markets such as Europe and Asia.

Key Market Insights

- Growing preference for clean-label and non-GMO certified products is driving demand across food and beverage applications globally.

- Animal feed remains the dominant application, accounting for nearly 46% of total market demand due to high protein requirements.

- North America leads the global market, supported by strong consumer awareness and established non-GMO supply chains.

- Asia-Pacific is the fastest-growing region, driven by rising demand from China, Japan, and India.

- Premium pricing of 10–20% over GMO soybeans continues to incentivize farmers and producers.

- Traceability and identity preservation systems are becoming critical for market competitiveness and export compliance.

What are the latest trends in the non-GMO soybean market?

Rising Demand for Plant-Based Protein Products

The global surge in plant-based diets has significantly increased the demand for non-GMO soy protein, particularly in meat substitutes, dairy alternatives, and functional foods. Consumers are increasingly seeking sustainable protein sources, and non-GMO soybeans offer a balance of nutritional value and clean-label assurance. Food manufacturers are actively reformulating products to include non-GMO soy ingredients, especially in regions with strict labeling regulations. This trend is further supported by the expansion of vegan and flexitarian populations, particularly in North America and Europe.

Adoption of Traceability and Identity Preservation Systems

Supply chain transparency has become a key trend in the non-GMO soybean market. Companies are investing in advanced traceability systems, including blockchain and digital tracking, to ensure product authenticity and compliance with non-GMO certifications. These systems help maintain segregation from GMO crops throughout the supply chain, enhancing trust among consumers and buyers. The adoption of such technologies is particularly strong in export-oriented markets where regulatory scrutiny is high, enabling suppliers to secure premium contracts and long-term partnerships.

What are the key drivers in the non-GMO soybean market?

Increasing Consumer Awareness and Clean-Label Demand

Rising awareness regarding food safety and health concerns associated with genetically modified organisms has led to a strong shift toward non-GMO products. Consumers are increasingly prioritizing transparency in food labeling, which has prompted manufacturers to adopt non-GMO soybeans as a key ingredient. This driver is particularly prominent in developed markets, where regulatory frameworks support non-GMO labeling and certification.

Expansion of Plant-Based Food Industry

The rapid growth of the plant-based food sector is a major driver for the non-GMO soybean market. Soy protein remains one of the most widely used plant-based protein sources due to its high protein content and versatility. The increasing popularity of meat substitutes, soy milk, and protein-enriched foods has significantly boosted demand for non-GMO soybeans, especially among health-conscious and environmentally aware consumers.

What are the restraints for the global market?

Higher Production and Segregation Costs

Non-GMO soybean production requires strict segregation from GMO crops, leading to increased costs in cultivation, transportation, and storage. Certification and traceability requirements further add to operational expenses, making non-GMO soybeans more expensive than conventional alternatives. This price differential can limit adoption, particularly in cost-sensitive markets.

Limited Availability Compared to GMO Soybeans

The global soybean market is dominated by GMO variants, which account for a significant share of production. This creates supply constraints for non-GMO soybeans, making it difficult for large-scale manufacturers to secure consistent volumes. Limited availability also contributes to price volatility, posing challenges for long-term procurement strategies.

What are the key opportunities in the non-GMO soybean industry?

Expansion of Export-Oriented Production

Emerging economies such as Brazil and India are increasingly focusing on non-GMO soybean cultivation to cater to premium export markets in Europe and Asia. Government support through subsidies, certification programs, and export incentives is enabling farmers to expand production. This export-driven growth presents significant opportunities for both producers and traders to tap into high-value international markets.

Growth of Organic Non-GMO Segment

The organic non-GMO soybean segment is gaining traction as consumers become more health-conscious and environmentally aware. Organic certification adds further value to non-GMO products, allowing producers to command higher prices. This niche segment is expected to grow rapidly, particularly in developed markets where demand for organic food products is strong.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 39800 Million |

