Natural Vanillin for Beverage Market Size

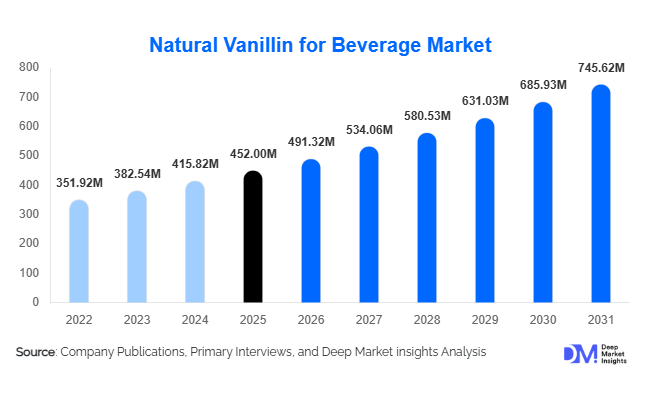

According to Deep Market Insights,the global natural vanillin for beverage market size was valued at USD 452 million in 2025 and is projected to grow from USD 491.32 million in 2026 to reach USD 745.62 million by 2031, expanding at a CAGR of 8.7% during the forecast period (2026–2031). Market growth is primarily driven by rising clean-label reformulation across beverage categories, accelerating demand for plant-based and functional drinks, and technological advancements in bio-fermentation that are narrowing the price gap between natural and synthetic vanillin.

Key Market Insights

- Bio-fermentation-derived vanillin leads the source segment, accounting for nearly 34% of total market share in 2025 due to scalability and cost efficiency.

- Liquid water-soluble natural vanillin dominates by form, representing approximately 46% share, driven by seamless integration in beverage production lines.

- RTD coffee & tea applications account for nearly 28% of demand, supported by premiumization and flavored cold brew expansion.

- North America holds around 31% of global revenue share, led by U.S. clean-label beverage reformulation.

- Asia-Pacific is the fastest-growing region, projected to expand at over 10% CAGR through 2031.

- Top five companies collectively hold about 48% of the global market, reflecting moderate consolidation and strong technology-driven competition.

What are the latest trends in the natural vanillin for beverage market?

Clean-Label Reformulation Accelerating Across Beverage Categories

Beverage manufacturers globally are reformulating product portfolios to remove artificial flavors and additives. Natural vanillin is increasingly used to enhance sweetness perception and deliver flavor depth in low-sugar and sugar-reduced beverages. Regulatory tightening in developed markets and consumer preference for recognizable ingredients are accelerating the shift. Beverage brands are prominently labeling “naturally flavored” claims, making natural vanillin a strategic ingredient in carbonated drinks, flavored milk, and plant-based beverages. This trend is particularly strong in North America and Europe, where retail buyers demand ingredient transparency and traceability certifications.

Bio-Fermentation Technology Scaling Rapidly

Technological innovation in fermentation-derived vanillin production has improved yield efficiency and consistency. Companies are investing in precision fermentation platforms using renewable feedstocks such as ferulic acid and lignin derivatives. This has reduced production costs and improved supply reliability compared to traditional vanilla bean extraction. The scalability of fermentation processes enables long-term supply contracts with multinational beverage manufacturers, making bio-based vanillin the preferred choice for high-volume applications.

What are the key drivers in the natural vanillin for beverage market?

Growth of RTD and Functional Beverage Industries

The rapid expansion of ready-to-drink coffee, tea, energy drinks, and fortified beverages is a major demand catalyst. RTD beverages require consistent flavor profiles and aroma stability, areas where natural vanillin performs effectively. With the global RTD beverage market exceeding USD 110 billion and growing at mid-single-digit rates, flavor ingredient suppliers are benefiting directly from increased production volumes.

