Natural Vitamin B12 Supplements Market Size

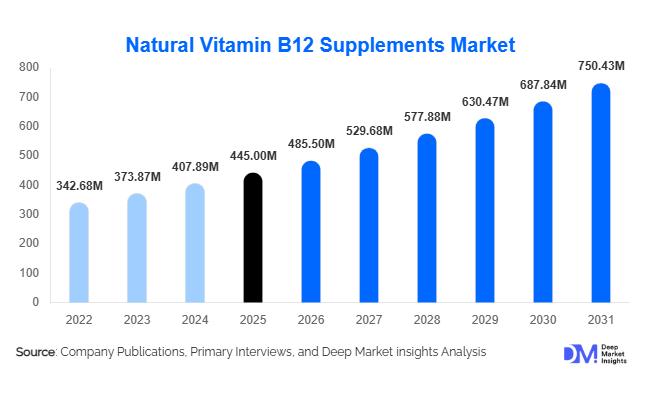

According to Deep Market Insights,the global natural vitamin B12 supplements market size was valued at USD 445 million in 2025 and is projected to grow from USD 485.50 million in 2026 to reach USD 750.43 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). Market growth is primarily driven by rising awareness of vitamin B12 deficiency, the rapid expansion of vegan and plant-based diets, and increasing preventive healthcare spending worldwide. Natural and fermentation-derived formulations are gaining preference over synthetic alternatives due to clean-label positioning, improved bioavailability, and sustainability considerations. Growing geriatric populations and expanding online supplement retail channels are further accelerating global demand.

Key Market Insights

- Methylcobalamin-based supplements dominate product demand due to superior bioavailability and neurological health benefits.

- Online retail channels are expanding rapidly, supported by subscription-based supplement models and direct-to-consumer brands.

- North America leads the global market, driven by high supplement penetration and diagnostic awareness of B12 deficiency.

- Asia-Pacific is the fastest-growing region, supported by rising middle-class income and expanding preventive healthcare awareness.

- Fermentation-derived natural B12 accounts for the majority of supply, offering scalable production and cost efficiency.

- Higher dosage formulations (1000 mcg and above) are increasingly prescribed for therapeutic deficiency correction.

What are the latest trends in the natural vitamin B12 supplements market?

Shift Toward Clean-Label & Plant-Based Supplementation

Consumers are increasingly preferring naturally fermented and algae-derived vitamin B12 supplements over synthetic alternatives. Clean-label positioning, non-GMO sourcing, and vegan certification are becoming important purchase criteria. Brands are investing in transparent sourcing and sustainability certifications to build trust. This trend aligns closely with the expansion of plant-based diets, particularly in North America and Europe, where vegan and flexitarian populations are steadily increasing. Companies are also reformulating products to remove artificial binders, preservatives, and allergens, reinforcing premium positioning.

Personalized & Digital Supplement Ecosystems

The rise of personalized nutrition platforms is transforming the supplement landscape. Digital health tools, at-home micronutrient testing kits, and AI-driven nutrition recommendations are driving customized vitamin B12 dosing strategies. Subscription-based models are expanding rapidly, offering consumers monthly deliveries tailored to their blood test results and dietary preferences. E-commerce marketplaces and brand-owned platforms are improving consumer access, while influencer-driven health education is strengthening awareness around B12 deficiency symptoms such as fatigue and cognitive decline.

What are the key drivers in the natural vitamin B12 supplements market?

Rising Global Prevalence of Vitamin B12 Deficiency

Vitamin B12 deficiency is increasingly diagnosed among elderly individuals, vegetarians, pregnant women, and patients with gastrointestinal disorders. Healthcare practitioners are recommending supplementation as part of preventive health regimens. The growing global geriatric population, particularly in North America, Europe, and Japan, is significantly contributing to sustained demand growth.

Growth of Vegan & Flexitarian Diets

Since vitamin B12 is primarily found in animal-based foods, plant-based consumers require supplementation. The rapid global adoption of vegan, vegetarian, and flexitarian diets has created a structural demand driver for natural B12 supplements. Plant-based branding enhances product positioning and pricing power.