| Market Size in 2026 | USD 42904.40 Million |

| Market Size in 2031 | USD 62459.09 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The non-GMO soybean market is characterized by a diverse product portfolio, with non-GMO soybean meal emerging as the dominant segment, accounting for approximately 34% of the global market share in 2025. This dominance is primarily driven by its critical role in animal nutrition, where it serves as a high-protein, cost-effective feed ingredient for poultry, swine, and aquaculture industries. The rising global demand for high-quality animal protein has significantly increased the consumption of soybean meal, particularly in emerging economies where livestock production is expanding rapidly. Additionally, the digestibility and amino acid profile of soybean meal make it an indispensable component in commercial feed formulations, reinforcing its leading position within the product segment.Whole non-GMO soybeans also play a significant role, particularly in global trade, where they are exported for both direct consumption and further processing. Countries with limited domestic production rely heavily on imports of whole soybeans to meet their processing and feed requirements. The versatility of soybeans as a raw agricultural commodity ensures sustained demand across multiple end-use industries. Overall, the product segment is being shaped by a combination of nutritional demand, industrial versatility, and the growing shift toward clean-label and non-GMO-certified food systems, which continues to elevate the importance of non-GMO soy products in the global agricultural and food value chain.

Application Insights

The application landscape of the non-GMO soybean market is largely dominated by the animal feed segment, which contributes approximately 46% of the total market share. This leadership position is underpinned by the essential role of soy-derived ingredients in livestock nutrition. The increasing global consumption of meat, dairy, and aquaculture products has created sustained demand for protein-rich feed ingredients, with non-GMO soybean meal serving as a primary input. The leading driver for this segment is the expansion of industrial livestock farming, particularly in Asia-Pacific and Latin America, where rising incomes and urbanization are driving dietary shifts toward animal-based protein consumption.Industrial applications, although currently representing a smaller share, are emerging as a promising growth avenue. Non-GMO soybeans are increasingly being utilized in the production of biodiesel, bioplastics, and other bio-based materials. The leading driver for this segment is the global push toward renewable energy and sustainable industrial practices. Governments and organizations worldwide are implementing policies to reduce carbon emissions and promote the use of bio-based alternatives, thereby creating new opportunities for non-GMO soybean utilization. As sustainability continues to gain importance across industries, the industrial application segment is expected to witness steady expansion over the forecast period.

Distribution Channel Insights

The distribution landscape of the non-GMO soybean market is predominantly led by direct sales channels, which account for nearly 52% of the market. This dominance is largely attributed to the procurement preferences of large-scale buyers, including feed manufacturers, food processors, and industrial users, who typically engage in long-term contracts with producers and suppliers. The leading driver for this segment is the need for supply chain reliability, price stability, and quality assurance, which are critical factors for bulk purchasers operating at scale.In recent years, online and retail distribution channels have started gaining prominence, particularly for specialty non-GMO products and smaller-scale buyers. The rise of digital platforms has enabled greater market transparency and accessibility, allowing buyers to source certified non-GMO products with ease. The increasing penetration of e-commerce and digital marketplaces is expected to further transform the distribution landscape, especially in developed markets where technological adoption is high. Although still a relatively smaller segment, the growth of online channels reflects a broader shift toward decentralized and consumer-driven procurement models.

Cultivation Type Insights

Conventional non-GMO soybeans currently dominate the cultivation type segment, holding approximately 68% of the total market share. This dominance is primarily driven by their widespread availability, established farming practices, and relatively lower production costs compared to organic variants. Farmers often prefer conventional non-GMO cultivation due to its higher yield potential and reduced certification requirements, making it a more economically viable option in large-scale agricultural operations. The leading driver for this segment is the balance between cost efficiency and compliance with non-GMO standards, which allows producers to cater to both domestic and international markets.The cultivation segment is also influenced by regulatory frameworks, certification standards, and international trade policies, which play a critical role in shaping production practices and market dynamics. As sustainability and traceability become increasingly important, both conventional and organic non-GMO cultivation systems are expected to evolve to meet the changing demands of consumers and regulatory bodies.

End-Use Industry Insights

The food processing industry represents the largest end-use segment, accounting for approximately 38% of the total market share. This segment’s dominance is driven by the extensive use of non-GMO soy ingredients in a wide range of processed food products, including snacks, bakery items, beverages, and plant-based alternatives. The leading driver for this segment is the rapid expansion of the plant-based food industry, which relies heavily on soy protein as a key ingredient due to its nutritional profile and functional versatility.The biofuel industry is also gaining importance as a consumer of non-GMO soybeans, particularly in the production of biodiesel. The increasing focus on renewable energy sources and government incentives for biofuel production are expected to drive demand from this segment. Overall, the end-use landscape is being shaped by a combination of health trends, sustainability initiatives, and industrial innovation, which collectively contribute to the expanding applications of non-GMO soy products.

