Natural Vitamins Market Size

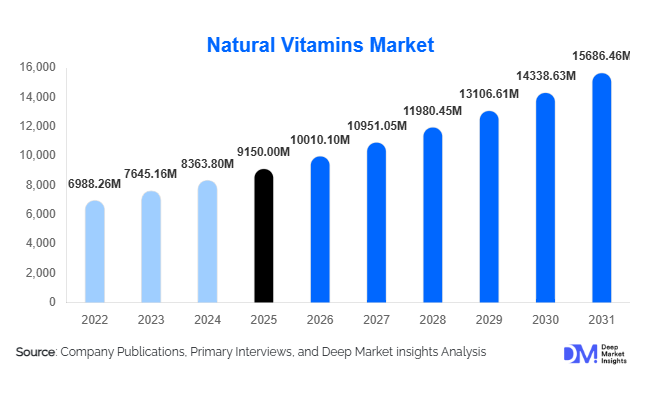

According to Deep Market Insights,the global natural vitamins market size was valued at USD 9,150 million in 2025 and is projected to grow from USD 10,010.10 million in 2026 to reach USD 15,686.46 million by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The natural vitamins market growth is primarily driven by rising consumer preference for plant-based and clean-label nutritional supplements, increasing awareness of preventive healthcare, and expanding demand for bioavailable micronutrients across dietary supplements, functional foods, and pharmaceutical applications. Growing concerns regarding synthetic additives and chemical processing have accelerated the shift toward plant-derived and fermentation-based vitamins, positioning natural variants as premium alternatives in the global nutraceutical industry.

Key Market Insights

- Plant-derived vitamins account for nearly 46% of the 2025 market share, reflecting strong consumer preference for vegan and organic-certified products.

- Natural Vitamin D leads by product type, contributing approximately 18% of total revenue in 2025 due to widespread global deficiency concerns.

- North America dominates the global market with around 34% share in 2025, driven by high supplement penetration and advanced e-commerce infrastructure.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR, supported by rising disposable incomes in China and India.

- Online retail and direct-to-consumer channels represent 28% of total distribution share, highlighting digital transformation in supplement sales.

- The top five companies collectively hold approximately 40% of global market share, indicating moderate competitive concentration.

What are the latest trends in the natural vitamins market?

Shift Toward Fermentation-Based and Sustainable Production

Manufacturers are increasingly investing in precision fermentation technologies to produce vitamins such as B12 and D3 through microbial biosynthesis. This method ensures consistent supply, reduces dependence on seasonal agricultural inputs, and aligns with sustainability goals. Companies are emphasizing carbon-neutral operations, traceability systems, and non-GMO certifications to strengthen brand positioning. Blockchain-enabled ingredient transparency and third-party organic certifications are becoming key differentiators, particularly in North America and Europe.

Personalized Nutrition and Subscription Models

Digital health integration is reshaping purchasing behavior. AI-driven health assessments, microbiome testing, and wearable data tracking are enabling customized vitamin regimens delivered via subscription-based platforms. Consumers are increasingly opting for personalized daily vitamin packs tailored to age, gender, and lifestyle requirements. This shift from mass-market supplementation to precision nutrition is improving customer retention rates and raising average order values across online distribution channels.

What are the key drivers in the natural vitamins market?

Rising Preventive Healthcare Awareness

Escalating healthcare costs and increasing prevalence of chronic diseases such as osteoporosis, cardiovascular disorders, and immunity-related conditions have strengthened demand for daily supplementation. Consumers view natural vitamins as safer and more bioavailable alternatives to synthetic products. The aging global population, particularly in developed economies, further reinforces structural demand for vitamin D, B-complex, and antioxidant formulations.

Clean-Label and Plant-Based Consumer Movement

The global shift toward vegan, vegetarian, and flexitarian lifestyles has significantly boosted demand for plant-derived vitamins. Consumers actively seek products free from artificial preservatives, synthetic fillers, and genetically modified ingredients. Organic certifications and sustainable sourcing practices are influencing purchasing decisions, enabling manufacturers to command premium pricing and maintain higher profit margins ranging between 18% and 25%.

What are the restraints for the global market?

High Production and Raw Material Costs

Natural extraction processes and fermentation-based production involve higher input costs compared to synthetic alternatives. Seasonal variability in plant raw materials and fluctuations in agricultural commodity prices can impact supply stability and pricing strategies. These factors restrict penetration in price-sensitive developing markets.

Regulatory Complexity and Claim Restrictions

Regulatory frameworks governing health claims, labeling standards, and ingredient approvals vary significantly across regions. Stringent compliance requirements in markets such as the United States and the European Union increase operational costs and prolong product launch timelines. Non-compliance risks product recalls and reputational damage, posing a significant barrier for smaller entrants.

