Natural Multivitamin and Minerals Market Size

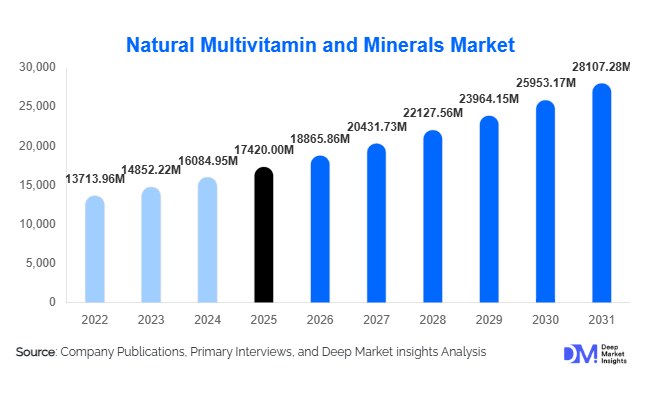

According to Deep Market Insights,the global natural multivitamin and minerals market size was valued at USD 17,420 million in 2025 and is projected to grow from USD 18,865.86 million in 2026 to reach USD 28,107.28 million by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). Market growth is primarily driven by rising preventive healthcare awareness, increasing preference for plant-based and clean-label supplements, and expanding demand across aging populations worldwide. Consumers are increasingly shifting away from synthetic micronutrients toward naturally derived vitamins and minerals sourced from botanical, marine, and fermented ingredients. The rapid penetration of e-commerce platforms, subscription-based supplement models, and personalized nutrition solutions is further accelerating global demand. Additionally, rising healthcare expenditure, growing urbanization, and increased focus on immunity, bone health, and general wellness continue to support long-term expansion of the natural multivitamin and minerals industry.

Key Market Insights

- Combined multivitamin and multimineral formulations dominate the market, accounting for nearly 46% of the 2025 global share due to consumer preference for comprehensive daily supplementation.

- Plant-based natural ingredient sources lead with over 54% share, reflecting strong demand for vegan, organic, and non-GMO certified formulations.

- North America holds approximately 34% of the global market share in 2025, driven by high supplement penetration and strong preventive healthcare awareness.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR due to rising middle-class income and increasing micronutrient deficiency awareness.

- Online retail channels contribute nearly 31% of global sales, supported by D2C subscription models and digital marketing strategies.

- Adults aged 19–49 years represent the largest consumer base, contributing approximately 38% of total market demand in 2025.

What are the latest trends in the natural multivitamin and minerals market?

Personalized and Subscription-Based Nutrition

Personalized nutrition is transforming the natural multivitamin and minerals market. Companies are leveraging AI-driven health assessments, biomarker testing, and DNA-based nutritional profiling to offer customized vitamin blends tailored to individual deficiencies and lifestyle needs. Subscription-based supplement delivery services are gaining traction, enhancing customer retention and enabling predictable recurring revenue streams. Consumers increasingly expect transparency, traceability, and clinically supported formulations, prompting manufacturers to integrate digital tools that improve product recommendations and health tracking.

Clean-Label and Sustainable Ingredient Innovation

Clean-label positioning has become central to brand differentiation. Consumers prefer organic-certified, non-GMO, allergen-free, and sustainably sourced ingredients. Fermented vitamins, algae-based minerals, and whole-food-derived micronutrients are gaining popularity due to superior bioavailability perceptions. Sustainable packaging innovations, including biodegradable bottles and refill pouches, are further strengthening brand loyalty. Regulatory emphasis on transparent labeling and ethical sourcing is encouraging manufacturers to invest in traceable supply chains and environmentally responsible production practices.

What are the key drivers in the natural multivitamin and minerals market?

Rising Preventive Healthcare Awareness

Growing global healthcare costs and increasing lifestyle-related diseases are shifting consumer focus toward prevention rather than treatment. Natural multivitamins are widely perceived as safer for long-term daily use compared to synthetic alternatives. Post-pandemic health consciousness has significantly increased immunity-focused supplementation, driving strong market expansion across developed and emerging economies.

Aging Global Population

The expanding geriatric population worldwide is significantly boosting demand for natural micronutrient supplementation. Aging individuals require higher levels of vitamins such as D, B12, and calcium due to declining absorption efficiency. Specialized age-targeted formulations are witnessing rising uptake, particularly in North America, Europe, and Japan.

