Natural Clouding Agents Market Size

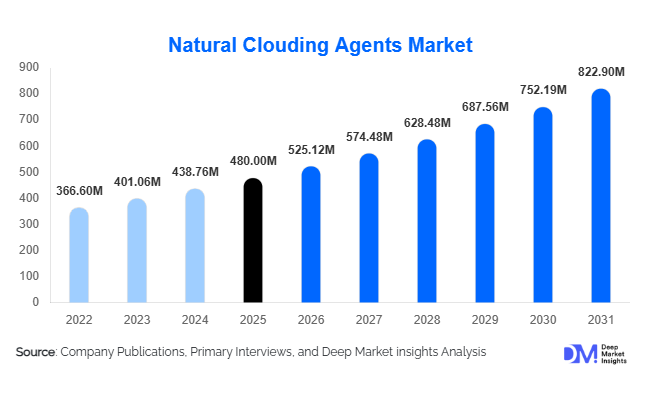

According to Deep Market Insights,the global natural clouding agents market size was valued at USD 480 million in 2025 and is projected to grow from USD 525.12 million in 2026 to reach USD 822.90 million by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). The natural clouding agents market growth is primarily driven by rising demand for clean-label beverage formulations, increased adoption of plant-based emulsifiers, and strong expansion in functional and ready-to-drink (RTD) beverage categories globally. Beverage manufacturers are increasingly replacing synthetic opacity enhancers with citrus-based and botanical-derived clouding systems to comply with regulatory standards and evolving consumer preferences.

Key Market Insights

- Citrus-based clouding agents dominate the global market, accounting for nearly 48% of total revenue share in 2025 due to strong compatibility with soft drinks and fruit beverages.

- Liquid emulsions lead by form, contributing approximately 55% of demand, as large-scale beverage processors prefer ready-to-use, stable formulations.

- Beverage manufacturers represent the largest end-use segment, holding close to 65% of overall consumption globally.

- Asia-Pacific is the largest regional market, accounting for nearly 30% of 2025 demand, supported by expanding beverage production in China and India.

- Functional beverages are the fastest-growing application, driven by health-focused consumers and fortified drink innovations.

- The top five companies control approximately 42% of the global market, reflecting moderate consolidation and strong R&D investment.

What are the latest trends in the natural clouding agents market?

Clean-Label Reformulation Accelerating

Global beverage and food companies are aggressively reformulating products to remove artificial emulsifiers and synthetic opacity agents. Natural clouding agents derived from citrus oils, gum arabic, and plant-based extracts are increasingly being incorporated into carbonated beverages, fruit juices, and flavored waters. This shift is particularly strong in North America and Europe, where regulatory frameworks and consumer awareness around ingredient transparency are more stringent. Manufacturers are investing in traceable sourcing models and sustainable citrus supply chains to further differentiate their products. Clean-label certifications and non-GMO claims are becoming critical selling points, especially for premium beverage brands targeting health-conscious consumers.

Spray-Dried and Encapsulated Solutions Gaining Popularity

Technological advancements in spray-drying and microencapsulation are reshaping the product landscape. Powdered natural clouding agents are gaining traction due to extended shelf life, lower transportation costs, and improved stability under acidic and thermal processing conditions. These solutions are particularly attractive for export-oriented beverage manufacturers in Asia and Latin America. Encapsulation technologies also enable better flavor oil stabilization and controlled release functionality, allowing manufacturers to integrate multiple functionalities within a single ingredient system. As global beverage production scales up, demand for cost-efficient and stable powdered systems is expected to increase significantly.

What are the key drivers in the natural clouding agents market?

Growth in RTD and Functional Beverages

The rapid expansion of RTD teas, flavored waters, sports drinks, and fortified beverages is a major growth driver. These products require stable emulsification systems to prevent phase separation and ensure consistent visual appeal. With the global functional beverage industry growing at over 8% annually, natural clouding agents are benefiting directly from increased formulation activity and product launches. Beverage producers are increasingly focusing on visually appealing, nutrient-enriched drinks, further boosting ingredient demand.

Expansion of Plant-Based Dairy Alternatives

The plant-based dairy market, valued at over USD 30 billion globally, is expanding at a high single-digit CAGR. Natural clouding agents enhance opacity and mouthfeel in almond, oat, soy, and coconut beverages, mimicking traditional dairy appearance. As plant-based consumption rises across North America, Europe, and Asia-Pacific, ingredient suppliers are developing customized systems specifically tailored for alternative milk applications.

What are the restraints for the global market?

Volatility in Raw Material Prices

Key raw materials such as citrus oils and gum arabic are agricultural derivatives, making them vulnerable to climatic changes, supply chain disruptions, and geopolitical instability. Price volatility impacts production costs and margins, particularly for small and mid-sized manufacturers.

Performance Limitations in Extreme Processing Conditions

Natural emulsions sometimes demonstrate lower stability compared to synthetic alternatives in high-shear or highly acidic formulations. Continuous R&D investment is required to improve pH tolerance, temperature stability, and shelf-life performance, which can increase development costs.

Product Type Insights

Citrus-based clouding agents dominate the global market, accounting for approximately 48% of the total market share in 2025. The leadership of this segment is primarily driven by the abundant availability of citrus by-products from juice processing industries, which ensures cost efficiency and stable raw material supply. Their superior compatibility with carbonated soft drinks and fruit juices, along with strong emulsification performance and clean-label positioning, further strengthens demand. Beverage manufacturers prefer citrus-derived systems due to their ability to deliver natural opacity, visual appeal, and flavor enhancement without compromising regulatory compliance. Botanical and gum-based systems, including acacia and plant-resin formulations, are gaining traction as manufacturers diversify sourcing strategies and respond to clean-label and allergen-free requirements. Continuous innovation in plant-derived emulsifiers and resin stabilization technologies is expected to enhance functional stability, expand application scope, and support long-term diversification within the product type segment.

