New Tea Market Size

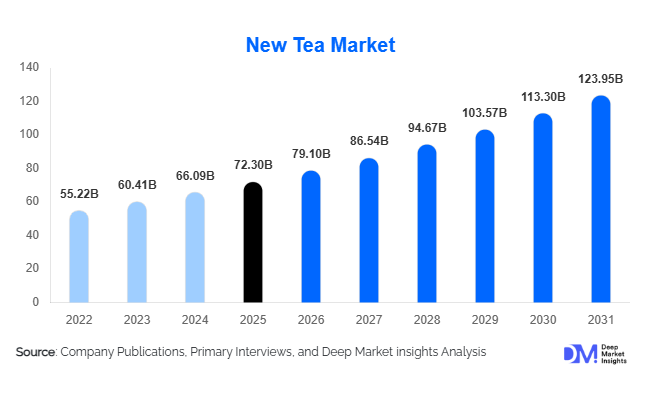

According to Deep Market Insights, the global new tea market size was valued at USD 72.3 billion in 2025 and is projected to grow from USD 79.10 billion in 2026 to reach USD 123.95 billion by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The new tea market growth is primarily driven by rising consumer preference for healthier beverage alternatives, increasing demand for premium and functional tea products, and rapid expansion of specialty tea cafés and ready-to-drink (RTD) tea beverages globally.

Key Market Insights

- Functional and wellness-oriented tea beverages are transforming the global tea industry, with growing demand for immunity, detox, relaxation, and energy-support tea formulations.

- Premiumization is accelerating across developed and emerging markets, driven by consumer interest in artisanal, organic, and single-origin tea products.

- Asia-Pacific dominates the global market, supported by strong tea consumption culture in China, India, Japan, and Southeast Asia.

- North America is among the fastest-growing regions, driven by demand for low-sugar, plant-based, and clean-label beverages.

- Bubble tea and specialty tea café culture are expanding rapidly, particularly among millennials and Gen Z consumers worldwide.

- Digital retail channels and direct-to-consumer tea brands are reshaping distribution, enabling global access to niche and premium tea offerings.

What are the latest trends in the new tea market?

Functional and Wellness Tea Innovations

The new tea industry is increasingly evolving toward wellness-focused beverage innovation. Consumers are actively seeking tea products that offer functional health benefits such as immunity enhancement, stress reduction, digestive wellness, and energy support. Manufacturers are introducing formulations infused with adaptogens, probiotics, collagen, vitamins, botanicals, and herbal extracts to target health-conscious consumers. Detox teas, sleep-support infusions, and metabolism-boosting blends are becoming mainstream product categories across North America, Europe, and Asia-Pacific. The trend is particularly strong among urban millennials and younger consumers who view beverages as part of preventive healthcare and daily wellness routines. Premium wellness teas also command higher profit margins, encouraging brands to accelerate product diversification and R&D investments.

Growth of Premium Tea Cafés and Bubble Tea Chains

The rapid expansion of specialty tea cafés and bubble tea chains is significantly reshaping global tea consumption patterns. Inspired by Asian tea culture, premium tea retail formats are witnessing strong expansion across the United States, Europe, the Middle East, and Southeast Asia. Consumers increasingly prefer customizable beverages with unique flavors, alternative milk options, fruit infusions, and visually appealing presentations promoted through social media platforms. Tea chains are also integrating digital ordering systems, loyalty applications, and AI-powered personalization to improve customer engagement. Premium café experiences are positioning tea as a lifestyle beverage rather than a traditional commodity product, driving substantial market value growth globally.

What are the key drivers in the new tea market?

Rising Demand for Healthy Beverage Alternatives

Growing health awareness and concerns regarding excessive sugar consumption are encouraging consumers to replace carbonated soft drinks with tea-based beverages. Green tea, herbal infusions, and unsweetened RTD tea products are increasingly perceived as healthier alternatives due to their antioxidant properties, lower calorie content, and functional health benefits. Consumers are prioritizing natural, plant-based beverages that support wellness and lifestyle management. This trend is particularly visible in developed markets where obesity, diabetes, and cardiovascular health concerns are accelerating demand for clean-label beverages.