Growth of Plant-Based Nutrition

The plant-based movement is influencing dietary supplement consumption patterns. Consumers are increasingly opting for botanical extracts and vegan-certified products. This trend is particularly strong among millennials and Gen Z populations, who prioritize sustainability and ethical sourcing in purchasing decisions.

What are the restraints for the global market?

Higher Production and Raw Material Costs

Naturally sourced vitamins and minerals require certified organic farming, sustainable harvesting, and complex extraction processes, resulting in higher production costs. Volatility in botanical raw material prices can impact profit margins and retail pricing.

Regulatory Complexity Across Regions

Stringent regulatory requirements related to health claims, labeling, and ingredient approvals vary significantly across countries. Compliance costs and longer approval timelines may delay product launches and restrict market entry for smaller players.

What are the key opportunities in the natural multivitamin and minerals industry?

Emerging Market Expansion

Rapid urbanization and growing middle-class populations in Southeast Asia, Latin America, and Africa present substantial growth opportunities. Rising awareness about micronutrient deficiencies and government-backed nutrition programs support bulk procurement and public-private partnerships.

Integration with Digital Health Platforms

Partnerships between supplement manufacturers and digital health platforms create opportunities for integrated wellness ecosystems. Mobile health apps offering deficiency tracking, supplement reminders, and health analytics enhance product adoption and long-term customer engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 17420 Million |

| Market Size in 2026 | USD 18865.86 Million |

| Market Size in 2031 | USD 28107.28 Million |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Tablets dominate the product form segment, accounting for approximately 32% of the global market share in 2025. The leadership of tablets is primarily driven by their cost efficiency, ease of large-scale manufacturing, dosage accuracy, and extended shelf life compared to alternative formats. Their compatibility with automated production lines and stability under varying storage conditions make them highly attractive to manufacturers and retailers alike. Moreover, tablets are widely accepted across both developed and emerging markets due to their affordability and familiarity among consumers. Gummies are emerging as the fastest-growing product form, supported by superior taste profiles, chewable convenience, and strong appeal among pediatric, millennial, and geriatric populations who prefer easy-to-consume formats. Continuous innovation in low-sugar and plant-based gummy formulations further accelerates adoption. Capsules and softgels continue to maintain strong demand in premium product categories, particularly for herbal extracts, omega-based nutrients, and high-bioavailability mineral complexes, where enhanced absorption and reduced gastrointestinal discomfort serve as key purchase drivers.

Nutrient Composition Insights

Combined multivitamin and multimineral formulations lead the nutrient composition segment, capturing nearly 46% of the global market share in 2025. The leading segment driver is consumer preference for comprehensive, all-in-one daily supplementation that simplifies health routines and addresses multiple micronutrient gaps simultaneously. Increasing awareness regarding lifestyle-related deficiencies, immunity support, and preventive healthcare has strengthened demand for broad-spectrum formulations. Whole-food-based natural blends are gaining substantial traction within premium segments, particularly among health-conscious consumers seeking clean-label, minimally processed, and plant-derived ingredients. Demand for condition-specific blends targeting immunity, bone health, cognitive performance, and energy metabolism is further expanding the category, supported by scientific validation and transparent labeling practices.

Distribution Channel Insights

Online retail and direct-to-consumer platforms account for approximately 31% of global revenue, making them the leading distribution channel in 2025. The primary growth driver for this segment is digital convenience combined with competitive pricing, subscription-based replenishment models, and personalized recommendation algorithms. The expansion of e-commerce ecosystems, influencer-driven marketing, and data-driven consumer targeting has significantly improved product accessibility and brand engagement. Pharmacies and drug stores remain critical distribution pillars, particularly for clinically recommended or physician-endorsed formulations, benefiting from consumer trust and professional guidance. Specialty health stores maintain a strong presence in developed markets, where curated portfolios of organic, non-GMO, and allergen-free supplements cater to discerning consumers seeking premium and niche health solutions.

Age Group Insights

Adults aged 19–49 years represent the leading age group segment, contributing approximately 38% of global demand in 2025. The key driver for this segment is rising preventive healthcare awareness among working professionals managing active lifestyles, stress, and dietary imbalances. Increased participation in fitness activities, growing adoption of plant-based diets, and rising disposable incomes further strengthen supplement consumption within this demographic. The geriatric population is expanding steadily, supported by age-related nutrient deficiencies, chronic disease management needs, and higher healthcare spending. Pediatric supplementation also remains relevant, particularly for immunity and cognitive development, driven by parental awareness and pediatrician recommendations.