Form Insights

Liquid emulsions account for nearly 55% of global demand in 2025, maintaining dominance due to their operational convenience and compatibility with automated, high-speed bottling and blending lines. The leading segment driver is the beverage industry's preference for ready-to-use formulations that reduce processing time, minimize dispersion challenges, and improve batch consistency. Liquid formats also ensure uniform cloud stability and faster incorporation into beverage matrices. However, powdered clouding agents are projected to witness faster growth over the forecast period, particularly in export-oriented beverage manufacturing and shelf-stable drink categories. Their lower transportation costs, longer shelf life, and improved storage efficiency make them attractive for emerging markets and cross-border trade. Advancements in spray-drying technologies and encapsulation methods are further enhancing the performance stability of powdered variants, strengthening their adoption across global supply chains.

Application Insights

Carbonated soft drinks lead the application segment with around 32% share of total demand in 2025, driven primarily by sustained global consumption volumes and consistent product reformulation cycles. The leading segment driver is the need for visual opacity and flavor enhancement in citrus-flavored and fruit-based soft drinks, where clouding agents play a critical functional role. Meanwhile, functional beverages represent the fastest-growing application category, supported by increasing consumer awareness regarding health, immunity, and wellness. The expansion of fortified drinks, vitamin-enhanced beverages, plant-based refreshers, and probiotic formulations across North America and Asia-Pacific is accelerating demand for natural clouding systems that align with clean-label and transparency trends. Growth in ready-to-drink teas, sports drinks, and nutraceutical beverages further strengthens application diversification.

End-Use Industry Insights

Beverage manufacturers dominate end-use consumption, accounting for approximately 65% of overall market share. The primary driver for this leading segment is the continuous innovation cycle within the global beverage industry, characterized by flavor diversification, premiumization, and reformulation toward natural ingredients. Large-scale beverage producers rely heavily on stable and regulatory-compliant clouding agents to maintain product consistency across international markets. Dairy alternative producers represent the fastest-growing end-use category, supported by strong global growth in plant-based milk, yogurt drinks, and protein-enriched beverages. The expansion of oat, almond, soy, and coconut-based beverage production requires specialized clouding systems to improve texture and visual appeal. Nutraceutical beverage manufacturers are emerging as a niche but rapidly expanding segment, driven by increasing demand for functional health beverages and fortified liquid supplements.

| By Source | By Form | By Application | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 28% of the global market share in 2025, with the United States serving as the primary contributor. Regional growth is driven by high per capita consumption of carbonated and functional beverages, strong demand for clean-label ingredients, and advanced beverage processing infrastructure. Strict regulatory standards established by agencies such as the U.S. Food and Drug Administration (FDA) encourage the adoption of natural and compliant clouding systems. Continuous product innovation in sports drinks, flavored waters, and fortified beverages further accelerates demand. The U.S. remains one of the largest importers of citrus-based clouding systems, benefiting from a well-established distribution network and large-scale beverage manufacturing capacity.

Europe

Europe accounts for nearly 25% of global share, led by Germany, France, and the United Kingdom. Regional growth is primarily driven by stringent clean-label mandates and regulatory frameworks enforced by the European Food Safety Authority (EFSA), which strongly promote natural ingredient adoption. Increasing consumer preference for organic beverages, low-sugar formulations, and plant-based drinks supports demand for botanical and citrus-derived clouding agents. Additionally, the region’s advanced research and development ecosystem and emphasis on sustainable sourcing practices are fostering innovation in plant-resin and gum-based systems.

Asia-Pacific

Asia-Pacific leads globally with approximately 30% share in 2025, driven by rapid urbanization, expanding middle-class populations, and increasing disposable incomes. China and India are major contributors due to significant expansion in beverage manufacturing infrastructure and rising demand for flavored and functional drinks. India is projected to be the fastest-growing market, registering growth above 11% CAGR, supported by increasing investments in food processing, favorable government initiatives promoting manufacturing, and strong growth in packaged beverage consumption. The region also benefits from local citrus production, which supports cost-efficient sourcing of raw materials for clouding agents.

Latin America

Latin America contributes approximately 10% of the global market share, with Brazil and Mexico serving as key growth engines. Regional expansion is supported by strong fruit juice production industries, abundant citrus cultivation, and export-oriented beverage manufacturing. Increasing consumption of flavored carbonated drinks and ready-to-drink juices, combined with improving retail distribution networks, further stimulates demand. Growing foreign investments in beverage processing facilities are also enhancing technological adoption and formulation upgrades across the region.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market share. Growth is driven by rising soft drink consumption in Saudi Arabia, the United Arab Emirates, and South Africa, supported by expanding urban populations and increasing youth demographics. Infrastructure development in food and beverage processing, along with government-led economic diversification initiatives, is strengthening manufacturing capacity. The region’s growing demand for premium imported beverages and flavored refreshment drinks is further contributing to steady adoption of natural clouding systems.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Natural Clouding Agents Market

- Givaudan

- Firmenich

- Symrise AG

- Kerry Group

- International Flavors & Fragrances Inc.

- Döhler Group

- Sensient Technologies Corporation

- ADM

- Tate & Lyle

- Ashland Global Holdings Inc.

- Cargill Incorporated

- Ingredion Incorporated

- Nexira

- Aarkay Food Products Ltd.

- Florida Chemical Company