Natural Folic Acid Market Size

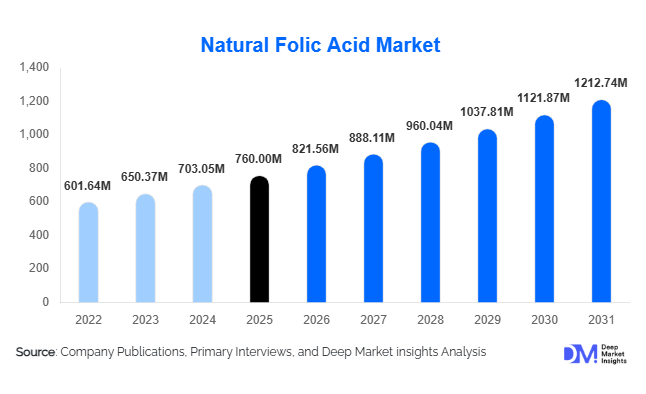

Accoding to Deep Market Insights, the global natural folic acid market size was valued at USD 760 million in 2025 and is projected to grow from USD 821.56 million in 2026 to reach USD 1,212.74 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The natural folic acid market growth is primarily driven by rising demand for clean-label vitamins, growing prenatal and women’s health supplement consumption, and increasing integration of naturally sourced micronutrients into functional foods and pharmaceutical formulations.

Key Market Insights

- Microbial fermentation-based natural folic acid dominates production, accounting for nearly 48% of total supply due to scalability and high-purity output.

- Dietary supplements represent the largest application segment, contributing approximately 46% of total demand in 2025.

- North America holds the largest regional share (32%), supported by strong supplement penetration and mandatory fortification programs.

- Asia-Pacific is the fastest-growing region, expanding at nearly 9.5% CAGR due to rising health awareness and government nutrition initiatives.

- High-purity (≥98%) variants account for over 52% of market revenue, driven by pharmaceutical-grade and prenatal formulations.

- Top five manufacturers control nearly 58% of global market share, indicating moderate consolidation with strong technological barriers.

What are the latest trends in the natural folic acid market?

Shift Toward Clean-Label & Non-GMO Fermentation

Manufacturers are increasingly adopting non-GMO microbial fermentation techniques to produce high-purity natural folate. This aligns with consumer demand for transparency and naturally sourced ingredients in prenatal supplements and fortified foods. Clean-label claims have become a strong differentiator in North America and Europe, where regulatory scrutiny and consumer awareness are high. Producers are investing in strain optimization technologies to improve yields while maintaining organic and allergen-free certifications. This transition is allowing natural folic acid to command a price premium of 15–25% over synthetic alternatives.

Expansion into Functional Foods & Plant-Based Nutrition

Natural folic acid is increasingly incorporated into plant-based dairy alternatives, protein bars, breakfast cereals, and fortified beverages. The global functional foods industry, growing above 7% annually, is creating sustained demand for naturally derived micronutrients. Brands are reformulating products to eliminate synthetic vitamins and strengthen their natural positioning. This trend is particularly strong in Asia-Pacific, where rising middle-class consumers are embracing preventive healthcare and fortified daily nutrition.

What are the key drivers in the natural folic acid market?

Rising Prenatal & Women’s Health Awareness

Global health agencies strongly recommend folate supplementation during pregnancy to prevent neural tube defects. Increasing maternal age and fertility planning have expanded the prenatal supplements market, which is growing near 9–10% annually. Natural folate is increasingly preferred in premium prenatal formulations due to perceived higher bioavailability and cleaner sourcing.

Growth of the Global Nutraceutical Industry

The global nutraceutical industry exceeded USD 450 billion in 2025 and continues expanding steadily. Natural folic acid benefits from widespread inclusion in multivitamins, B-complex supplements, and immune support products. E-commerce expansion and direct-to-consumer supplement brands are further accelerating global distribution.

