Natural Vanillin Market Size

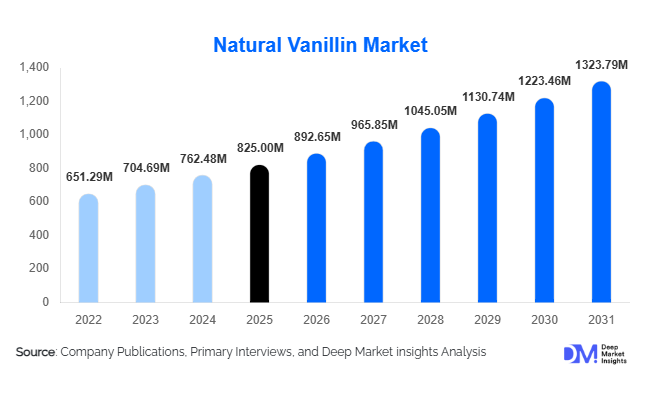

According to Deep Market Insights,the global natural vanillin market size was valued at USD 825 million in 2025 and is projected to grow from USD 892.65 million in 2026 to reach USD 1,323.79 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The natural vanillin market growth is primarily driven by rising clean-label demand, regulatory pressure to replace synthetic additives, and increasing adoption of bio-based flavor ingredients across food, beverage, pharmaceutical, and personal care industries. Advancements in fermentation-based production technologies are also narrowing the cost gap between natural and synthetic vanillin, further accelerating global adoption.

Key Market Insights

- Biotechnology-derived natural vanillin is gaining dominance, supported by scalable fermentation processes and stable supply chains.

- Food and beverage applications account for the majority share, driven by reformulation initiatives and premium product positioning.

- Europe leads the global market, supported by stringent labeling regulations and high clean-label penetration.

- Asia-Pacific is the fastest-growing region, fueled by expanding processed food industries in China and India.

- Powder form dominates due to longer shelf life, ease of transportation, and compatibility with dry food formulations.

- Direct B2B distribution remains the primary sales channel, with long-term procurement contracts between manufacturers and multinational food processors.

What are the latest trends in the natural vanillin market?

Shift Toward Fermentation-Based Natural Vanillin

One of the most transformative trends in the natural vanillin market is the rapid adoption of fermentation-based production. Manufacturers are increasingly utilizing bio-fermentation processes derived from ferulic acid and eugenol to produce vanillin that meets regulatory definitions of “natural.” This shift reduces dependency on volatile vanilla bean harvests and improves supply stability. Advanced microbial engineering and process optimization have enhanced yields and reduced production costs, enabling large-scale commercialization. Companies are investing in sustainable feedstocks and carbon-neutral production pathways, aligning with global ESG objectives and strengthening long-term supply resilience.

Premiumization and Clean-Label Reformulation

Food and beverage brands are actively reformulating product portfolios to eliminate artificial flavors and adopt natural ingredients. Natural vanillin is increasingly used in premium chocolates, bakery items, plant-based dairy alternatives, and specialty beverages. Consumer preference for transparent labeling and plant-derived ingredients is driving higher willingness to pay for natural formulations. In parallel, cosmetic and fragrance manufacturers are shifting toward naturally sourced aroma compounds to support clean beauty claims. This premiumization trend is elevating natural vanillin from a niche ingredient to a mainstream industrial flavor solution.

What are the key drivers in the natural vanillin market?

Growing Clean-Label Consumer Demand

Consumers globally are scrutinizing ingredient lists and actively avoiding synthetic additives. Regulatory bodies in North America and Europe are tightening standards around flavor labeling, compelling manufacturers to transition toward natural alternatives. Natural vanillin enables brands to claim “no artificial flavors,” significantly influencing purchasing decisions in bakery, dairy, confectionery, and beverage segments. This structural shift in consumer behavior is creating sustained long-term demand.