Expansion of Premium and Specialty Tea Consumption

Premiumization has emerged as one of the strongest growth drivers within the global tea industry. Consumers are increasingly willing to pay premium prices for organic tea, artisanal blends, luxury loose-leaf tea, and single-origin products that offer superior quality and authenticity. High-income urban consumers are driving demand for specialty tea experiences that combine taste, sustainability, and premium packaging. Luxury tea gifting and experiential tea consumption are also becoming more prominent in Asia-Pacific and North America, encouraging manufacturers to introduce differentiated premium offerings.

What are the restraints for the global market?

Volatility in Raw Material Prices and Climate Dependency

The new tea market remains highly dependent on agricultural production conditions. Tea cultivation is vulnerable to fluctuations in rainfall patterns, rising temperatures, droughts, pest infestations, and changing climatic conditions. Major tea-producing countries such as China, India, Kenya, and Sri Lanka frequently experience supply disruptions that can significantly impact tea pricing and raw material availability. Rising labor and transportation costs are also contributing to production cost volatility, creating pressure on manufacturer profit margins.

Stringent Regulatory and Certification Requirements

The increasing focus on organic certification, pesticide residue regulations, sustainability compliance, and labeling transparency is creating operational challenges for manufacturers. Functional tea beverages often require extensive validation regarding ingredient safety and health claims, especially across international markets with differing regulatory frameworks. Compliance costs related to sustainable sourcing certifications, biodegradable packaging, and export regulations may create barriers for smaller and emerging tea brands attempting global expansion.

What are the key opportunities in the new tea industry?

Expansion of Functional RTD Tea Beverages

The ready-to-drink tea category represents one of the largest opportunities within the global new tea market. Consumers increasingly prefer convenient, portable, and health-focused beverages suitable for busy lifestyles. Functional RTD teas infused with vitamins, probiotics, herbal extracts, and low-sugar formulations are gaining strong traction across retail and convenience channels. Beverage manufacturers are heavily investing in innovative packaging technologies, cold-brew tea formulations, and sparkling tea products to attract younger demographics. As consumers continue shifting away from traditional carbonated beverages, RTD tea demand is expected to accelerate substantially over the next decade.

Digital Retail and Direct-to-Consumer Growth

E-commerce and direct-to-consumer business models are creating significant growth opportunities for tea brands globally. Online channels allow manufacturers to market niche products such as organic blends, artisanal teas, and wellness-focused formulations directly to high-value consumers without heavy reliance on traditional retail infrastructure. Subscription-based tea services, influencer-driven marketing, AI-powered personalization, and social commerce are improving customer engagement and repeat purchases. Emerging markets with rapidly expanding internet penetration and digital payment adoption are expected to further strengthen online tea sales growth globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72.30 Billion |

| Market Size in 2026 | USD 79.10 Billion |

| Market Size in 2031 | USD 123.95 Billion |

| CAGR | 9.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global new tea market is experiencing substantial diversification across product categories as consumers increasingly seek beverages that combine wellness benefits, premium experiences, and functional nutrition. Green tea continues to dominate the overall market landscape, accounting for nearly 28% of global market share in 2025. The segment’s leadership position is primarily supported by strong consumer awareness regarding antioxidant content, metabolism enhancement, cardiovascular wellness, and weight management benefits. The widespread popularity of catechin-rich beverages, particularly in Asia-Pacific and North America, continues to strengthen global demand for green tea products across both retail and foodservice channels. Manufacturers are also introducing innovative green tea blends infused with botanicals, fruits, collagen, probiotics, and adaptogens to attract younger health-conscious consumers seeking multifunctional beverages.Premium and specialty tea categories, including organic teas, artisanal blends, single-origin teas, handcrafted loose-leaf teas, and ethically sourced products, are gaining considerable traction among affluent urban consumers. Consumers increasingly value authenticity, traceability, sustainable farming practices, and premium packaging experiences, particularly within developed markets. Luxury tea brands are emphasizing storytelling, regional sourcing, rare tea varieties, and artisanal craftsmanship to differentiate themselves in highly competitive premium beverage markets.Ready-to-drink tea beverages are also rapidly expanding within convenience retail, e-commerce, vending, and foodservice channels. Busy urban lifestyles and increasing demand for healthier grab-and-go beverage alternatives continue to drive strong growth in RTD tea consumption globally. Manufacturers are increasingly launching low-calorie, low-sugar, sparkling, probiotic-infused, and functional RTD tea beverages targeted toward younger consumers seeking convenience without compromising wellness preferences.

