Natural Vitamin C Supplement Market Size

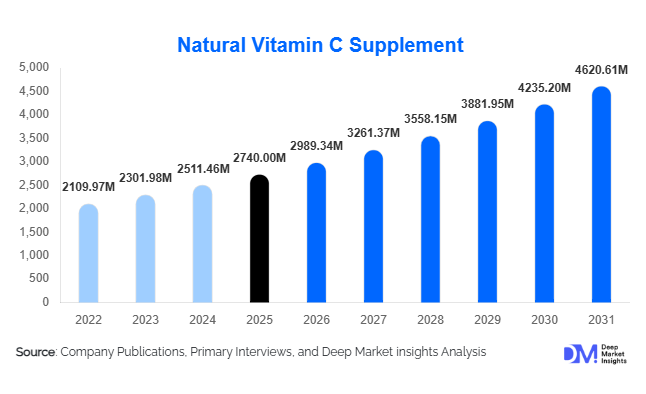

According to Deep Market Insights,the global natural vitamin C supplement market size was valued at USD 2,740 million in 2025 and is projected to grow from USD 2,989.34 million in 2026 to reach USD 4,620.61 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). Market growth is primarily driven by rising immunity awareness, increasing consumer preference for plant-based and clean-label supplements, and expanding applications across sports nutrition and preventive healthcare. Natural sources such as amla, acerola cherry, camu camu, and citrus extracts are gaining prominence over synthetic ascorbic acid due to perceived higher bioavailability and minimal processing.

Key Market Insights

- Plant-based and clean-label positioning is reshaping the supplement industry, with botanical vitamin C sources gaining higher consumer trust.

- Tablets remain the dominant format, while gummies and effervescent tablets are the fastest-growing delivery forms.

- North America leads global demand, supported by strong supplement culture and preventive healthcare spending.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income and domestic botanical production.

- Pharmacies and drug stores account for the largest distribution share, though online retail is rapidly expanding.

- Sports and active lifestyle consumers are emerging as a high-growth end-use segment, incorporating natural vitamin C into recovery and antioxidant formulations.

What are the latest trends in the natural vitamin C supplement market?

Shift Toward Botanical & Organic Sourcing

Consumers increasingly prefer vitamin C derived from natural sources such as acerola cherry and amla over synthetic alternatives. Organic certification, non-GMO labeling, and sustainable farming practices are becoming differentiators in premium product categories. Brands are investing in vertically integrated sourcing models to ensure traceability and quality control. This trend is especially strong in North America and Europe, where regulatory scrutiny and consumer awareness are high.

Advanced Delivery Formats & Liposomal Innovation

Manufacturers are adopting liposomal encapsulation and microencapsulation technologies to enhance absorption and bioavailability. Effervescent tablets, gummies, and liquid formulations are gaining popularity among pediatric and geriatric consumers. Personalized nutrition subscriptions and AI-based dosage recommendations are also emerging, positioning natural vitamin C supplements within the broader precision nutrition ecosystem.

What are the key drivers in the natural vitamin C supplement market?

Rising Immunity and Preventive Healthcare Awareness

Post-pandemic health consciousness has made immune support a daily priority for consumers. Natural vitamin C is widely recognized for its antioxidant and immune-enhancing properties, leading to year-round demand rather than seasonal spikes. Preventive health programs promoted by employers and governments further reinforce consumption patterns.

Growth in Sports Nutrition and Active Lifestyles

The expanding global sports nutrition industry, valued above USD 50 billion, is integrating natural antioxidants into recovery and performance products. Athletes and fitness enthusiasts are increasingly adopting higher dosage vitamin C (501–1000 mg range), driving premium product sales.

What are the restraints for the global market?

Raw Material Price Volatility

Botanical sources such as acerola and amla are sensitive to climatic fluctuations, impacting harvest yields and pricing stability. Volatile raw material costs can pressure manufacturer margins and influence retail pricing strategies.