What are the key opportunities in the natural vitamins industry?

Expansion in Emerging Markets

Rapid urbanization and rising middle-class income in countries such as China, India, Brazil, and Indonesia present substantial growth potential. Government-led health awareness campaigns and preventive nutrition initiatives are encouraging wider supplement adoption. Local manufacturing partnerships can reduce import dependency and improve margins, especially in Asia-Pacific where domestic production incentives are strengthening under programs such as “Make in India” and biotechnology expansion policies in China.

Integration with Functional Foods and Beauty Nutrition

Natural vitamins are increasingly incorporated into functional beverages, plant-based dairy alternatives, fortified snacks, and beauty-from-within products. The global functional foods industry, valued at over USD 180 billion, is providing cross-sector growth opportunities. Collagen boosters, antioxidant blends, and immunity gummies are expanding application scope beyond traditional capsule formats.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9150 Million |

| Market Size in 2026 | USD 10010.10 Million |

| Market Size in 2031 | USD 15686.46 Million |

| CAGR | 9.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Natural Vitamin D dominates the product segment, accounting for approximately 18% of total market revenue in 2025. Its leadership position is primarily driven by the rising global prevalence of Vitamin D deficiency, increasing diagnostic testing, and strong clinical validation supporting its role in bone mineralization, calcium absorption, immune modulation, and inflammatory response management. Growing consumer awareness campaigns and physician recommendations have significantly strengthened routine Vitamin D supplementation across both developed and emerging economies. Natural Vitamin C and B-Complex formulations follow closely, supported by sustained demand for immune resilience, stress management, and energy metabolism optimization. Multi-vitamin blends continue to maintain robust adoption among adult consumers seeking comprehensive daily nutritional coverage, particularly in preventive healthcare regimes. Fermentation-derived Vitamin B12 is gaining prominence within vegan and plant-based product portfolios, reflecting global dietary transitions, ethical consumption trends, and the need for bioavailable B12 sources in plant-forward diets.

Source Insights

Plant-derived vitamins lead the source segment with nearly 46% revenue share in 2025, primarily driven by the accelerating shift toward clean-label, organic-certified, and vegan-friendly formulations. Consumers increasingly associate plant-based sourcing with sustainability, transparency, and reduced environmental impact, encouraging manufacturers to expand botanical extraction technologies and traceable sourcing practices. Microbial and fermentation-derived sources represent the fastest-growing sub-segment due to superior scalability, consistent purity levels, and cost-efficient large-scale production capabilities. Advances in biotechnology and precision fermentation are further enhancing yield efficiency and stability. Animal-derived sources maintain steady demand, particularly for natural Vitamin A and D extracted from fish liver oils, where established bioavailability and traditional usage continue to support market presence. However, ethical sourcing concerns and sustainability pressures are moderating long-term growth relative to plant-based alternatives.

Form Insights

Capsules and softgels collectively account for approximately 34% of market share in 2025, maintaining their leadership due to dosage precision, enhanced bioavailability, extended shelf stability, and consumer familiarity. Their compatibility with oil-soluble vitamins such as Vitamin D and A further strengthens their dominance. Gummies are experiencing rapid expansion across pediatric and adult segments, supported by improved flavor technologies, sugar-reduction innovations, and growing preference for convenient, palatable delivery formats. Powders and liquid drops continue to serve specialized niches, particularly in sports nutrition, pediatric supplementation, and clinical nutrition settings where flexible dosing and rapid absorption are prioritized. The diversification of delivery formats reflects manufacturers’ efforts to enhance compliance, personalization, and targeted nutrient delivery.

Distribution Channel Insights

Online retail and direct-to-consumer platforms contribute approximately 28% of total market revenue in 2025, making digital commerce one of the primary growth engines for the industry. The leading driver behind this channel’s expansion is the increasing consumer preference for subscription-based models, personalized supplement regimens, product comparison convenience, and access to extensive brand portfolios. Pharmacies and drug stores remain a significant distribution channel, particularly for clinically recommended formulations and prescription-adjacent supplementation, benefiting from consumer trust and professional guidance. Specialty health stores retain premium positioning for organic-certified, sustainably sourced, and high-potency formulations, appealing to informed consumers seeking differentiated and niche products.