Advancements in Bioavailability & Delivery Formats

Sublingual tablets, oral sprays, and liquid drops offer enhanced absorption compared to conventional tablets. Innovations in methylcobalamin formulations have improved efficacy, driving higher consumer retention and repeat purchases.

What are the restraints for the global market?

Raw Material Price Volatility

Natural vitamin B12 production relies on microbial fermentation processes, which are sensitive to fluctuations in raw material and energy costs. Price volatility can pressure margins, particularly for small and mid-sized manufacturers.

Regulatory Complexity Across Regions

Dietary supplement regulations vary widely across the U.S., Europe, and Asia. Differences in labeling requirements, permissible health claims, and quality standards create compliance challenges and increase time-to-market for new product launches.

What are the key opportunities in the natural vitamin B12 supplements industry?

Expansion in Emerging Asia-Pacific Markets

Countries such as India, China, Indonesia, and Vietnam are witnessing increased awareness of nutritional deficiencies. Expanding pharmacy retail networks and growing online supplement penetration create substantial growth opportunities. Public health campaigns targeting anemia and maternal nutrition further support structured demand.

Integration with Sports & Performance Nutrition

Vitamin B12 plays a critical role in energy metabolism and red blood cell formation, making it relevant for endurance athletes and active consumers. Integration into sports nutrition blends, protein supplements, and recovery formulas is opening new revenue streams beyond traditional health supplements.

Product Form Insights

Tablets continue to hold the largest share of the global market, accounting for approximately 35% of total revenue in 2025. The dominance of this segment is primarily driven by its cost efficiency, longer shelf life, ease of storage, and large-scale manufacturability, which make tablets highly suitable for both developed and emerging markets. Their precise dosage accuracy and widespread consumer familiarity further reinforce demand, particularly in pharmacy-led distribution channels. Capsules and softgels collectively represent a significant portion of the premium product landscape, supported by consumer preference for improved digestibility, enhanced absorption perception, and cleaner-label positioning. Softgels, in particular, benefit from their ability to encapsulate oil-based formulations and deliver smoother swallowing experiences. Sublingual tablets and oral sprays are emerging as the fastest-growing product formats, driven by increasing awareness of enhanced bioavailability and the need to address absorption challenges associated with gastrointestinal limitations. These formats are especially attractive for geriatric consumers and individuals with deficiency-related conditions. Gummies are steadily gaining traction among younger demographics and first-time supplement users due to their palatable taste profiles, convenience, and alignment with lifestyle-oriented wellness trends, further expanding the addressable consumer base.

Vitamin Type Insights

Methylcobalamin dominates the global market with nearly 42% share in 2025, supported by strong clinical preference for active-form supplementation and superior bioavailability compared to synthetic alternatives. Its direct involvement in neurological function and red blood cell formation makes it the preferred choice among healthcare practitioners and preventive health consumers. Adenosylcobalamin and hydroxocobalamin cater to specialized therapeutic applications, particularly in clinical deficiency treatment and injectable formulations, where targeted metabolic support is required. These variants maintain steady demand within hospital and practitioner-driven channels. Naturally fermented cyanocobalamin continues to hold a stable position in cost-sensitive markets due to its affordability, scalability in production, and long-standing regulatory acceptance. The leading position of methylcobalamin is primarily driven by increasing consumer education regarding active vitamin forms, rising neurological health concerns, and the premiumization of dietary supplements globally.

Distribution Channel Insights

Online retail accounts for approximately 33% of total global sales, reflecting the rapid digitalization of consumer purchasing behavior and the expansion of e-commerce platforms. The leading growth driver for this segment is the increasing consumer preference for convenience, subscription-based purchasing models, product comparison transparency, and access to a wide variety of clean-label and specialty formulations. Pharmacies and drugstores remain critical distribution channels, particularly for higher-dose and physician-recommended formulations, benefiting from strong consumer trust and professional guidance. Health and specialty stores continue to support premium, organic, and plant-based brands, aligning with wellness-focused consumer segments. Practitioner clinics and integrative health centers contribute to therapeutic-grade product demand, especially in cases requiring medically supervised supplementation. The omnichannel retail environment is further strengthening market penetration across diverse consumer groups.