Form Insights

Based on form, tea bags continue to dominate the global new tea market with approximately 34% market share in 2025 owing to their affordability, convenience, ease of preparation, and extensive availability across supermarkets, convenience stores, and online retail platforms. The dominance of tea bags is strongly supported by rising household consumption and workplace beverage usage where convenience remains a major purchasing factor. Consumers prefer tea bags for their consistency in flavor, quick brewing process, portability, and accessibility across multiple price ranges. Manufacturers are also increasingly introducing biodegradable and plastic-free tea bags in response to rising environmental concerns and sustainable packaging regulations.Instant tea powders and tea concentrates are gaining increasing popularity within foodservice operations, beverage manufacturing, and institutional applications due to their scalability, convenience, and extended shelf life. These formats are particularly important in the production of ready-to-drink beverages, bubble tea preparations, functional wellness drinks, and flavored iced tea products. The rapid growth of café chains and quick-service beverage outlets is supporting increasing industrial demand for concentrated tea ingredients.Tea pods and capsules are emerging as niche premium categories driven by growing adoption of single-serve beverage systems in developed economies. Consumers seeking convenience, portion control, and premium beverage experiences are increasingly adopting tea capsules compatible with modern brewing machines. Technological innovation within smart kitchen appliances and home beverage systems is expected to create additional opportunities for pod-based tea consumption over the forecast period.

Distribution Channel Insights

Supermarkets and hypermarkets continue to account for the largest distribution share globally due to extensive retail penetration, strong product visibility, wide brand availability, and consumer accessibility. Large-format retail stores enable consumers to compare product variants, pricing, flavors, and packaging formats conveniently under a single shopping environment. Promotional campaigns, in-store sampling activities, and bundled offers further strengthen tea sales through organized retail channels. Emerging economies are also witnessing significant expansion of modern retail infrastructure, which continues to improve consumer access to branded tea products.Specialty tea stores continue to attract premium consumers seeking curated tea experiences, artisanal blends, rare tea varieties, and expert product guidance. These stores often emphasize experiential retail concepts through tea tasting sessions, wellness workshops, and educational product demonstrations that enhance customer engagement and brand loyalty. Specialty retail channels play an important role in supporting premiumization trends across the global tea industry.Foodservice distribution is expanding rapidly with the global growth of bubble tea chains, premium cafés, tea lounges, restaurants, and hospitality operators integrating specialty tea beverages into their menus. Tea-based mocktails, wellness beverages, matcha lattes, flavored iced teas, and fusion tea drinks are becoming increasingly popular across urban foodservice environments. Hospitality establishments are also incorporating premium tea experiences into luxury hotel dining and wellness tourism offerings to enhance consumer experiences.Digital commerce platforms are increasingly enabling smaller and independent tea brands to expand internationally without requiring substantial investments in physical retail infrastructure. Social commerce, influencer collaborations, subscription-based tea clubs, and targeted digital advertising campaigns are significantly reshaping global tea distribution dynamics.