Explore more data points, trends and opportunities Download Free Sample Report

Natural Multivitamin and Minerals Market Segmentations

By Product Form

- Tablets

- Capsules

- Softgels

- Gummies

- Powders

- Liquid Formulations

By Nutrient Composition

- Multivitamin-Only Formulations

- Multimineral-Only Formulations

- Combined Multivitamin & Multimineral Formulations

- Whole-Food Based Natural Blends

- Herbal-Infused Vitamin & Mineral Complexes

By Age Group

- Pediatric

- Adolescents

- Adults

- Middle-Aged

- Geriatric

By Gender-Specific Formulation

- Men-Specific Formulas

- Women-Specific Formulas

- Unisex/General Formulas

- Prenatal & Postnatal Formulas

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Health Stores

- Practitioner/Clinical Sales

By Application

- General Wellness & Preventive Healthcare

- Immunity Support

- Bone & Joint Health

- Cardiovascular Health

- Cognitive & Brain Health

- Beauty & Skin Health

- Sports & Performance Nutrition

Regional Insights

North America

North America holds approximately 34% of the global market share in 2025, positioning it as the leading regional market. The United States accounts for over 28% of global revenue, supported by high healthcare expenditure, advanced retail infrastructure, and strong consumer awareness regarding preventive nutrition. Growth in the region is driven by high dietary supplement penetration rates, expanding demand for clean-label and plant-based formulations, and continuous product innovation. The presence of established manufacturers, robust regulatory frameworks, and widespread adoption of subscription-based e-commerce models further strengthen regional dominance. Canada contributes steadily, supported by rising interest in natural health products and strong pharmacy distribution networks.

Europe

Europe represents nearly 28% of the global market share, with Germany, the United Kingdom, and France serving as major revenue contributors. Regional growth is driven by stringent regulatory standards that enhance consumer confidence, along with strong demand for organic-certified and sustainably sourced supplements. Increasing aging populations across Western Europe are fueling demand for bone health, cardiovascular support, and cognitive wellness formulations. The United Kingdom is among the fastest-growing European markets, supported by expanding adoption of plant-based nutrition and vegan supplementation trends. Germany remains a key hub for scientifically validated and pharmacy-dispensed products, reinforcing steady market expansion.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR exceeding 9%. China and India are primary growth engines, driven by rising middle-class populations, urbanization, and increasing awareness of preventive healthcare. Expanding digital commerce platforms and growing penetration of international supplement brands are accelerating regional demand. In India, increasing disposable income and heightened focus on immunity following recent public health concerns are strengthening consumption. China’s growth is further supported by cross-border e-commerce channels and demand for premium imported formulations. Japan represents a mature yet stable market characterized by high demand for quality-certified, science-backed, and condition-specific supplements tailored to aging populations.

Latin America

Latin America accounts for approximately 6% of global demand, led by Brazil and Mexico. Regional growth is driven by expanding urban populations, improving retail infrastructure, and rising awareness of preventive healthcare. Increasing participation in sports and fitness activities, coupled with growing availability of affordable supplement formats, is enhancing market penetration. Government-led public health campaigns promoting nutritional awareness and expanding pharmacy chains are further supporting steady regional development.

Middle East & Africa

The Middle East & Africa contribute around 4% of the global market, with the United Arab Emirates and South Africa serving as key growth hubs. Rising disposable income levels, expanding modern retail formats, and increasing health consciousness are primary drivers across the region. Demand for premium imported supplements is particularly strong in Gulf Cooperation Council countries, supported by expatriate populations and high per-capita income. In Africa, improving healthcare access, urbanization, and growing awareness of micronutrient deficiencies are gradually expanding supplement adoption, creating long-term growth potential.

Key Players in the Natural Multivitamin and Minerals Market

- Amway Corp.

- Nestlé Health Science

- Herbalife Nutrition Ltd.

- Abbott Laboratories

- Bayer AG

- GNC Holdings

- Nature’s Sunshine Products

- Blackmores Limited

- Himalaya Wellness Company

- NOW Foods

- Garden of Life

- Nature’s Way

- Swisse Wellness

- Otsuka Holdings Co., Ltd.

- Arkopharma