What are the restraints for the global market?

Higher Production Costs Compared to Synthetic Alternatives

Natural folic acid produced through fermentation or plant extraction involves higher capital investment, strain development costs, and longer production cycles. This results in a pricing premium that limits penetration in price-sensitive markets across parts of Africa and Latin America.

Raw Material Price Volatility

Fermentation-based production depends on agricultural feedstocks such as molasses and plant biomass. Fluctuations in raw material prices and supply chain disruptions can affect profitability and pricing stability for manufacturers.

What are the key opportunities in the natural folic acid industry?

Mandatory Food Fortification Programs

Expanding folic acid fortification mandates in developing nations present large-scale opportunities. Governments in Southeast Asia, Africa, and Latin America are strengthening maternal nutrition policies, creating stable institutional demand for high-quality folate supplies. Suppliers entering long-term public procurement contracts can secure consistent revenue streams.

Premium Bioactive Folate Formulations

Development of advanced bioactive blends combining folate with vitamin B12, iron, and DHA offers margin expansion opportunities. Premium prenatal and cognitive health products are driving demand for high-potency formulations, especially in North America, Europe, and Japan.

Source Insights

Microbial fermentation-based natural folic acid leads the global market with approximately 48% share in 2025, making it the dominant source segment. The leadership of fermentation-derived folic acid is primarily driven by its ability to consistently achieve ≥98% purity levels, ensuring suitability for pharmaceutical-grade and premium nutraceutical applications. The scalability of microbial fermentation processes enables manufacturers to maintain cost efficiencies while meeting stringent global regulatory standards across the United States, Europe, and Asia-Pacific. Additionally, fermentation technology offers controlled production environments, stable quality parameters, and improved traceability, which are critical for clean-label and high-compliance markets. Plant-derived folate represents a niche but steadily expanding segment, particularly in certified organic, vegan, and plant-based product lines where natural sourcing claims influence consumer purchasing decisions. Algae-based sources remain an emerging category, gaining traction in specialty formulations and sustainable ingredient portfolios, especially among premium nutraceutical brands seeking differentiated positioning.

Form Insights

Powder form accounts for nearly 55% of total market revenue in 2025, positioning it as the leading segment within the form category. The dominance of powdered folic acid is primarily driven by its superior stability, extended shelf life, and ease of incorporation into tablets, capsules, sachets, and premix formulations. Manufacturers prefer powder due to its compatibility with large-scale blending processes, reduced transportation costs, and simplified storage requirements. Encapsulated and beadlet forms are witnessing accelerated adoption in pharmaceutical and high-value nutraceutical applications where controlled release, enhanced bioavailability, and moisture protection are essential. These specialized forms support advanced therapeutic formulations and fortified infant nutrition products. Liquid concentrates, while representing a smaller share, maintain consistent demand in beverage fortification and ready-to-drink nutritional products, particularly within functional beverage segments that require rapid solubility and homogeneous dispersion.

Application Insights

Dietary supplements dominate the application landscape with approximately 46% share of the 2025 market, supported by sustained global demand for multivitamins, prenatal supplements, and women’s health formulations. The leading position of dietary supplements is driven by increasing awareness of folate’s role in fetal neural development, cardiovascular health, and overall metabolic function. The pharmaceutical segment follows, benefiting from prescription-based prenatal therapies and therapeutic interventions for folate deficiency-related conditions. Governments and healthcare systems in developed economies continue to promote preventive supplementation, further strengthening pharmaceutical demand. Functional foods represent the fastest-growing application segment, expanding at a CAGR exceeding 9%, as food manufacturers increasingly fortify cereals, dairy alternatives, and bakery products to align with preventive health trends and regulatory fortification policies.