End-Use Insights

Household consumption remains the largest end-use segment within the global new tea market, contributing nearly 46% of total demand in 2025. The segment’s dominance is primarily driven by rising at-home beverage consumption trends, increasing health awareness, and growing consumer preference for natural and functional beverages. Tea remains deeply integrated into daily consumption routines across multiple cultures and regions, supporting stable long-term household demand. The expansion of remote work culture and wellness-oriented lifestyles has further encouraged consumers to increase tea consumption at home as part of relaxation and self-care routines.Foodservice applications represent the fastest-growing end-use segment due to the rapid expansion of tea cafés, bubble tea outlets, specialty beverage chains, and experiential café concepts across urban markets. Younger consumers increasingly view tea beverages as social lifestyle products rather than merely traditional beverages. Innovative tea-based beverages incorporating fruits, dairy alternatives, tapioca pearls, collagen, and functional ingredients are driving substantial menu innovation within foodservice establishments.The hospitality and travel industries are increasingly incorporating luxury tea experiences into hotel dining programs, wellness retreats, cruise services, and airline beverage menus. Premium tea pairings, afternoon tea experiences, and wellness-oriented beverage offerings are helping hospitality operators enhance customer experiences while supporting premium positioning strategies.Beverage manufacturers are also expanding the use of tea extracts and concentrates within nutraceutical beverages, fortified drinks, sports beverages, functional energy drinks, and beauty-focused wellness products. The growing convergence between functional nutrition and beverage innovation continues to create new industrial applications for tea ingredients globally.

Price Range Insights

Mid-range tea products account for the largest volume share within the global new tea market due to their broad affordability, mass-market accessibility, and extensive retail availability across both developed and developing economies. Consumers within this segment prioritize value, quality consistency, and product familiarity, making mid-priced tea products highly attractive for daily consumption. Large multinational tea brands continue to dominate this category through aggressive retail expansion, product diversification, and promotional pricing strategies.Premium and super-premium tea categories are witnessing substantially faster growth rates, particularly in urban centers where consumers increasingly prioritize quality, sustainability, artisanal sourcing, and elevated beverage experiences. Rising disposable incomes, evolving lifestyle preferences, and growing consumer willingness to pay for authenticity are significantly contributing to premium segment expansion globally. Luxury loose-leaf teas, handcrafted artisanal blends, imported wellness teas, ceremonial matcha products, and organic single-origin varieties are commanding premium pricing due to strong brand positioning and superior ingredient quality.Economy tea products continue to maintain strong demand across price-sensitive markets in Asia, Africa, and Latin America where tea remains an essential daily beverage consumed in high volumes. Affordable pricing, local production capabilities, and widespread distribution networks continue to support stable demand for economy tea products. Manufacturers operating within this segment are focusing on cost optimization, efficient supply chains, and large-scale production to remain competitive while maintaining affordability for mass-market consumers.

Explore more data points, trends and opportunities Download Free Sample Report

New Tea Market Segmentations

By Product Type

- Green Tea

- Black Tea

- Oolong Tea

- White Tea

- Herbal & Botanical Tea

- Functional & Wellness Tea

- Fruit Infusion Tea

- Ready-to-Drink (RTD) Tea

- Specialty & Premium Tea

By Form

- Loose Leaf Tea

- Tea Bags

- Instant Tea Powder

- Tea Pods & Capsules

- Liquid Tea Concentrates

By Nature

- Conventional

- Organic

- Sustainable/Fair-Trade Certified

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Tea Stores

- Online Retail/E-Commerce

- Foodservice Distribution

- Direct-to-Consumer (DTC)

- Health & Wellness Stores

By End Use

- Household Consumption

- Foodservice

- Corporate & Institutional

- Wellness & Healthcare

- Hospitality & Travel

- Beverage Manufacturing

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global new tea market with approximately 47% market share in 2025 and is expected to maintain its leadership position throughout the forecast period. The region’s dominance is strongly supported by deep-rooted tea consumption traditions, large population base, expanding middle-class demographics, and strong regional production capabilities. China remains the world’s largest producer and consumer of tea due to centuries-old tea culture, increasing domestic premiumization trends, and strong export capabilities. Rising demand for premium green tea, oolong tea, organic tea, and functional wellness beverages continues to strengthen the Chinese market.Southeast Asian countries including Thailand, Indonesia, Vietnam, Malaysia, and the Philippines are witnessing robust growth in bubble tea, flavored tea beverages, and café culture expansion. Rising disposable incomes, westernized consumption patterns, digital food delivery platforms, and increasing youth population are major drivers accelerating regional demand. Additionally, the rapid growth of e-commerce platforms and social media-driven beverage trends is enabling tea brands to expand rapidly across urban markets in Asia-Pacific.

