Neutral Grain Spirit Market Size

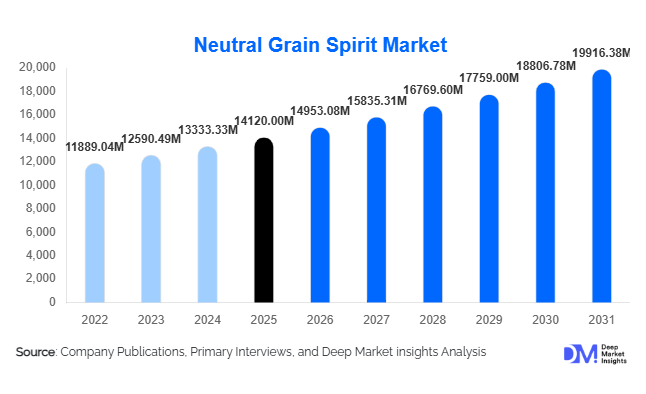

According to Deep Market Insights, the global neutral grain spirit market size was valued at USD 14120 million in 2025 and is projected to grow from USD 14953.08 million in 2026 to reach USD 19916.38 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The neutral grain spirit market growth is primarily driven by rising global spirits consumption, expanding ready-to-drink (RTD) beverage demand, pharmaceutical-grade ethanol requirements, and increasing industrial solvent applications.

Neutral grain spirit (NGS), typically distilled at 95–96% ABV, serves as the backbone of vodka, gin, liqueurs, RTDs, medicinal tinctures, flavor extraction systems, and various industrial applications. Growth across Asia-Pacific and North America, combined with premiumization trends in Europe, is accelerating demand for high-purity ethanol solutions. Increasing investments in grain-based distillation infrastructure and government-supported ethanol programs further support long-term supply stability and export-driven expansion.

Key Market Insights

- Beverage-grade neutral grain spirit accounts for over 60% of global demand, primarily driven by vodka, gin, and flavored alcoholic beverages.

- Asia-Pacific holds the largest production share, supported by strong grain availability and expanding distillery infrastructure in India and China.

- Pharmaceutical-grade ethanol is the fastest-growing segment, expanding due to hygiene awareness and medical formulation demand.

- Direct industrial contracts dominate distribution, representing over half of global transactions.

- Raw material price volatility significantly influences pricing benchmarks and profit margins.

- Top five players control approximately 40% of the global market, indicating moderate consolidation.

What are the latest trends in the neutral grain spirit market?

Premiumization of Spirits and RTD Expansion

The premiumization of vodka and gin is increasing demand for ultra-neutral, high-purity grain spirit with consistent organoleptic properties. RTD beverages, including hard seltzers and flavored vodka mixes, are expanding at faster rates than traditional spirits in North America and Europe. Beverage companies are entering long-term sourcing agreements with ethanol producers to secure quality consistency. Craft distilleries are also contributing to demand for specialty grain-based spirits with traceable raw material origins.

Shift Toward Grain-Based Ethanol Production

Governments in countries such as India and China are encouraging grain-based ethanol production to utilize agricultural surpluses and strengthen domestic value chains. Modern distillation technologies, energy-efficient multi-pressure columns, and improved dehydration units are enhancing yield efficiency and reducing carbon intensity. Sustainability initiatives, including biomass boilers and wastewater recycling systems, are becoming standard investments in new distilleries.

What are the key drivers in the neutral grain spirit market?

Rising Global Alcoholic Beverage Consumption

Global spirits consumption continues to grow steadily, particularly in Asia-Pacific and North America. Vodka alone accounts for nearly 30% of beverage-grade NGS usage. Expansion of flavored spirits and RTDs is accelerating production volumes. Increasing disposable incomes and urbanization in emerging economies are further strengthening long-term demand.

Growing Pharmaceutical and Hygiene Applications

Pharmaceutical manufacturers rely on high-purity ethanol for syrups, tinctures, antiseptics, and sanitizers. The global pharmaceutical industry’s sustained growth above 6% annually is reinforcing ethanol demand. Compliance with pharmacopeial standards such as USP and EP is enabling producers to command premium pricing in this segment.

What are the restraints for the global market?

Feedstock Price Volatility

Corn, wheat, and molasses account for nearly 65–70% of production costs. Climatic disruptions, export restrictions, and commodity speculation create pricing fluctuations, directly affecting producer margins.

Regulatory and Excise Complexity

Alcohol production is heavily regulated with varying excise structures across regions. Licensing, taxation, and cross-border trade restrictions can limit expansion and increase compliance costs for producers.

What are the key opportunities in the neutral grain spirit industry?