End-Use Insights

Adults aged 18–60 years represent nearly 41% of total consumption in 2025, making this the leading end-use segment. The primary driver for this dominance is the growing emphasis on preventive healthcare, immunity enhancement, stress management, and productivity optimization among working populations. Increasing urbanization and sedentary lifestyles further reinforce routine supplementation habits. The geriatric population segment is expanding rapidly due to rising life expectancy, increased incidence of osteoporosis and chronic deficiencies, and physician-driven supplementation for bone, cardiovascular, and cognitive health support. Sports nutrition and beauty-focused applications are witnessing double-digit growth, fueled by fitness culture expansion, social media influence, and rising consumer interest in nutraceuticals that support skin health, collagen synthesis, and metabolic performance.

Explore more data points, trends and opportunities Download Free Sample Report

Natural Vitamins Market Segmentations

By Product Type

- Natural Vitamin A

- Natural Vitamin B

- Natural Vitamin C

- Natural Vitamin D

- Natural Vitamin E

- Natural Vitamin K

- Natural Multivitamin Blends

By Source

- Plant-Derived Vitamins

- Animal-Derived Vitamins

- Microbial/Fermentation-Derived Vitamins

By Form

- Tablets

- Capsules & Softgels

- Powders

- Liquids

- Gummies

By Application

- General Health & Immunity

- Bone & Joint Health

- Cardiovascular Health

- Cognitive Health

- Prenatal Care

- Beauty & Skin Health

- Sports Nutrition

By Distribution Channel

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Online Retail & E-commerce

- Direct-to-Consumer (DTC) Platforms

Regional Insights

North America

North America accounts for approximately 34% of global revenue in 2025, maintaining its leadership position due to high dietary supplement penetration rates, advanced healthcare awareness, and strong consumer purchasing power. The United States represents the majority of regional demand, supported by an established nutraceutical ecosystem, robust regulatory framework, and sophisticated e-commerce infrastructure that enables rapid product innovation and direct-to-consumer engagement. Preventive health culture, rising chronic disease prevalence, and widespread functional food integration further drive sustained growth. Canada contributes steady expansion, driven by clean-label preferences, transparent labeling regulations, and growing demand for plant-based and sustainably sourced vitamin formulations.

Europe

Europe holds nearly 29% share of the 2025 market, with Germany, France, the United Kingdom, and Italy serving as major contributors. Regional growth is strongly influenced by stringent quality standards, high consumer awareness regarding preventive healthcare, and strong environmental sustainability values. Germany leads regional production and export of plant-based vitamins, benefiting from advanced manufacturing infrastructure and research capabilities. Demand across Europe is further supported by aging demographics, increasing vegan adoption, and government-supported nutritional awareness initiatives. Regulatory harmonization across the European Union enhances cross-border trade and product standardization, strengthening regional market stability.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 11% CAGR. China and India are key demand centers, driven by expanding middle-class populations, rapid urbanization, rising disposable incomes, and government-led public health initiatives addressing micronutrient deficiencies. Increasing digital commerce penetration and domestic manufacturing capabilities further accelerate growth. Japan and South Korea represent mature yet innovation-driven markets characterized by strong consumer preference for high-quality, scientifically validated formulations and functional ingredients. The region’s growth trajectory is additionally supported by increasing sports participation, beauty supplementation trends, and growing awareness of preventive nutrition among younger demographics.

Latin America

Brazil and Mexico dominate regional demand, supported by improving healthcare access, rising awareness of immune health, and increasing imports of plant-based vitamin ingredients. Economic stabilization in key markets is gradually enhancing consumer spending on preventive healthcare products. Expanding online retail penetration and cross-border e-commerce platforms are improving product accessibility, particularly in urban centers. Although growth remains moderate compared to North America and Asia-Pacific, strengthening distribution networks and rising demand for affordable supplementation are contributing to steady market expansion.

Middle East & Africa

The Middle East & Africa region demonstrates emerging growth potential, with the United Arab Emirates and Saudi Arabia leading demand due to high disposable incomes, premium supplement adoption, and increasing lifestyle-related health concerns. Government investments in healthcare diversification and wellness infrastructure further stimulate market development. South Africa represents the primary African market, driven by expanding urban healthcare facilities, growing middle-class populations, and rising awareness of nutritional supplementation. While overall regional penetration remains comparatively lower, improving retail networks and increasing digital accessibility are expected to support long-term growth.

Key Players in the Natural Vitamins Market

- DSM-Firmenich

- BASF SE

- Amway Corp.

- Nestlé Health Science

- Nature’s Bounty

- Herbalife Ltd.

- NOW Foods

- Garden of Life

- Archer Daniels Midland Company

- Glanbia plc

- Himalaya Wellness

- Blackmores Ltd.

- Swisse Wellness

- MegaFood

- Nature’s Sunshine Products