Explore more data points, trends and opportunities Download Free Sample Report

Non-GMO Soybean Market Segmentations

By Product Type

- Whole Non-GMO Soybeans

- Non-GMO Soybean Meal

- Non-GMO Soybean Oil

- Non-GMO Soy Protein

- Non-GMO Soy Flour

By Application

- Food & Beverages

- Animal Feed

- Industrial Applications

By Distribution Channel

- Direct Sales

- Agricultural Cooperatives

- Commodity Traders

- Online & Retail Channels

Regional Insights

North America

North America holds a significant share of approximately 32% of the global non-GMO soybean market, with the United States leading production and consumption. The region benefits from advanced agricultural infrastructure, high adoption of modern farming techniques, and well-established supply chains that ensure consistent quality and availability. A key growth driver in North America is the strong consumer awareness regarding non-GMO and clean-label products, which has led to increased demand for certified non-GMO soy ingredients in both food and feed applications. Additionally, the rapid growth of the plant-based food industry, supported by innovation and investment, is further accelerating market expansion. Regulatory support and labeling requirements also play a crucial role in promoting transparency and boosting consumer confidence in non-GMO products.

Europe

Europe accounts for approximately 28% of the global market share, driven by stringent regulations on genetically modified organisms and a strong consumer preference for non-GMO food products. The region relies heavily on imports to meet its demand, with countries such as Germany, France, and the Netherlands serving as major import hubs. The primary growth driver in Europe is the regulatory framework that restricts GMO cultivation and promotes non-GMO sourcing, thereby creating a favorable market environment for non-GMO soy products. Additionally, the increasing popularity of organic and sustainable food options, coupled with high consumer purchasing power, supports market growth. The expansion of plant-based diets and the presence of well-developed food processing industries further contribute to the region’s strong demand for non-GMO soy ingredients.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the non-GMO soybean market, with a projected CAGR exceeding 9.5%. Key markets such as China, Japan, and India are driving demand across both food and feed applications. The leading growth driver in this region is the rapid urbanization and rising disposable incomes, which are leading to increased consumption of protein-rich foods, including meat and plant-based alternatives. China’s large livestock industry and growing feed demand, along with Japan and South Korea’s reliance on imports for food processing, significantly contribute to regional growth. Additionally, the increasing awareness of health and nutrition is boosting demand for soy-based food products, particularly in urban areas. Government initiatives to enhance food security and promote sustainable agriculture further support market expansion in the region.

Latin America

Latin America plays a pivotal role in the global non-GMO soybean market, particularly as a major supplier. The region contributes approximately 18% of global supply, with Brazil emerging as a key exporter of non-GMO soybeans. Favorable climatic conditions, abundant arable land, and cost-effective production practices provide a competitive advantage to producers in this region. The primary growth driver is the increasing global demand for non-GMO soy exports, particularly from Europe and Asia, where domestic production is insufficient to meet consumption needs. Investments in agricultural technology and infrastructure are further enhancing productivity and export capabilities, positioning Latin America as a critical player in the global supply chain.

Middle East & Africa

The Middle East and Africa region is experiencing steady growth in the non-GMO soybean market, driven by rising population, urbanization, and increasing demand for protein-rich food products. The region relies heavily on imports to meet its consumption needs, particularly for animal feed and food processing applications. The leading growth driver is the expansion of the livestock sector, supported by government initiatives aimed at improving food security and reducing dependence on imports. Additionally, changing dietary patterns and increasing awareness of health and nutrition are contributing to higher demand for soy-based products. As infrastructure and supply chains continue to develop, the region is expected to present significant growth opportunities for non-GMO soybean suppliers.

Key Players in the Non-GMO Soybean Market

- Archer Daniels Midland Company

- Cargill Incorporated

- Bunge Limited

- Louis Dreyfus Company

- Wilmar International

- CHS Inc.

- Amaggi Group

- Scoular Company

- Clarkson Grain Company

- Grain Millers Inc.

- Identity Preserved International

- Sunrise Foods International

- Perdue Agribusiness

- Fuji Oil Holdings

- Non-GMO Project Verified Suppliers Network