Expansion of Pharmaceutical-Grade Capacity

Upgrading facilities to pharmaceutical-grade certification standards presents a high-margin opportunity. Pharmaceutical-grade ethanol commands 15–20% higher margins than beverage-grade spirit and is witnessing strong demand growth across emerging markets.

Export-Oriented Production in Emerging Economies

India, Brazil, and Thailand are emerging as export hubs due to competitive feedstock pricing and supportive ethanol policies. Growing import demand in Africa and the Middle East presents untapped opportunities for large-scale producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14120 Million |

| Market Size in 2026 | USD 14953.08 Million |

| Market Size in 2031 | USD 19916.38 Million |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Raw Material Insights

Wheat-based neutral grain spirit accounts for approximately 34% of the global market share in 2025, making it the leading raw material segment. Its dominance is primarily driven by strong production capacity across Europe, particularly in Poland, Germany, and France, where high-quality wheat supplies and advanced distillation infrastructure support premium spirit manufacturing. Wheat-based NGS is widely preferred in premium vodka and gin production due to its neutral sensory profile, smooth mouthfeel, and consistent purity levels. The leading segment growth is further supported by rising consumer demand for premium and craft alcoholic beverages across developed markets.

Corn-based ethanol holds a substantial share, particularly in North America, where abundant maize production, established ethanol refineries, and integrated grain supply chains ensure cost efficiency and production scalability. The United States benefits from vertically integrated agribusiness operations and federal biofuel incentives, indirectly supporting neutral grain spirit production infrastructure. Sugarcane-based and molasses-based neutral spirits are prominent in Latin America and parts of Asia, leveraging mature sugar industries and feedstock cost advantages. Brazil, India, and Thailand benefit from strong sugarcane availability, enabling competitive pricing and export-oriented production models.

Grade Insights

Beverage-grade neutral grain spirit dominates the global market, accounting for nearly 62% of total market share in 2025. The segment’s leadership is driven by sustained global demand for vodka, gin, flavored spirits, and ready-to-drink (RTD) alcoholic beverages. Expanding urban populations, premiumization trends, and rising disposable incomes across emerging economies continue to fuel beverage-grade consumption. Strict quality standards and purity requirements in alcoholic beverage manufacturing further reinforce the segment’s structural dominance.

Pharmaceutical-grade ethanol represents the fastest-growing grade segment, supported by rising healthcare expenditure, expanding pharmaceutical manufacturing capacity, and increased use of ethanol in antiseptics, syrups, tinctures, and solvent applications. Growth is particularly strong in Asia-Pacific and the Middle East, where governments are investing in domestic pharmaceutical production. Industrial and cosmetic grades collectively account for approximately 20–25% of global demand, supported by usage in personal care formulations, chemical intermediates, and cleaning products.

Application Insights

Alcoholic beverage production remains the dominant application, accounting for nearly 65% of total neutral grain spirit consumption. The leading application growth driver is the continued global expansion of vodka and gin production, alongside rapid growth in flavored spirits and premium craft offerings. The RTD segment is the fastest-growing sub-application within beverages, supported by changing consumer preferences toward convenience, lower alcohol content options, and innovative flavor profiles. Younger demographics and urban consumers are key contributors to this growth trend.

Pharmaceutical applications account for approximately 15% of total demand and are expanding steadily due to increased healthcare awareness, growing generic drug production, and the continued use of ethanol as a solvent and preservative. Food flavor extraction, perfumes, cosmetics, and chemical intermediates collectively contribute the remaining share, benefiting from expanding food processing industries and rising global demand for personal care products.

End-Use Industry Insights

Distilleries and beverage manufacturers represent over 63% of global neutral grain spirit demand, making them the leading end-use segment. Growth in this segment is directly supported by steady expansion of the global spirits industry, which is valued at over USD 520 billion in 2025. Premiumization, export-oriented production, and brand diversification strategies among major distillers continue to strengthen long-term demand visibility for neutral grain spirit suppliers.

Pharmaceutical manufacturers represent the fastest-growing end-use segment, expanding at an estimated CAGR of 7–8%. Increasing investments in domestic drug production across Asia, the Middle East, and Africa are contributing to rising pharmaceutical-grade ethanol consumption. Export-driven demand is also increasing in Africa and the Middle East, where local production capacity remains limited and import reliance supports stable trade flows.