End-Use Industry Insights

Nutraceutical manufacturers account for approximately 44% of total demand and represent the fastest-growing end-use industry segment. Their growth is fueled by rising consumer preference for preventive healthcare, personalized nutrition, and clean-label dietary supplements. The infant nutrition sector is expanding steadily, supported by the global infant formula market projected to surpass USD 90 billion by 2030, where folic acid remains a critical micronutrient for developmental health. Pharmaceutical manufacturers maintain stable annual growth of approximately 5–6%, driven by prescription prenatal formulations, hospital supply contracts, and standardized therapeutic dosages. The expanding role of contract manufacturing organizations (CMOs) and private-label supplement producers further contributes to sustained industrial demand across regions.

| By Source | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global natural folic acid market in 2025, supported by advanced healthcare infrastructure, strong dietary supplement penetration, and regulatory-backed fortification mandates. The United States represents the largest importer and consumer, driven by mandatory folic acid fortification of enriched grains under FDA regulations and high consumer adoption of prenatal and multivitamin supplements. Strong retail distribution networks, e-commerce growth, and expanding functional food innovation further support regional expansion. Canada demonstrates steady growth through public health nutrition programs, maternal health awareness initiatives, and structured dietary guidelines that encourage micronutrient supplementation, contributing to consistent regional demand.

Europe

Europe holds approximately 27% market share, led by Germany, France, the United Kingdom, and Italy. Regional growth is driven by strict regulatory standards governing ingredient purity and labeling, which favor high-quality fermentation-based folic acid. Increasing consumer preference for clean-label, non-synthetic, and sustainably sourced vitamins further accelerates demand. Preventive healthcare policies, aging population demographics, and growing prenatal supplement awareness support steady market expansion. Additionally, Europe’s strong pharmaceutical manufacturing base and advanced nutraceutical innovation ecosystem enhance regional consumption and intra-regional trade.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at nearly 9.5% CAGR. China dominates global production and export capacity due to large-scale fermentation infrastructure, cost competitiveness, and integrated supply chains. Domestic consumption is also rising with increasing functional food fortification and expanding middle-class health awareness. India records the highest consumption growth at around 10% CAGR, driven by expanding prenatal supplement awareness, improving maternal healthcare access, and domestic pharmaceutical manufacturing incentives such as the “Make in India” initiative. Japan and South Korea contribute to regional growth through demand for premium-grade, high-purity nutraceutical ingredients and advanced functional food innovation. Rapid urbanization, dietary shifts, and expanding e-commerce supplement sales collectively reinforce Asia-Pacific’s growth trajectory.

Latin America

Latin America demonstrates steady growth, led by Brazil and Mexico. Regional expansion is supported by government-led maternal nutrition initiatives, increasing awareness of micronutrient deficiencies, and rising dietary supplement imports. Expanding middle-class populations, improved healthcare access, and gradual strengthening of food fortification policies contribute to sustained demand. Local pharmaceutical production capabilities and growing retail pharmacy networks further enhance regional distribution efficiency.

Middle East & Africa

The Middle East & Africa region represents an emerging growth market, with the United Arab Emirates and South Africa serving as key demand centers. Growth is driven by increasing health consciousness, expanding expatriate populations, and rising imports of premium dietary supplements. Government-led nutrition programs and expanding private healthcare infrastructure support gradual market development. Across parts of Africa, long-term potential is supported by growing food fortification initiatives aimed at addressing micronutrient deficiencies, improving maternal health outcomes, and strengthening public health nutrition frameworks.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Folic Acid Market

- DSM-Firmenich

- BASF SE

- Zhejiang Medicine Co., Ltd.

- Jiangxi Tianxin Pharmaceutical

- Hebei Jiheng Pharmaceutical

- Xinfa Pharmaceutical

- Nantong Changhai Food Additive

- Gnosis by Lesaffre

- Divi’s Laboratories Ltd.

- Amoli Organics

- Lonza Group

- SternVitamin GmbH

- Vitablend Nederland B.V.

- Farbest Brands

- Parchem Fine & Specialty Chemicals