Non-Alcoholic Sparkling Wine Market Size

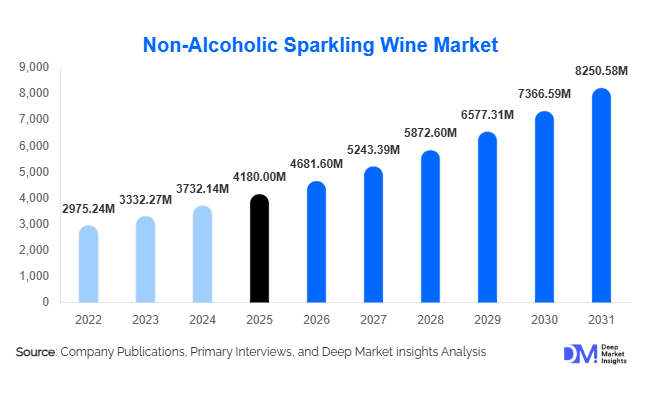

According to Deep Market Insights, the global non-alcoholic sparkling wine market size was valued at USD 4,180 million in 2025 and is projected to grow from USD 4,681.60 million in 2026 to reach USD 8,250.58 million by 2031, expanding at a CAGR of 12.0% during the forecast period (2026–2031). Market expansion is primarily driven by shifting consumer preferences toward low- and zero-alcohol beverages, increasing health consciousness, and the rapid premiumization of alcohol alternatives across developed and emerging economies. The category has transitioned from niche dietary substitutes into mainstream celebratory beverages, supported by improved taste profiles, advanced dealcoholization technologies, and strong retail visibility.

Key Market Insights

- Health-conscious consumption trends are accelerating demand for alcohol-free celebratory beverages globally.

- Premiumization and flavor innovation are reshaping consumer perception, positioning non-alcoholic sparkling wine as a lifestyle product rather than a substitute.

- Europe dominates production and consumption, supported by strong wine heritage and innovation in dealcoholization technologies.

- Asia-Pacific is the fastest-growing region, driven by rising urban middle-class populations and cultural acceptance of alcohol-free alternatives.

- E-commerce and modern retail channels are expanding accessibility and enabling global brand penetration.

- Technological advancements in vacuum distillation and reverse osmosis are significantly improving product quality.

What are the latest trends in the non-alcoholic sparkling wine market?

Premiumization and Craft Positioning

Non-alcoholic sparkling wine is increasingly positioned as a premium beverage category rather than a functional substitute for alcoholic wine. Producers are investing heavily in high-quality grape sourcing, terroir-based branding, and sophisticated packaging formats resembling luxury champagne offerings. Consumers now expect authentic wine-like complexity, refined carbonation, and elegant presentation. Premium labels are introducing vintage-inspired variants, organic certifications, and limited-edition releases, which are improving margins and attracting affluent consumers seeking healthier indulgence options. Restaurants and luxury hospitality venues are also expanding alcohol-free pairing menus, further legitimizing the category.

Technology-Enhanced Dealcoholization Processes

Technological innovation remains a defining trend. Advanced methods such as spinning cone column technology and reverse osmosis allow alcohol removal while preserving aroma compounds and mouthfeel. This has significantly reduced the quality gap between alcoholic and non-alcoholic sparkling wines. Producers are increasingly using AI-driven fermentation monitoring and flavor stabilization techniques to ensure consistency across batches. Improved shelf stability and carbonation retention are enabling global exports, allowing brands to scale internationally while maintaining product integrity.

What are the key drivers in the non-alcoholic sparkling wine market?

Growing Health and Wellness Movement

Consumers worldwide are reducing alcohol consumption due to wellness priorities, fitness culture, and preventive healthcare awareness. Younger demographics, particularly millennials and Gen Z, are embracing “sober-curious” lifestyles, driving sustained demand growth. Non-alcoholic sparkling wine allows participation in social rituals without alcohol intake, making it highly attractive across professional and social settings.