North America

North America accounts for nearly 19% of the global new tea market and remains one of the fastest-growing regional markets worldwide. The United States continues to drive regional growth through increasing consumer demand for low-sugar, clean-label, organic, and functional tea beverages. Rising health concerns regarding obesity, diabetes, and excessive sugar consumption are encouraging consumers to replace carbonated soft drinks with healthier tea alternatives. Functional wellness beverages targeting immunity support, detoxification, stress reduction, digestive wellness, and hydration are gaining strong traction across the region.Canada is also witnessing increasing demand for sustainable, ethically sourced, and environmentally responsible tea products driven by rising wellness awareness and sustainability-conscious consumer behavior. The expansion of specialty tea boutiques, wellness cafés, and premium foodservice establishments is further supporting regional premiumization trends. Additionally, strong digital commerce penetration and subscription-based tea services are accelerating consumer access to premium international tea brands throughout North America.

Europe

Europe holds approximately 21% market share globally, led by the United Kingdom, Germany, France, and Italy. The region continues to represent a mature yet steadily evolving tea market characterized by high consumer awareness regarding sustainability, product quality, and wellness-oriented beverage consumption. The United Kingdom remains one of the world’s largest tea-consuming nations where tea consumption is deeply integrated into daily cultural traditions. Premium black tea blends, herbal teas, and functional wellness beverages continue to experience strong demand across British households and foodservice channels.European consumers strongly prioritize clean-label ingredients, recyclable packaging, ethical sourcing, and sustainability certifications when purchasing tea products. Stringent environmental regulations and growing climate awareness are encouraging manufacturers to adopt eco-friendly packaging materials and transparent sourcing practices. Functional wellness teas, immunity-supporting beverages, and organic specialty blends are gaining considerable popularity among younger consumers seeking healthier and environmentally responsible consumption patterns.

Latin America

Latin America is emerging as an important developing growth region within the global new tea market driven by rising urbanization, improving disposable incomes, and increasing consumer awareness regarding wellness beverages. Countries including Brazil, Mexico, Argentina, and Chile are witnessing growing demand for herbal teas, detox beverages, imported specialty teas, and premium RTD tea products. Consumers are increasingly incorporating tea into healthier lifestyle routines as awareness regarding functional nutrition and preventive healthcare expands across the region.Growing tourism industries and expanding foodservice sectors in major metropolitan areas are supporting the popularity of premium tea beverages, iced tea products, and specialty café concepts. Additionally, increasing investments in retail modernization and cross-border e-commerce are expected to further strengthen long-term regional market growth.

Middle East & Africa

The Middle East & Africa region is witnessing steadily growing demand within the global new tea market supported by strong tea consumption traditions, rising premium café culture, tourism expansion, and increasing disposable incomes. Tea remains an important cultural beverage across countries including Turkey, Saudi Arabia, UAE, Morocco, Egypt, and South Africa where social tea consumption continues to drive stable household demand.Africa continues to play a vital role within the global tea supply chain, particularly through major tea-producing countries such as Kenya, which remains one of the world’s leading tea exporters. Expanding agricultural investments, export-oriented tea production, and growing international demand for African tea varieties continue to support regional industry development. Improvements in retail infrastructure, digital commerce penetration, and urban consumer spending are expected to further contribute to market expansion across Middle Eastern and African economies over the forecast period.

Key Players in the New Tea Market

- Unilever

- Nestlé

- Tata Consumer Products

- ITO EN

- The Coca-Cola Company

- PepsiCo

- DAVIDsTEA

- Twinings

- Dilmah Ceylon Tea Company

- Bigelow Tea Company

- Celestial Seasonings

- Harney & Sons

- Vahdam India

- Tenfu Group

- Lupicia