Expansion of Processed and Premium Food Industries

The global expansion of processed foods, specialty confectionery, and premium dairy products is directly supporting vanillin demand. Rising disposable incomes in Asia-Pacific and the Middle East are boosting consumption of packaged desserts and flavored beverages. Natural vanillin enhances flavor authenticity and supports premium positioning, allowing manufacturers to achieve higher margins while meeting evolving consumer expectations.

What are the restraints for the global market?

High Production Costs Compared to Synthetic Vanillin

Natural vanillin remains significantly more expensive than petrochemical-derived synthetic variants. Vanilla bean cultivation is geographically concentrated and vulnerable to climate disruptions, while fermentation production requires high capital expenditure. This price differential limits adoption in cost-sensitive markets and mass-market product categories.

Raw Material Price Volatility

Vanilla bean supply, particularly from Madagascar, is subject to extreme price fluctuations due to climatic events and geopolitical instability. Although fermentation reduces dependency, feedstock costs such as ferulic acid and eugenol can also fluctuate, impacting overall profit margins and procurement planning.

What are the key opportunities in the natural vanillin industry?

Biotechnology and Sustainable Production Investments

Investments in advanced fermentation facilities present strong growth opportunities. Governments promoting bio-based chemicals under initiatives such as “Make in India” and “Made in China 2025” are supporting domestic production capabilities. Companies that scale sustainable and carbon-neutral fermentation processes can gain competitive advantage and secure long-term supply contracts with multinational brands.

Expansion in Emerging Markets

Rapid urbanization and growing processed food consumption in China, India, Southeast Asia, Brazil, and the Middle East create untapped demand. Establishing regional production hubs reduces import dependency and logistics costs, enhancing competitiveness. Export-driven growth toward high-value markets such as the United States and Germany also presents strong revenue potential for emerging manufacturers.

Source Type Insights

Biotechnology-derived natural vanillin holds approximately 38% of the 2025 market share, making it the leading source segment. Its dominance is primarily driven by scalability, stable year-round supply, cost efficiency compared to traditional extraction, and compliance with global natural labeling regulations. Fermentation-based production methods enable manufacturers to meet growing clean-label demand while maintaining consistent purity and aroma intensity. Ferulic acid-based production is expanding rapidly due to its optimized conversion efficiency and lower raw material cost, strengthening its adoption among large-scale food ingredient manufacturers.

Vanilla bean-derived natural vanillin maintains a premium niche position, supported by demand from luxury chocolate manufacturers, artisanal bakery producers, and high-end confectionery brands. Although supply volatility and higher production costs limit large-scale adoption, its authentic flavor profile and strong consumer perception as “true natural” sustain demand in premium product categories.

Form Insights

Powder-based natural vanillin accounts for nearly 62% of the 2025 market, making it the leading form segment. Growth in this segment is driven by its longer shelf life, improved stability under varying storage conditions, reduced transportation costs, and ease of blending in dry formulations. Powder form is especially preferred in bakery premixes, confectionery coatings, dairy powders, and nutraceutical blends, where uniform dispersion and precise dosing are critical.

Liquid forms are widely used in beverages, flavored syrups, dairy drinks, and pharmaceutical suspensions due to their rapid solubility and ease of integration into aqueous systems. Encapsulated formats are gaining traction in high-value controlled-release and heat-stable applications, particularly in functional foods, fortified bakery products, and premium confectionery items where aroma retention during processing is essential.

Application Insights

Food and beverages dominate the market with around 68% share in 2025, making it the leading application segment. This dominance is driven by rising consumer preference for clean-label and natural flavoring ingredients across packaged foods. Bakery and confectionery represent the largest sub-segment within this category, accounting for approximately 34% of total demand. Growth in this segment is supported by expanding premium chocolate production in Europe, rising artisanal bakery chains in North America, and increasing dairy dessert consumption in Asia-Pacific.

Dairy products, beverages, and frozen desserts are experiencing accelerated growth due to increasing product innovation, including plant-based alternatives and reduced-sugar formulations that rely on natural flavor enhancers. Additionally, nutraceutical beverages and protein-enriched drinks are incorporating natural vanillin to improve palatability and consumer acceptance.