Premiumization and Sensory Enhancement Demand

Consumers are seeking premium beverage experiences with sophisticated flavor layering. Natural vanillin enhances mouthfeel and sweetness perception, enabling sugar reduction without compromising taste. Premium dairy beverages, specialty cold brews, and flavored plant-based drinks are key beneficiaries of this trend.

What are the restraints for the global market?

Price Premium Over Synthetic Vanillin

Natural vanillin remains priced between 2.5x to 4x higher than synthetic alternatives. In cost-sensitive markets, beverage manufacturers may delay reformulation unless regulatory or branding advantages justify the premium.

Raw Material Price Volatility

Feedstock dependency on agricultural derivatives such as ferulic acid and vanilla beans exposes producers to supply fluctuations. Climate variability and agricultural yield changes can impact production economics and margins.

What are the key opportunities in the natural vanillin for beverage industry?

Expansion in Plant-Based Beverage Segment

Plant-based milk alternatives, valued at over USD 25 billion globally, are growing at nearly 9% CAGR. These beverages require flavor masking and sweetness enhancement, creating strong incremental demand for natural vanillin. Localized fermentation production in Asia presents opportunities for new entrants.

Sustainability-Driven Procurement Strategies

Major beverage corporations are integrating ESG and Scope 3 emission targets into supplier selection processes. Natural vanillin derived from lignin valorization and renewable fermentation feedstocks aligns with circular economy models. Suppliers with carbon footprint documentation and clean-label certifications can secure long-term contracts and premium pricing.

Source Insights

Bio-fermentation-derived vanillin dominates the global natural vanillin for beverage applications market, accounting for approximately 34% of total market share in 2025. The segment’s leadership is primarily driven by its superior scalability, consistent purity profile, and improving cost competitiveness compared to traditional extraction methods. Beverage manufacturers increasingly prefer bio-fermentation due to its ability to meet clean-label requirements while ensuring batch-to-batch consistency — a critical factor for large-scale RTD beverage production.

Ferulic acid–derived vanillin follows closely, supported by stable industrial feedstock availability and relatively predictable pricing structures. This source benefits from well-established supply chains and industrial manufacturing infrastructure, particularly in Europe and Asia-Pacific.Vanilla bean–extracted vanillin remains a niche yet premium segment due to higher production costs, agricultural dependency, and limited scalability. However, it commands strong positioning in ultra-premium beverages, specialty coffee formulations, craft sodas, and luxury dairy-based drinks where authentic origin claims enhance product differentiation.

Form Insights

Liquid water-soluble natural vanillin accounts for nearly 46% of global demand, making it the leading form segment. The segment’s dominance is driven by beverage manufacturers’ preference for ready-to-use formats that integrate seamlessly into high-speed blending, mixing, and homogenization processes. Liquid formats reduce formulation complexity, improve dispersion efficiency, and minimize production downtime — key advantages in large-scale beverage manufacturing.

Powder forms represent a substantial share, particularly in dry beverage premixes, instant coffee blends, protein drink powders, and concentrated formulations. Their longer shelf life and ease of storage make them attractive for export-oriented producers.Encapsulated vanillin formats are gaining momentum due to enhanced thermal stability, controlled flavor release, and protection against oxidation. These characteristics are particularly valuable in UHT-treated dairy beverages, high-temperature processing applications, and extended shelf-life functional drinks.

Application Insights

RTD coffee and tea lead the application landscape with approximately 28% share of global consumption in 2025. The leading segment driver is the rapid innovation in flavored cold brew coffee, specialty iced lattes, and milk-based tea beverages across Asia-Pacific and North America. Premiumization trends, café-style beverage replication, and demand for indulgent yet clean-label flavors continue to strengthen natural vanillin adoption in this segment.

Dairy-based beverages account for nearly 22% share, supported by flavored milk expansion, protein-enriched drinks, and lactose-free dairy innovations. Natural vanillin enhances creaminess perception while supporting sugar-reduction strategies, making it highly valuable in reformulated dairy beverages.Plant-based beverages represent one of the fastest-growing application areas, expanding at double-digit rates in select markets. Growth is fueled by rising vegan populations, lactose intolerance awareness, and sustainability-driven consumption. Natural vanillin plays a crucial role in masking off-notes from plant proteins such as soy, pea, and almond, improving overall sensory appeal.