Explore more data points, trends and opportunities Download Free Sample Report

Neutral Grain Spirit Market Segmentations

By Raw Material

- Wheat-Based Neutral Grain Spirit

- Corn (Maize)-Based Neutral Grain Spirit

- Barley-Based Neutral Grain Spirit

- Rye-Based Neutral Grain Spirit

- Sugarcane-Based Neutral Spirit

- Molasses-Based Neutral Spirit

- Multi-Grain Blends

By Grade

- Beverage Grade

- Pharmaceutical Grade

- Industrial Grade

- Cosmetic & Personal Care Grade

- Food Processing Grade

By Application

- Alcoholic Beverage Production (Vodka, Gin, Liqueurs, RTDs)

- Pharmaceutical Formulations

- Food & Flavor Extraction

- Cosmetics & Perfumes

- Chemical Intermediates

- Industrial Solvents

By Distribution Channel

- Direct Industrial Contracts

- Bulk Distributors

- Export/Trading Houses

- Contract Distillation & Private Label

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 32% of the global neutral grain spirit market share in 2025, positioning it as the largest and fastest-growing regional market with an estimated CAGR of around 7%. India and China lead regional consumption and production. India alone represents nearly 12% of global consumption, driven by strong domestic spirits demand, a large population base, and government-backed ethanol blending and industrial policies. Rising disposable income, expanding urbanization, and the rapid growth of organized retail and hospitality sectors are further stimulating demand. In China, increasing premium spirit consumption and growing pharmaceutical manufacturing capacity are key growth drivers. Southeast Asian countries are also witnessing rising investments in distillation infrastructure to support both domestic consumption and export opportunities.

Europe

Europe holds nearly 28% of the global market, supported by well-established distillation industries in Poland, Germany, and France. Eastern Europe remains a key vodka production hub, benefiting from strong cultural consumption patterns and established export networks. Western Europe drives premium gin and craft spirit demand, particularly in the UK, Spain, and France. Regional growth is supported by premiumization trends, strong regulatory quality standards, and advanced agricultural supply chains. Additionally, sustainability initiatives and energy-efficient distillation technologies are enhancing production efficiency and competitiveness.

North America

North America commands approximately 24% market share, with the United States contributing nearly 20% of global consumption. The region benefits from abundant corn production, advanced ethanol refining capacity, and a mature beverage industry. Growth is strongly supported by the rapid expansion of RTDs, flavored spirits, and craft distilleries. Increasing consumer preference for premium and locally produced spirits is reinforcing small- and mid-scale distillery investments. Pharmaceutical and personal care manufacturing expansion further supports steady industrial-grade demand.

Latin America

Latin America is characterized by strong sugarcane-based ethanol infrastructure, with Brazil dominating regional production. The country’s integrated sugar and ethanol industry provides significant feedstock cost advantages and export competitiveness. Growth drivers include expanding domestic spirits consumption, favorable agricultural conditions, and increasing export opportunities to Africa and North America. Mexico and Colombia are also witnessing growth in beverage alcohol production and pharmaceutical manufacturing, supporting regional demand expansion.

Middle East & Africa

The Middle East & Africa region remains largely import-dependent, though demand is steadily rising. South Africa and the UAE serve as major consumption and re-export hubs. Increasing pharmaceutical manufacturing capacity, healthcare investments, and expanding food processing industries are boosting regional demand. In Africa, rising urbanization and growing middle-class populations are gradually increasing alcoholic beverage consumption. Limited domestic distillation capacity in several countries creates sustained import demand, presenting opportunities for global exporters.

Investment & CapEx Trends

Capital expenditure across the neutral grain spirit market is increasingly focused on capacity expansion, efficiency improvements, and sustainability initiatives. Governments in India, Brazil, and China are actively supporting ethanol production under national industrial strategies such as “Make in India” and “Made in China 2025,” encouraging domestic manufacturing and reducing import dependence. Significant investments are being directed toward modern distillation columns, molecular sieve dehydration systems, automated fermentation units, and energy-efficient boilers to enhance yield and reduce operating costs.

Private sector CapEx is concentrated on upgrading facilities to meet pharmaceutical-grade standards, improving carbon footprint performance, and integrating renewable energy sources into production processes. Export-oriented distilleries located near major ports are expanding storage and logistics infrastructure to strengthen global supply chain capabilities. Sustainability-driven investments, including waste heat recovery systems and by-product valorization, are emerging as key competitive differentiators in mature markets.

Key Players in the Neutral Grain Spirit Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Green Plains Inc.

- Wilmar International Ltd.

- Tereos Group

- MGP Ingredients Inc.

- Cristalco SAS

- COFCO Biochemical

- Raízen Energia

- Manildra Group

- Bajaj Hindusthan Sugar Ltd.

- Grain Processing Corporation

- Globus Spirits Ltd.

- Louis Dreyfus Company

- Biosev SA