Natural Stabilizer Market Size

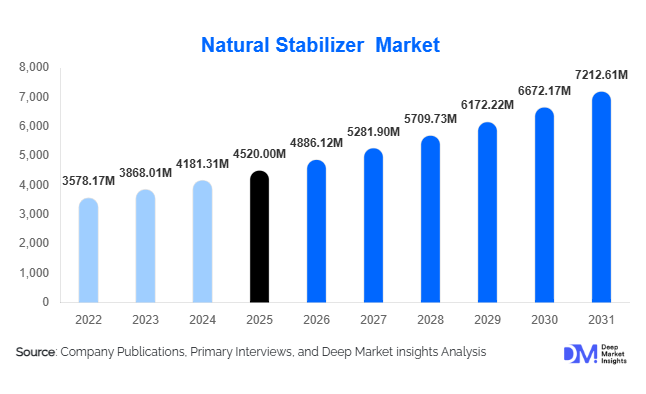

According to Deep Market Insights,the global natural stabilizer market size was valued at USD 4,520 million in 2025 and is projected to grow from USD 4,886.12 million in 2026 to reach USD 7,212.61 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The natural stabilizer market growth is primarily driven by rising demand for clean-label food ingredients, rapid expansion of plant-based dairy and alternative protein products, and increasing reformulation efforts to replace synthetic emulsifiers and artificial additives.

Key Market Insights

- Plant-based stabilizer account for nearly 48% of the global market, driven by clean-label positioning and wide applicability across dairy and beverages.

- Dairy and dairy alternatives represent the largest end-use segment, contributing approximately 34% of total market demand in 2025.

- Powdered stabilizer dominate with over 70% share, supported by longer shelf life and ease of industrial handling.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR due to food processing expansion in China and India.

- Top five companies collectively hold about 42% market share, reflecting moderate consolidation and strong technological competition.

- Export-driven processed food production in emerging economies is accelerating demand for globally compliant natural stabilizer blends.

What are the latest trends in the natural stabilizer market?

Clean-Label Reformulation Across Processed Foods

Food manufacturers globally are reformulating product portfolios to eliminate artificial stabilizers, synthetic emulsifiers, and chemically modified additives. Natural stabilizer derived from plant, marine, and fermentation sources are increasingly replacing traditional synthetic ingredients. Major dairy brands, bakery producers, and beverage companies are highlighting “no artificial additives” and “natural texture” on product labels. This shift is particularly pronounced in North America and Europe, where regulatory scrutiny and consumer awareness are highest. Reformulation initiatives are also pushing suppliers to develop allergen-free, non-GMO, and organic-certified stabilizer blends tailored to premium product lines.

Growth of Plant-Based and Alternative Protein Applications

The rapid expansion of plant-based milk, yogurt alternatives, protein beverages, and meat substitutes is transforming stabilizer demand. Natural stabilizer play a critical role in protein suspension, viscosity control, creaminess enhancement, and emulsion stability. Oat, almond, and soy beverages require multi-functional hydrocolloid blends to prevent phase separation and improve mouthfeel. As plant-based product launches accelerate globally, stabilizer suppliers are collaborating closely with food innovators to co-develop customized texture solutions. This trend is expanding beyond dairy alternatives into functional beverages and high-protein snacks.

What are the key drivers in the natural stabilizer market?

Rising Demand for Clean and Transparent Ingredients

Consumers increasingly prioritize transparency in ingredient lists. Natural stabilizers such as pectin, guar gum, xanthan gum, carrageenan, and alginates are perceived as safer and more sustainable compared to synthetic counterparts. Regulatory frameworks in the U.S. and Europe are reinforcing this transition, encouraging manufacturers to adopt natural-origin functional ingredients. The clean-label movement has therefore become a foundational growth driver for the natural stabilizer market.

Expansion of Global Dairy and Dairy Alternatives Industry

The global dairy industry, valued at over USD 900 billion, continues to evolve with premiumization and functional innovations. Yogurts, flavored milks, frozen desserts, and plant-based dairy alternatives require stabilizers for texture, moisture retention, and shelf-life extension. The double-digit growth of plant-based milk categories in Asia-Pacific and North America significantly strengthens stabilizer demand, particularly for advanced emulsifying and gelling.