Regulatory Variability Across Regions

Differing dietary supplement regulations in the U.S., EU, and Asia create compliance complexities. Labeling requirements, health claim restrictions, and ingredient approval standards can delay product launches and increase operational costs.

What are the key opportunities in the natural vitamin C supplement industry?

Integration with Public Health & Wellness Programs

Governments promoting preventive healthcare present institutional supply opportunities. Natural vitamin C supplements can be incorporated into elderly care programs, workplace wellness initiatives, and maternal health campaigns.

Emerging Market Expansion & Export Growth

Asia-Pacific and Latin America are experiencing double-digit consumption growth. India and Brazil, major producers of amla and acerola respectively, are strengthening export-driven supply chains to North America and Europe. Companies investing in organic certifications and sustainable sourcing can capture high-margin export demand.

Source Insights

The acerola cherry segment leads the global natural vitamin C supplements market, accounting for approximately 28% of total market share in 2025. Its leadership is primarily driven by its exceptionally high natural vitamin C concentration, superior bioavailability perception, and strong consumer preference for plant-derived ingredients. The widespread availability of acerola-based formulations across North America and Europe further strengthens its position, supported by clean-label trends and demand for minimally processed ingredients. Additionally, established supply chains in Latin America, particularly Brazil, ensure stable raw material sourcing and competitive pricing, reinforcing market dominance.

Amla-based supplements represent one of the fastest-expanding source categories, particularly across Asia-Pacific. Growth in this segment is supported by deep-rooted acceptance of traditional herbal medicine systems, including Ayurveda, where amla has long been recognized for immune and antioxidant benefits. Cost advantages in domestic cultivation, increasing export potential, and growing global awareness of Indian botanicals further accelerate adoption. The rising demand for multifunctional supplements that combine vitamin C with polyphenols and other phytonutrients also enhances the appeal of amla-based products globally.

Form Insights

Tablets dominate the market with nearly 32% share in 2025, primarily driven by consumer familiarity, affordability, longer shelf life, and ease of large-scale manufacturing. Their precise dosage standardization and convenience in bulk packaging make them particularly attractive for adult daily supplementation programs and institutional healthcare distribution. The leading driver behind tablet dominance is cost efficiency combined with strong retail penetration through pharmacies and supermarkets, where tablets remain the preferred format for immune health maintenance.

Gummies are the fastest-growing form segment, supported by rising demand for convenient, palatable, and easy-to-consume supplement options. Increased adoption among pediatric consumers and millennials is accelerating growth, as taste, portability, and lifestyle compatibility become key purchasing factors. Innovation in sugar-free, vegan, and naturally flavored gummies further expands their appeal, while social media marketing and D2C branding strategies significantly enhance visibility and consumer engagement.

Dosage Strength Insights

The 501 mg–1000 mg dosage category accounts for approximately 41% of the total market share, making it the leading strength segment. Its dominance is driven by the perception of balanced therapeutic effectiveness and safety, aligning with common daily recommended intake levels for immune support and antioxidant protection. Healthcare practitioner recommendations and standardized clinical guidelines often fall within this dosage range, reinforcing consumer trust and repeat purchases.

Products above 1000 mg are gaining traction, particularly among athletes, individuals with higher oxidative stress exposure, and immune-compromised consumers. The expansion of sports nutrition, increased awareness of recovery supplementation, and post-pandemic immune health prioritization are key drivers behind the growth of higher-dosage formulations.

Distribution Channel Insights

Pharmacies and drug stores account for nearly 35% of global sales, maintaining their leadership due to high consumer trust, pharmacist recommendations, and strong regulatory compliance standards. The primary growth driver for this segment is medical endorsement and credibility, particularly in developed markets where consumers rely on professional guidance for supplement selection. Strategic shelf placement, in-store promotions, and integration with healthcare services further strengthen this channel’s position.