Distribution Channel Insights

Direct sales to beverage manufacturers dominate the market, accounting for approximately 62% of total share. This leadership is driven by long-term procurement contracts, volume-based pricing agreements, and collaborative product development initiatives between ingredient suppliers and major beverage brands. Direct sourcing ensures quality assurance, supply stability, and regulatory compliance.Ingredient distributors maintain a strong presence in emerging markets, where small- and mid-sized beverage producers rely on regional supply networks. Distributors play a critical role in logistics management, technical support, and customized formulation services, particularly in Asia-Pacific, Latin America, and the Middle East.

| By Source | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for roughly 31% of the global market in 2025, led by the United States, which contributes nearly 24% of total revenue. Regional growth is driven by strong clean-label demand, sugar-reduction initiatives, and continuous premium beverage innovation. The rapid expansion of RTD coffee, plant-based dairy alternatives, and functional beverages further accelerates natural vanillin adoption.Regulatory clarity from the U.S. Food and Drug Administration (FDA) regarding natural flavor labeling strengthens market confidence. Additionally, advanced beverage processing infrastructure and strong R&D investment by major beverage corporations support sustained demand growth. Canada shows steady expansion, supported by rising plant-based drink consumption and increasing health-conscious consumer preferences.

Europe

Europe holds approximately 29% share, with Germany, France, and the United Kingdom leading regional demand. Growth is primarily driven by strict labeling regulations, sustainability mandates, and heightened consumer awareness regarding artificial additives.The European Union’s regulatory framework on flavor transparency and sustainability reporting is accelerating the shift toward naturally derived flavor ingredients. Furthermore, strong demand for organic-certified beverages, reduced-sugar dairy drinks, and premium artisanal coffee products supports continued market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing region, projected to expand at over 10% CAGR through the forecast period. China and India are key high-growth markets, driven by rapidly expanding RTD beverage industries, urbanization, and rising middle-class disposable incomes.Growth drivers include the surge in milk tea chains, cold coffee culture adoption, flavored yogurt drinks, and increasing Western beverage influence. Japan remains innovation-driven, particularly in premium flavored beverages and functional drinks, where high-quality natural flavor ingredients are strongly preferred.Expanding domestic beverage manufacturing capacity and improving ingredient supply chains further enhance regional market scalability.

Latin America

Brazil and Mexico lead regional demand, supported by strong consumption of flavored dairy drinks, carbonated soft beverages, and affordable indulgence products. Market growth remains moderate but steady, driven by expanding urban populations and increasing penetration of packaged beverages.Improving retail infrastructure, rising modern trade channels, and growing youth demographics contribute to flavor innovation in the region. Cost-sensitive manufacturers increasingly adopt bio-fermentation-derived vanillin to balance affordability with natural labeling claims.

Middle East & Africa

The UAE and Saudi Arabia are emerging premium beverage hubs, supported by high per-capita income levels and rapid expansion of specialty coffee chains. South Africa drives regional beverage processing demand due to its established manufacturing base.l̥l̥Regional growth is supported by beverage diversification strategies, tourism-driven premium consumption, and rising demand for halal-certified natural ingredients. Increasing investment in food and beverage manufacturing infrastructure across Gulf Cooperation Council (GCC) countries further supports long-term market potential.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Vanillin for Beverage Market

- Givaudan

- Firmenich

- Symrise AG

- International Flavors & Fragrances Inc.

- MANE

- Solvay

- Borregaard

- Evolva

- Advanced Biotech

- Lesaffre

- Apple Flavor & Fragrance Group

- Omega Ingredients

- Prinova Group

- Treatt PLC

- Aurochemicals