What are the restraints for the global market?

Raw Material Price Volatility

Natural hydrocolloids are often derived from agricultural and marine sources. Climatic fluctuations, crop yield variability, and geopolitical trade disruptions can impact guar gum, carrageenan, and alginate prices. Price volatility affects procurement planning and compresses margins for stabilizer manufacturers.

Regulatory Debates Around Specific Hydrocolloids

In certain regions, regulatory reviews and consumer debates regarding specific gums, particularly carrageenan, have created formulation uncertainty. Companies must continuously invest in compliance testing and reformulation to mitigate regulatory risks.

What are the key opportunities in the natural stabilizer industry?

Customization and Premium Functional Blends

Food manufacturers increasingly require application-specific stabilizer rather than single-ingredient solutions. Suppliers who offer customized blends tailored to viscosity, freeze-thaw stability, or protein compatibility can command premium margins. This specialization creates differentiation opportunities and long-term supply partnerships with multinational food companies.

Emerging Market Food Processing Expansion

Rapid industrialization of food processing in India, China, Brazil, and Southeast Asia presents significant growth opportunities. Export-oriented processed food producers require globally compliant, high-performance stabilizer. Establishing regional blending plants and technical application centers in these markets can unlock long-term competitive advantages.

Ingredient Source Insights

Plant-based stabilizer dominate the global natural stabilizer market, accounting for approximately 48% share in 2025. The leadership of this segment is primarily driven by accelerating clean-label demand, regulatory preference for naturally derived ingredients, and broad raw material availability across multiple geographies. Pectin, guar gum, and locust bean gum blends are widely adopted across dairy, dairy-alternative, bakery, and beverage applications due to their strong functionality in texture control, viscosity modulation, and moisture retention. The rising consumer shift toward plant-based diets and minimally processed foods has further strengthened demand for plant-origin hydrocolloids. Marine-based stabilizers such as carrageenan and alginates maintain stable demand in dairy desserts, chocolate milk, processed meats, and ready-to-eat foods owing to their strong gelling and water-binding properties. Fermentation-based including xanthan gum and gellan gum are witnessing steady growth, particularly in beverages and sauces where suspension stability, phase separation prevention, and uniform mouthfeel are critical. The expansion of functional beverages and premium sauces continues to support the growth trajectory of fermentation-derived stabilizers.

Functional Application Insights

Emulsifying and stabilizing blends represent the leading functional segment with around 32% share of the 2025 market. The dominance of this segment is primarily driven by rapid expansion in plant-based beverages, flavored dairy products, and protein-fortified drinks that require stable dispersion of fats and proteins. These play a critical role in maintaining homogeneity, preventing sedimentation, and enhancing product shelf stability under varying storage conditions. Thickening and gelling follow closely, supported by strong demand in bakery fillings, confectionery gels, dairy desserts, and fruit preparations where texture consistency and structural integrity are essential. Increasing innovation in reduced-sugar and low-fat formulations has further elevated the importance of multifunctional stabilizer that deliver viscosity, mouthfeel, and stability simultaneously. As manufacturers focus on product differentiation through texture optimization, demand for tailored stabilizer blends continues to expand.

Form Insights

Powdered stabilizer account for nearly 72% of the global market, making them the dominant form segment. The leading position of powdered formats is driven by extended shelf life, ease of transportation, reduced microbial risk, and compatibility with automated dosing used in large-scale food manufacturing facilities. Powders offer precise formulation control, improved storage efficiency, and lower logistics costs, making them the preferred choice for industrial processors. Additionally, powdered allow for customized blending and easy integration into dry premixes. Liquid stabilizer are gradually gaining traction in beverage and ready-to-drink manufacturing, particularly where rapid solubility and process convenience are prioritized. However, higher storage costs and shorter shelf stability continue to limit their overall market share relative to powders.