Expansion of Retail and Hospitality Acceptance

Supermarkets, premium restaurants, airlines, and hotels are expanding alcohol-free beverage portfolios. Dedicated zero-alcohol shelves and curated beverage menus have improved product visibility and trial rates. Hospitality operators increasingly view alcohol-free sparkling wine as a high-margin addition catering to inclusive consumer preferences.

Regulatory and Cultural Support

Stricter drunk-driving regulations, workplace alcohol policies, and growing acceptance of alcohol-free lifestyles across regions are encouraging adoption. Government health campaigns promoting reduced alcohol consumption indirectly support category growth, especially in Europe and Asia-Pacific.

What are the restraints for the global market?

Higher Production Costs

Dealcoholization technologies require specialized equipment and energy-intensive processes, increasing manufacturing costs compared to traditional soft beverages. These costs translate into premium retail pricing, limiting penetration among price-sensitive consumers.

Consumer Perception Challenges

Despite improvements, some consumers still associate alcohol-free wines with inferior taste quality. Overcoming legacy perceptions requires continued investment in branding, sampling campaigns, and product education.

What are the key opportunities in the non-alcoholic sparkling wine industry?

Emerging Market Expansion

Rapid urbanization and growing disposable incomes in Asia-Pacific and Middle Eastern countries present major opportunities. Cultural environments with limited alcohol consumption norms are particularly favorable for alcohol-free alternatives. Companies entering early can establish strong brand loyalty and distribution networks.

Functional and Low-Calorie Innovation

Integration of functional ingredients such as botanicals, antioxidants, and adaptogens represents a significant innovation opportunity. Consumers increasingly seek beverages offering wellness benefits alongside indulgence. Low-sugar and clean-label formulations are gaining strong traction among health-focused consumers.

On-Premise and Celebration Occasions

Weddings, corporate events, and luxury hospitality venues are expanding alcohol-free beverage offerings to accommodate diverse consumer preferences. Dedicated alcohol-free beverage menus create new premium consumption occasions, expanding volume demand beyond retail purchases.

Product Type Insights

Alcohol-removed sparkling wine dominates the global non-alcoholic sparkling wine market, accounting for approximately 46% of total market share in 2025. The strong leadership of this segment is primarily driven by consumer preference for authentic wine experiences that closely replicate traditional sparkling wine in aroma, mouthfeel, and complexity while eliminating alcohol content. Advanced dealcoholization technologies, including vacuum distillation and reverse osmosis, have significantly improved product quality, enabling manufacturers to retain varietal characteristics and premium positioning. As health-conscious consumers increasingly moderate alcohol intake without compromising social experiences, alcohol-removed variants have become the preferred substitute during celebrations, corporate gatherings, and lifestyle occasions.Sparkling grape juice alternatives continue to maintain steady demand among entry-level consumers and family-oriented occasions, particularly in emerging markets where affordability and accessibility remain key purchasing factors. These products attract younger consumers and households seeking inclusive beverages suitable for all age groups. Meanwhile, botanical-infused sparkling variants are rapidly gaining traction within premium and experimental beverage categories, reflecting broader consumer interest in functional ingredients, natural flavor infusions, and craft-style innovation. The expansion of organic and vegan-certified sparkling wines further reflects sustainability-driven purchasing behavior, as environmentally conscious consumers increasingly prioritize ethical sourcing, clean-label formulations, and reduced environmental impact across beverage choices. Collectively, innovation in flavor complexity, premium positioning, and wellness alignment continues to strengthen product diversification across the market.