Distribution Channel Insights

Direct B2B sales represent nearly 70% of global revenue, reflecting strong long-term procurement partnerships between flavor manufacturers and multinational food processors. Large-scale buyers prioritize supply reliability, technical customization, and regulatory documentation, which supports the dominance of direct contracts.

Specialty ingredient distributors play a critical role in serving small and mid-sized food manufacturers by offering flexible order volumes and regional warehousing capabilities. Online ingredient platforms are gradually expanding access for artisanal producers, specialty bakeries, and emerging brands, particularly in North America and Europe, where digital procurement adoption is increasing.

End-Use Industry Insights

The bakery and confectionery industry remains the primary consumer of natural vanillin, supported by global bakery market growth exceeding 5% annually. The segment’s leadership is driven by consistent demand for flavor standardization, premium product positioning, and increased global consumption of chocolates, cookies, pastries, and filled desserts.

Dairy and frozen desserts represent one of the fastest-growing end-use segments, expanding at over 8% CAGR due to rising plant-based product adoption and innovation in flavored yogurts, ice creams, and protein-enriched dairy beverages. The fragrance and cosmetics industry is emerging as a high-margin segment, leveraging natural aroma compounds to meet clean beauty and sustainability trends. Pharmaceutical syrups and nutraceutical supplements also contribute incremental growth, particularly in export-oriented markets where natural excipients improve product positioning.

| By Source Type | By Form | By Application | By Distribution Channel | By Region |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 28% of the 2025 market share, led by the United States. Regional growth is driven by strong clean-label penetration, strict food safety regulations, and high consumer awareness regarding ingredient transparency. The presence of advanced food processing infrastructure and major flavor manufacturers further supports demand. Canada contributes steadily through premium bakery production, specialty beverages, and expanding plant-based dairy alternatives. Increasing innovation in functional foods and protein beverages is also accelerating regional consumption.

Europe

Europe leads globally with around 32% market share in 2025. Germany, France, Switzerland, and the UK are key demand centers due to their advanced chocolate, confectionery, and bakery industries. Regional growth is strongly supported by stringent EU labeling regulations favoring natural flavor adoption over synthetic alternatives. Additionally, high consumer preference for sustainably sourced ingredients and the presence of premium chocolate manufacturers drive consistent demand. Innovation in organic and clean-label food products further strengthens Europe’s leadership position.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 9% CAGR. China and India are major demand drivers, supported by rapid expansion of processed food industries, rising disposable incomes, and growing urbanization. Increasing domestic fermentation capacity enhances supply security and cost competitiveness. Japan and South Korea show steady premium confectionery demand, while Southeast Asian countries are witnessing increased investments in bakery chains and beverage manufacturing. The growing adoption of Western-style desserts and dairy consumption further accelerates market expansion.

Latin America

Latin America represents about 6–7% of global demand, led by Brazil and Mexico. Regional growth is supported by expanding bakery and carbonated beverage industries, rising urban middle-class populations, and increasing investments in domestic food processing. Growing export activities of flavored dairy and confectionery products are gradually strengthening demand for natural flavoring agents.

Middle East & Africa

The Middle East & Africa account for approximately 4–5% share of the global market. The UAE and South Africa are key markets, driven by premium confectionery imports, expanding hospitality sectors, and rising investments in food processing infrastructure. Increasing demand for halal-certified natural ingredients and the expansion of international bakery chains are expected to support steady regional growth over the forecast period.

Company Market Share

The natural vanillin market is moderately consolidated, with the top five companies accounting for approximately 52% of global revenue. Leading players maintain competitive advantage through fermentation technology investments, sustainable sourcing strategies, and long-term supply agreements with multinational food and fragrance brands.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Vanillin Market

- Givaudan

- Firmenich

- Symrise AG

- International Flavors & Fragrances (IFF)

- Takasago International Corporation

- Mane SA

- Solvay

- Evolva

- Advanced Biotech

- Lesaffre

- Prova

- Van Aroma

- Aurochemicals

- Camlin Fine Sciences

- Apple Flavor & Fragrance Group