End-Use Industry Insights

Dairy and dairy alternatives hold approximately 34% of total demand in 2025, making them the largest end-use segment. The leadership of this segment is driven by growing consumption of yogurt, flavored milk, cheese spreads, plant-based milk, and frozen desserts, all of which rely heavily on stabilizers for texture, viscosity, and shelf-life enhancement. The rapid expansion of plant-based dairy substitutes has further accelerated demand for advanced stabilizer blends that can replicate traditional dairy mouthfeel. Bakery and confectionery represent a significant share of the market, supported by the need for moisture retention, crumb softness, filling stability, and extended product freshness. The meat and plant-based meat segment is among the fastest-growing categories as manufacturers increasingly utilize natural binders and water-holding agents to improve yield, texture, and product integrity while meeting clean-label standards. The rise in convenience foods and ready-to-eat meals further strengthens demand across multiple end-use industries.

| By Ingredient Source | By Functional Application | By Form | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds nearly 28% of the global market in 2025, led by strong demand in the United States and supported by Canada. Regional growth is primarily driven by high clean-label adoption, strong consumer awareness regarding ingredient transparency, and advanced food processing infrastructure. The rapid expansion of plant-based dairy and meat alternatives, combined with continuous product innovation from established food brands, significantly boosts stabilizer demand. Additionally, well-developed cold chain logistics, large-scale industrial food production, and strong research and development investments further support regional market expansion.

Europe

Europe accounts for approximately 25% of global demand, with Germany, France, the United Kingdom, and the Netherlands serving as key markets. Growth in the region is strongly influenced by stringent additive regulations that encourage the use of natural and minimally processed ingredients. Consumer preference for organic, non-GMO, and clean-label products drives consistent demand for plant-based stabilizers. Europe’s mature dairy industry, expanding plant-based beverage segment, and strong bakery sector further reinforce stabilizer consumption. Innovation in reformulation strategies aimed at reducing sugar, fat, and synthetic additives also acts as a major regional growth driver.

Asia-Pacific

Asia-Pacific leads the global market with roughly 30% share and remains the fastest-growing region at over 9.5% CAGR. China and India are expanding food processing capacities and increasing investments in packaged food manufacturing, significantly driving stabilizer demand. Rising urbanization, growing middle-class populations, and increasing consumption of convenience foods further stimulate market growth. Japan and South Korea contribute through demand for premium texture used in high-quality dairy desserts, beverages, and functional foods. The rapid development of local dairy alternatives and ready-to-drink beverage industries continues to accelerate regional expansion.

Latin America

Latin America contributes about 8% of global demand, with Brazil and Mexico leading the regional market. Growth is supported by strong processed meat production, expanding dairy exports, and increasing consumption of packaged bakery products. Rising investments in food manufacturing infrastructure and export-oriented production strategies further drive stabilizer adoption. Growing awareness of natural ingredients and gradual modernization of retail channels also contribute to steady regional demand.

Middle East & Africa

The Middle East & Africa region holds approximately 9% share of the global market. Growth is supported by expanding dairy processing capacity in Saudi Arabia and the United Arab Emirates, along with increasing packaged food production in South Africa. Rising population levels, higher disposable incomes in Gulf countries, and growing demand for shelf-stable food products contribute to stabilizer consumption. Additionally, investments in food security initiatives and domestic food manufacturing capabilities further strengthen regional market potential.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Company Market Share

The natural stabilizer market is moderately consolidated, with the top five companies collectively accounting for approximately 42% of the global market. Competitive positioning is largely influenced by product innovation, customized formulation capabilities, strong technical support services, and efficient raw material sourcing strategies. Companies are increasingly focusing on developing multifunctional stabilizer blends that align with clean-label trends while maintaining cost efficiency. Strategic partnerships with food manufacturers, expansion into emerging markets, and continuous research and development investments remain central to sustaining competitive advantage in the global market.

Key Players in the Natural Stabilizer Market

- Cargill, Incorporated

- Kerry Group plc

- Tate & Lyle PLC

- Ingredion Incorporated

- CP Kelco

- DuPont Nutrition & Biosciences

- Ashland Global Holdings Inc.

- DSM-Firmenich

- Darling Ingredients

- Palsgaard A/S

- Nexira

- TIC Gums

- Fiberstar, Inc.

- Jungbunzlauer Suisse AG

- Naturex