Flavor Insights

White non-alcoholic sparkling wine leads the global market with nearly 52% market share in 2025, supported primarily by its versatile taste profile, refreshing acidity, and compatibility with a wide variety of cuisines. The leading driver for this segment is its strong alignment with everyday consumption occasions, ranging from casual dining to formal celebrations, allowing consumers to integrate alcohol-free options seamlessly into existing food and beverage habits. Additionally, lighter flavor characteristics appeal to both traditional wine consumers transitioning toward moderation and new consumers entering the category through wellness-oriented lifestyles.Rosé variants represent the fastest-growing flavor segment, benefiting from strong lifestyle branding, visual appeal, and social media influence that resonates particularly with millennial and Gen Z consumers. The category’s association with modern social culture, premium aesthetics, and experiential consumption has accelerated adoption across urban markets and hospitality venues. Red sparkling variants remain comparatively niche but are positioned within premium segments, attracting consumers seeking deeper flavor complexity and pairing opportunities with richer cuisines. As producers continue refining tannin balance and texture in alcohol-free red formats, gradual expansion of this segment is expected within mature wine markets.

Distribution Channel Insights

Off-trade retail channels dominate the global market, accounting for approximately 63% of total sales, primarily driven by supermarkets and hypermarkets that provide extensive product visibility, competitive pricing, and consumer convenience. The leading driver of this segment is the normalization of alcohol-free beverages within mainstream retail environments, where dedicated non-alcoholic beverage sections encourage impulse purchases and trial adoption. Large-format retail chains also facilitate brand discovery through promotional campaigns, seasonal displays, and bundled offerings during festive periods.Online retail represents the fastest-growing distribution channel, supported by expanding direct-to-consumer models, subscription beverage services, and digital-first brand strategies. E-commerce platforms enable niche and premium brands to reach geographically dispersed consumers while offering personalized recommendations and educational content that supports category awareness. Specialty beverage stores continue to influence premium purchasing decisions by providing curated selections, expert guidance, and experiential retail environments that reinforce product authenticity and quality perception.

Packaging Insights

Glass bottles account for approximately 71% of global market share, maintaining dominance due to their strong association with premium positioning, traditional wine aesthetics, and celebratory consumption occasions. The leading driver behind glass packaging adoption is consumer perception of authenticity and quality, particularly during social gatherings, weddings, and formal events where presentation plays a significant role in purchasing decisions. Glass also preserves carbonation and flavor stability, reinforcing its suitability for premium non-alcoholic sparkling wines.However, canned sparkling wines are expanding rapidly as convenience-driven consumption patterns reshape beverage packaging preferences. Lightweight portability, single-serve formats, and sustainability advantages such as recyclability and reduced transportation emissions are accelerating adoption among younger consumers and outdoor lifestyle segments. Ready-to-drink occasions, including travel, festivals, and casual social gatherings, continue to support innovation in alternative packaging formats, contributing to broader category accessibility.

End-Use Analysis

Household consumption represents the largest end-use segment, driven primarily by increasing integration of alcohol-free beverages into daily lifestyles and social rituals. The leading driver for this segment is the global shift toward mindful drinking, where consumers seek healthier alternatives for routine relaxation, family celebrations, and weekday socialization without alcohol-related effects. Rising awareness of wellness, productivity, and balanced living continues to encourage repeat household purchases.The hospitality and foodservice sectors are emerging as the fastest-growing end-use segments, supported by restaurants, hotels, and premium dining establishments expanding inclusive beverage menus to cater to diverse consumer preferences. Alcohol-free pairings are increasingly incorporated into tasting menus and fine-dining experiences, enhancing category legitimacy within culinary culture. Airline catering and corporate events are also contributing incremental demand as organizations adopt inclusive beverage offerings for professional and multicultural audiences. Export-driven demand is rising significantly, with European producers expanding distribution into Asia-Pacific and North America, supported by growing global tourism and hospitality industries projected to expand at over 8% annually, directly reinforcing adoption across commercial venues.