Online retail channels represent over 25% of total sales and are expanding rapidly through direct-to-consumer platforms, subscription-based models, and global e-commerce marketplaces. The leading growth driver in this segment is convenience combined with wider product assortment and price transparency. Digital marketing strategies, influencer endorsements, and personalized recommendation algorithms significantly boost online conversion rates, particularly among younger demographics.

End-Use Insights

Adults aged 18–60 years represent approximately 52% of overall demand, making them the largest end-use segment. The leading driver behind this dominance is the widespread adoption of daily preventive healthcare practices and increasing awareness of immunity maintenance, stress management, and skin health benefits associated with vitamin C intake. Busy lifestyles and higher disposable incomes further contribute to routine supplementation within this demographic.

The sports and fitness segment is growing at over 11% CAGR, outpacing the overall market, driven by rising gym memberships, endurance sports participation, and recovery-focused nutrition strategies. Geriatric demand is expanding steadily due to aging populations in developed markets, increasing focus on immune resilience, and physician-recommended supplementation. Pediatric gummy formulations are emerging as a significant growth niche, supported by parental preference for palatable, easy-to-administer formats that encourage consistent intake.

| By Source | By Form | By Dosage Strength | By Distribution Channel | By End-Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, with the United States accounting for nearly three-fourths of regional demand. Growth in the region is primarily driven by a well-established supplement culture, high per capita healthcare expenditure, and strong preventive healthcare awareness. Post-pandemic consumer behavior continues to favor immune-support products, while premiumization trends encourage adoption of organic and non-GMO formulations. Advanced retail infrastructure, widespread e-commerce penetration, and continuous product innovation further reinforce regional leadership. Additionally, favorable regulatory clarity for dietary supplements supports new product launches and brand expansion.

Europe

Europe accounts for roughly 27% of global market share, with Germany, the U.K., and France serving as major consumption hubs. Regional growth is driven by stringent regulatory frameworks that enhance consumer confidence in product quality and safety. A strong preference for organic-certified and sustainably sourced supplements significantly influences purchasing behavior. Increasing aging populations, rising focus on preventive healthcare, and growing vegan and plant-based lifestyle adoption further accelerate demand. Expansion of pharmacy chains and cross-border e-commerce platforms also strengthens distribution efficiency across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at nearly 11% CAGR. China and India are the primary growth engines, supported by rising middle-class income, expanding urban populations, and increasing awareness of immunity and wellness products. Domestic botanical production capabilities, particularly for amla and other natural sources, provide cost advantages and strengthen local supply chains. Rapid digitalization, growing online retail adoption, and government initiatives promoting traditional medicine systems further contribute to market acceleration. Additionally, increasing sports participation and expanding healthcare access enhance long-term growth prospects.

Latin America

Brazil leads regional growth due to its strong acerola production base and expanding domestic supplement consumption. The availability of raw materials locally reduces production costs and supports export competitiveness. Rising health awareness, growing middle-income populations, and increased penetration of organized retail channels are key drivers across the region. Mexico and Argentina are witnessing gradual demand expansion, supported by improving healthcare infrastructure and increasing consumer interest in preventive nutrition.

Middle East & Africa

The UAE and South Africa are key markets within the region, driven by increasing health awareness, premium supplement adoption, and expanding urban populations. Growth is supported by rising disposable incomes, greater exposure to global wellness trends, and increasing availability of international brands through modern retail and online channels. Government initiatives promoting healthcare development and growing expatriate populations further stimulate demand for high-quality dietary supplements, positioning the region as an emerging opportunity market over the forecast period.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Vitamin C Supplement Market

- Amway Corp.

- Herbalife Ltd.

- Nature’s Bounty Co.

- NOW Foods

- Garden of Life

- Blackmores Ltd.

- Himalaya Wellness Company

- Nature’s Way Products LLC

- Solgar Inc.

- Swanson Health Products

- NutraMarks Inc.

- GNC Holdings

- DSM Nutritional Products

- Pharmavite LLC

- MegaFood