End-Use Insights

Adults aged 18–50 represent approximately 40% of total demand, making this the leading end-use segment in 2025. Growth in this demographic is primarily driven by rising preventive healthcare adoption, increasing workplace stress, energy management needs, and lifestyle-related nutritional gaps. The geriatric population represents a high-growth segment due to age-related absorption challenges, increased prevalence of deficiency conditions, and expanding global life expectancy. Vegan and vegetarian consumers are expanding at double-digit growth rates as plant-based dietary patterns increase the risk of vitamin deficiencies, thereby necessitating supplementation. Sports nutrition applications are emerging as a fast-growing niche segment, supported by rising participation in fitness activities and performance optimization trends. The leading demand driver across end-use segments remains heightened awareness of preventive health management and personalized nutrition strategies.

| By Product Form | By Vitamin Type | By Source | By Distribution Channel | By End-Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 38% of the global market in 2025, led predominantly by the United States. Regional growth is driven by high dietary supplement penetration rates, strong preventive healthcare awareness, widespread clinical testing for deficiencies, and a well-established regulatory framework supporting product quality and innovation. The expanding vegan and flexitarian population further accelerates demand for supplementation. In Canada, steady market expansion is supported by aging demographics, increasing healthcare expenditure, and growing consumer preference for natural and clean-label health products. Advanced retail infrastructure and strong online commerce ecosystems continue to reinforce regional leadership.

Europe

Europe holds around 27% market share, with Germany, the United Kingdom, and France representing key consumption hubs. Regional growth is supported by strong adoption of plant-based diets, rising awareness of micronutrient deficiencies, and stringent regulatory standards that enhance product quality and consumer trust. An aging population across Western Europe is contributing to sustained demand for preventive and therapeutic supplementation. Additionally, increasing focus on sustainability and naturally sourced ingredients is encouraging product innovation and premium positioning across the region.

Asia-Pacific

Asia-Pacific represents nearly 22% of global demand and is the fastest-growing regional market, expanding at a CAGR exceeding 11%. China and India serve as major growth engines due to expanding middle-class populations, rising disposable incomes, and increasing awareness of anemia and nutritional deficiencies. Urbanization, improving healthcare infrastructure, and rapid digital commerce penetration are accelerating product accessibility. Government-led nutrition awareness programs and expanding pharmaceutical manufacturing capabilities further support regional growth momentum.

Latin America

Latin America accounts for approximately 8% of the global market, with Brazil and Mexico driving regional demand. Growth is supported by expanding pharmacy retail networks, increasing urban health awareness, and improving economic stability in major metropolitan areas. Rising prevalence of nutritional deficiencies and growing adoption of preventive healthcare practices are encouraging supplement consumption. E-commerce expansion is also enhancing product reach in underserved regions.

Middle East & Africa

The Middle East & Africa region represents about 5% of global demand. Market growth is supported by rising healthcare investment in the United Arab Emirates and South Africa, expanding private healthcare infrastructure, and increasing dietary supplement adoption among urban populations. Growing expatriate communities, higher disposable incomes in Gulf Cooperation Council countries, and rising awareness of micronutrient deficiencies are further contributing to steady market expansion across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Vitamin B12 Supplements Market

- Amway Corp.

- Nestlé Health Science

- Herbalife Nutrition Ltd.

- NOW Foods

- Nature’s Bounty Co.

- Garden of Life

- Solgar Inc.

- Pharmavite LLC

- DSM Nutritional Products

- Jamieson Wellness Inc.

- Nature’s Way Products LLC

- Himalaya Wellness Company

- Swanson Health Products

- Blackmores Ltd.

- GNC Holdings LLC