| By Product Type | By Flavor Profile | By Distribution Channel | By Packaging Type |

|---|---|---|---|

|

|

|

|

Regional Insights

Europe

Europe leads the global non-alcoholic sparkling wine market with approximately 38% share in 2025, supported by its deeply established wine heritage and advanced production infrastructure. Germany serves as a major innovation hub due to technological leadership in dealcoholization processes, enabling high-quality alcohol-free wine production at scale. France and Spain leverage strong premium branding and appellation-driven expertise to position alcohol-free sparkling wines within luxury and gastronomy segments, while the United Kingdom demonstrates strong retail penetration and consumer acceptance of sober-curious lifestyles.Regional growth is primarily driven by rising health awareness, regulatory encouragement of responsible drinking, and increasing consumer participation in moderation movements such as “Dry January” and wellness-focused social trends. Mature distribution networks, strong export capabilities, and continuous product innovation further sustain Europe’s leadership position, while sustainability initiatives across vineyards and packaging enhance long-term consumer trust.

North America

North America accounts for nearly 27% of global market share, led by the United States and Canada. Market expansion is strongly supported by the rapid rise of sober-curious consumer behavior, particularly among younger professionals seeking premium social experiences without alcohol consumption. Retailers across the region are dedicating larger shelf space to alcohol-free beverages, accelerating visibility and consumer trial.Regional growth drivers include expanding wellness culture, increasing demand for functional and low-calorie beverages, and strong adoption within hospitality and restaurant chains introducing alcohol-free menus. Innovation-led startups and celebrity-backed beverage brands are also contributing to category awareness through digital marketing and experiential campaigns. Additionally, the growth of e-commerce beverage platforms and subscription-based purchasing models continues to strengthen accessibility and repeat consumption patterns.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, projected to expand at over 14% CAGR, driven by rapid urbanization, rising disposable incomes, and evolving social consumption patterns. China, Japan, Australia, and India are key contributors, with metropolitan consumers increasingly embracing premium non-alcoholic beverages during corporate gatherings and social celebrations.Regional growth is fueled by cultural acceptance of alcohol-free alternatives, growing health awareness among younger populations, and expanding modern retail infrastructure. The influence of Western dining culture and international tourism has accelerated exposure to alcohol-free sparkling wine formats, while local distributors increasingly introduce imported premium brands. Additionally, stricter drink-driving regulations and workplace wellness initiatives across several countries support long-term category adoption.

Middle East & Africa

The Middle East & Africa region demonstrates strong growth potential, particularly within markets where cultural and religious factors limit alcohol consumption. Countries such as the UAE and Saudi Arabia are emerging as premium consumption hubs, supported by rapid expansion of luxury hospitality, fine dining establishments, and international tourism projects.Regional growth drivers include increasing demand for sophisticated alcohol-free alternatives that align with social norms while maintaining premium experiences. High-end hotels and event venues are actively incorporating non-alcoholic sparkling wines into beverage offerings to serve global visitors. In Africa, South Africa contributes through export-oriented production capabilities and growing domestic interest in wellness beverages, supported by improving retail infrastructure and rising middle-class consumption.

Latin America

Latin America is witnessing gradual but steady adoption, particularly in Brazil, Mexico, and Chile, where wellness awareness and premium lifestyle trends are influencing beverage choices. Expanding modern retail formats and the growing presence of imported premium brands are introducing consumers to alcohol-free sparkling wine categories.Regional growth is driven by increasing urbanization, evolving dining culture, and rising demand for celebratory beverages suitable for diverse social settings. Hospitality sector development and tourism recovery are further supporting category penetration, while younger consumers demonstrate openness toward innovative and healthier beverage alternatives, positioning the region for sustained long-term growth.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Non-Alcoholic Sparkling Wine Market

- Carl Jung GmbH

- Torres Natureo (Miguel Torres S.A.)

- Eisberg (Schloss Wachenheim AG)

- Freixenet S.A.

- Oddbird International

- Thomson & Scott

- Leitz GmbH

- Kolonne Null

- Sutter Home Winery

- Giesen Group

- Pierre Chavin

- McGuigan Wines

- Codorníu Group

- Be Free Wine

- Ariel Vineyards